This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Over the last seven years, software startup investing has changed quite a bit. In other words, if machine learning startups raised the same amount of money in 2016 is 2010, the chart would show a value of 1. If those startups raised twice the amount of capital then the figure would be 2.

Today is January 10, 2017. In less earth shattering news, the fact that it's 2017 also means that my "SaaS Funding in 2016" napkin needs an update. Today I'd like to take a stab at the (early) 2017 answer to that question. So, what does it take to raise capital, in SaaS, in early 2017? Here's the 2017 SaaS Funding Napkin!

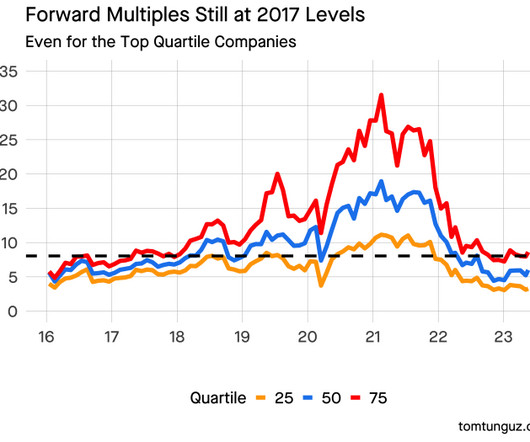

After the correction earlier this year, public valuation multiples had reset to those of 2017. Not too long before the public market correction, high-growth startups routinely commanded 100x ARR multiples. Congratulations to team Figma on building their impressive business. That’s not a bear market multiple.

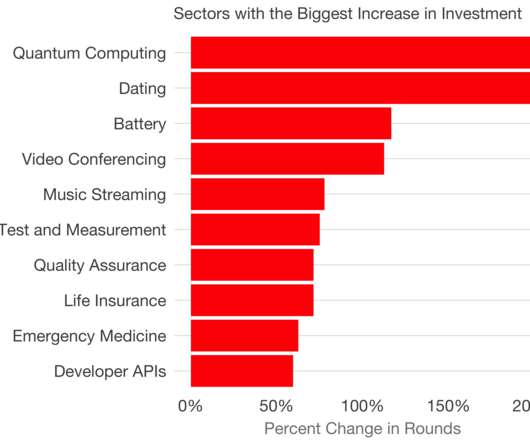

From time to time, I chart the fastest growing categories of startup investment in the US for seed through Series C. Here are 2015 , 2017 , This year, I was certain the categories would have been influenced by COVID19.

Comparing 2017 averages to seven year highs, we observe Series A, Series B, and Series Seed round sizes are effectively at their all-time highs, ignoring some minor differences. Should the current trend continue, 2017 would see the fewest number of rounds since 2012, and a 45% reduction from 2014 high. billion from $4.2

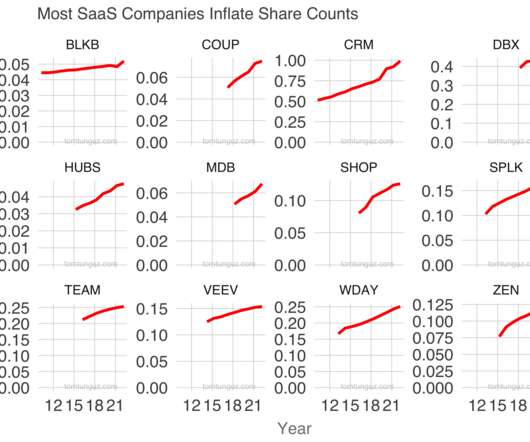

Before a startup is founded, no stock exists. The startup can inflate share count by creating shares. By the time it’s public, more than 100m shares exist across hundreds of shareholders (employees, institutional investors, retail investors). Conversely, the company can deflate share count by buying shares and destroying them.

Is your B2B startup now part of the past … because it was founded before 2023? VCs especially are obsessed with AI-native startups. Has growth slowed while new AI entrants in your space are growting at epic rates? No one’s coming to save you. It’s not too late. We are early. The market has fundamentally shifted.

I didn’t calculate this figure in 2017. More money enables startups to achieve greater milestones before raising the next round. (note I’m switching from median to average here). In 4 years, we’ve seen a 4x increase in the median MRR of a Series A SaaS company. That’s quite a growth rate.

From startup to $500M CARR, Spencer Burke, SVP of Growth at Braze, shares how Braze scaled a growth and customer success team. As an early startup team, you’re doing every job under the sun. We get lazy writing job descriptions, and taking shortcuts is a luxury most startups don’t have. But that was it.

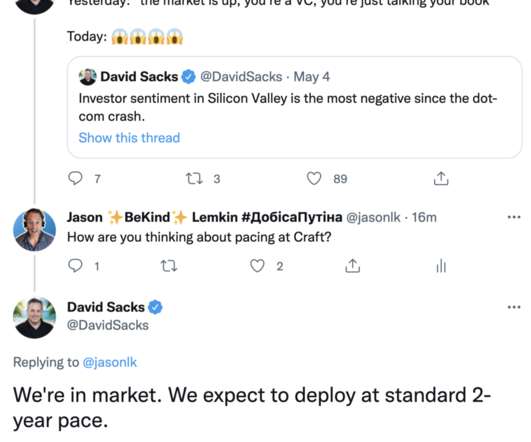

If as a VC you invested at $10m pre initially, and say it’s 2021 and that same startup is doing a 100x round at a $300m valuation, this early VC fund can pick and choose whether to invest more or not. For example, SaaStr Fund I from 2017 has now deployed $61m of its $68m. Older funds run out of reserves. Just ask. No one asks.

The rest of the top quartile has remained depressed, suppressing the cohort to 2017 levels, just as they were last year. But rally hasn’t convincingly beaten the black line representing the 2017 median. These top five stocks explain the most recent earnings upward in the chart above.

As the year is coming to an end I’d like to share a few thoughts on what we’ll be looking for in the SaaS world in 2017. Related posts (from this blog): Why (most) SaaS startups should aim for negative MRR churn How fast is fast enough? Will it be a SaaS solution with voice as the primary form of input?

We had a closer look at who the young upstarts of Latin America are in search of the most exciting Latin American SaaS startups. With them in mind, we have created our Startup Program , tailored especially for SaaS startups. Here are the most exciting Latin American SaaS startups that we cannot wait to meet in less than a month.

In 2017, SaaS companies reported their cost of customer acquisition had increased by 65% in the previous five year period. What happened to these figures during Covid? We can examine the sales efficiency of public software companies to get a sense.

The article pointed to the seeming collapse in the amount of venture capital raised by San Francisco startups relative to other regions. If we compare San Francisco to the Valley by round, Series Bs and Series Ds have increased markedly in the valley in 2017. Now it’s the Valley startups’ turn to raise.

But in 2017, the Series A median surpassed the 2009 Series B median. The truth is - in today’s market - the median startup is doing that already. In 2009, the median post Series C startup counted $20.8M In 2018, a post-Series B startup would have received $26.7M The dashed blue line is the median series A from 2009.

The biggest change is that growth investors, the folks that invest at $10m+ ARR, are often now looking for SaaS startups to be tripling at this stage — not doubling. The post Is It Now “Triple, Triple, Triple, Double, Double, Double” — T3D3 — For Top Tier SaaS Startups? Or at least growing 150% or so.

At Saastr, Jason and I discussed the role of private equity in SaaS on stage as a potential acquisition path for SaaS startups. Private equity hasn’t been a common exit route for venture backed startups in the past. Said another way, PE firms are spending as much buying SaaS startups as corporate acquirers.

A funny thing happened along the way to Sand Hill Road in the last decade : startups stopped talking about how much runway a Series A would buy them. In 2010, the median software Series A startup raised $3.2m & employed 15 people at about $150k average cost. Today, the public markets value companies like it’s 2017.

So if things are slowing down at your startup, be honest about the root cause. Blame “the economy” too much, and you’re doing yourself a disservice. It’s not slowing down Salesforce, Snowflake, or almost any other SaaS or Cloud leader. Salesforce Growth: 2023 $31.8B (guidance) 2022 $26.5B 2021 $21.25B 2020 $17.1B 2014 $4.1B.

The Rebrand That Changed Everything 2017’s pivot from dapulse to monday.com wasn’t just a name change. Product-Led Growth Before It Was Cool While others were building massive sales teams, Zinman pushed for a product that would sell itself. The result? ARR growth?

(Note: I wrote a version of this in 2017 when times were good. As a startup, there are few things more important than Being Present: Your customers need to believe. Startups are a journey. If you’ve never run a hot startup, or worked at a hot startup, you may not get this. So here’s the 2020+ version). __.

While the data ends here, here’s what I can tell you I am seeing in growth rounds today: Very few growth rounds are happening at all When the do happen, they are for capital efficient startups growing > 50% at scale And … the peak valuation is about 15x. For the best ones.

The point is that SaaS multiples are still higher than where they were from 2010-2017. Draw a straight line and assume multiples gradually expand at the same rate as they were growing from 2017-2019. The Bear Case: Multiples are still elevated compared to the pre-2018 period. It just went nuts during Peak Covid. A related post here.

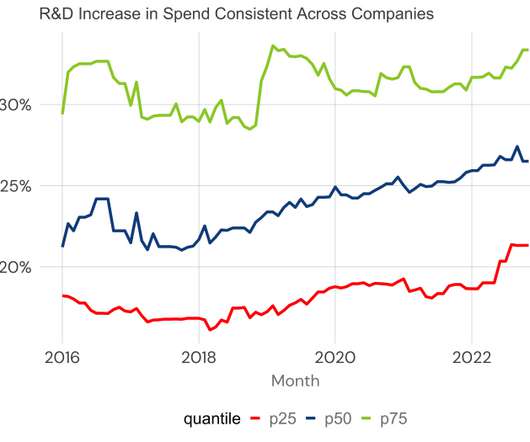

During Office Hours with Lee Kirkpatrick , Lee recalled managing a startup through a downturn. Starting in 2017 when the data is richer, the PLG companies increased R&D spend from 27.5% The business cut R&D spend to conserve cash. I wondered if a similar pattern existed in the public software markets.

Up until say 2017–2018 or so, in SaaS, there was a rough rule: a relatively small amount of secondary liquidity ($1m-$2m) would be offered by growth investors in top VC rounds once a startup crossed $10m ARR or so. The demand to buy founders’ shares at all but a handful of super-hot startups has waned.

As the UKs tech startup ecosystem continues to thrive, visionary founders are driving innovation across various industries, shaping the future of technology , finance , healthcare , and beyond. In this article, we highlight the top 10 tech startup founders in the UK for 2025 (who you should be following if you arent already!),

Starting in 2017, revenue recognition for SaaS companies will change, and SaaS startups will have more flexibility in the way they record revenue than in the past. Public companies must transition to these new regulations starting in 2017. Private companies have the option to migrate to these new standards in 2017.

In 2017, there will be a lot of comparison between the prices public bound companies fetch at IPO compared to the last round private valuations as the public window opens. Given all that change, which early round will be the hardest to raise for founders in 2017? Let’s take a look at the Crunchbase data for US startups.

This trend started in 2014 and has continued through the first quarter of 2017. Though quite rare in 2010, startups have raised more than 750 second seed rounds in each of the last three years. This data shows that they are broadly accepted as a common way to finance an early stage startup. It’s quite nearly always 2.

rates them on 3-Year Growth – a slightly strange metric for start-ups at all different stages), for SaaS and SaaS-ish startups: [note, the higher they are on the list, the faster they are growing on a % basis YoY]. #7 Where it Went: $45m revenue in 2017 and reported $100m+ in 2021, but acquired for modest sum in 2021. 557 SEOmoz.

And it has been since 2017 or so! There are 1000s of startups any BigCo can and does partner with. But what about 25% of a smaller, but fast-growing startup where the integration is even tighter? Salesforce’s biggest source of new revenue isn’t CRM or even support. It’s partners and platform. as a partner.

The Return to the Startup Game. In 2017, Bansal sold his unicorn company AppDynamics to Cisco for $4 billion. Says Bansal, “You should be doing what you enjoy…I realized I really enjoyed the journey of building a startup.” Easier With Second Startup: Fundraising, Managing the Board, Predicting the Future.

After all the hype and ICO-mania in 2017, the flurry of startups attempting to solve every startup with a distributed ledger and the collapse of currencies in 2018, one startup emerges in 2019 with the next killer use case; Bitcoin being the first. Volumes relative to 2017 didn’t change materially, though.

Jeff says he’s realized startups are either “product constrained or distribution constrained “ Make your investments accordingly. Finally, the session we did with Jeff at the 2017 SaaStr Annual right after Twilio’s IPO was incredible. If your customers love your product now, hire reps.

More than 30% of the initial coin offerings (ICO) in 2017 target developers and businesspeople with their products. B2B crypto companies raised about $400M of ICO dollars in 2017. In contrast, blockchain startups are exploring inter-company applications, processes that involve two or more companies. The numbers are still small.

Watch her session from Annual 2017, and if you aren’t inspired, you are doing it wrong: #3. He was still working at a struggling startup in downtown San Mateo, which I think ultimately sold for just $10m and maybe was down to 2 employees at that point. Even in a class of unicorns. His prior start-up also made no money.

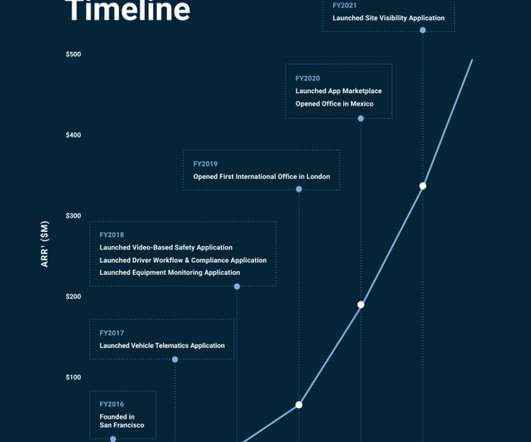

Everyone once in a while a startup just plain executes from Day 1. After 18 months building, things just took off when they launched, going from $0 in 2017 to an incredible $500m in ARR in 2021, in just 5 years. It doesn’t happen often, and it’s never quite as linear as it looks. That’s jaw-dropping. Wow Samsara !!

In December 2017, the amount raised in ICOs nearly equaled the amount raised by Series A investments globally. Startups can raise hundreds of millions of dollars on an idea. About a third of the ICOs in 2017 raised some form of institutional capital before ICO. The ICO market today bears many similarities to the dotcom era.

Prior to Creandum, Peter started his career at Lazada (South East Asia’s leading e-commerce player) and Paymill (payment startup). After some time in b2b marketing at Google and a few years at Bain & Company’s PE taskforce, Peter joined Creandum and the venture side in 2017.

With thousands of new startups emerging everyday and the average turnover rate for business applications trending at 39% annually, the SaaS industry couldn’t be more competitive. A 2017 U.S. When a startup is in its infancy, a founder may not be able to forecast exactly where the business will be in a year’s time.

He was also Coordinator and Trainer of startup sales at Gama Academy, the first sales training program for Brazilian startups. In 2017, he co-founded B2B Stack, a software review marketplace that boosts the buying process of B2B tech in Brazil. He’s been running SaaSholic, a blog where he writes about startups and SaaS.

Because, as she says, building a startup is simply much more fun. She has been around the globe, working in startups and digital agencies in Brazil, Germany, Southeast Asia, and Hong Kong. Diane is also passionate about everything startup, digital transformation in our lives, and psychology. The reason? Diny Gomes. Lisa Zhang.

Brex is a company that provides credit cards for startups, and Alloy provides financing for small businesses. Both Brex and Alloy have been mutual customers of one another since 2017 and in this session, they shared their lessons learned on balancing production innovation with regulation while mitigating risks.

We organize all of the trending information in your field so you don't have to. Join 80,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content