This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

And more importantly, revenue and user growth that is accelerating at scale. Lemkin (@jasonlk) May 22, 2025 The Early Days: Solving a Real Problem (2017-2018) Jacob Eiting and Miguel Carranza weren’t trying to build a unicorn when they started RevenueCat in 2017. By the time they raised their $1.5

in revenue. Then, in 2017, with around $50M in revenue, BILL added payment capabilities. When René’s dad had a payroll company, the rule of thumb was always one year’s worth of revenue, four quarters, because a customer lasted a year. Are We In a Downturn? There was an inflection point for BILL around 10k customers.

After the correction earlier this year, public valuation multiples had reset to those of 2017. That year, Cisco acquired AppDynamics for 17x trailing revenue. If we assume a company recognizes about 2/3 of its ARR as revenue, then I estimate the Adobe/Figma deal at roughly 75x trailing revenue.

Think your customers will pay more for data visualizations in your application? Five years ago they may have. But today, dashboards and visualizations have become table stakes. Discover which features will differentiate your application and maximize the ROI of your embedded analytics. Brought to you by Logi Analytics.

Most high-growth software investors value public companies on enterprise value to forward revenue multiple. But investors in private companies use a different metric, enterprise value to forward annual recurring revenue (ARR).The The public markets project revenue for the next 12 months. What conclusions could we draw?

(As you can see, I really like placeit.net :) ) In case you haven't started to think about your plan for 2017 yet, now's the time. Growth Calculator This little tool allows you to enter your MRR as of the end of 2016 and a target growth factor for 2017. If you're a long-time reader of this blog, you may have seen them before.

collectively, only about 160 companies meet basic IPO readiness criteria (>$100M revenue, >15% growth, >-25% EBITDA margin). Why It Matters : The report shows that VC investment has been highly correlated to rates, but in a moderate interest rate environment, rates will likely play a smaller role similar to 2017-2019.

Ultimately — revenue multiples. Revenue multiples are how much VCs, investors, and ultimately, an IPO and public markets will value each dollar of revenue. Revenue multiples don’t affect customers, or even revenue itself. pic.twitter.com/JNnzizB82v. — Byron Deeter (@bdeeter) May 5, 2022.

The problem with this train of thought: you’re missing out on revenue. At Intercom, we have learned that investing in real-time support, with response times under 5 minutes, can actually turn customer support into a revenue driver. We believe that this approach is counterproductive to a businesses’ revenue objectives.

. $500k+ deals make up half their revenue, and $1m deals 37%. $500k+ deals made up 41% of Braze’s revenue in 2021 and 2020, and $1m+ deals grew to 37% of their revenue, up from 25%. Still, Braze isn’t overly concentrated, with no customer being over 5% of their revenue. 40% of Revenue from Outside U.S.

It means it’s really, really hard to get revenues going. You close a customer for $120 in annualized revenue, you only get to recognize $10 of that a month. Tons of work, tiny revenues to start. Get the revenues going, even if they are small. 120% NRR: Your revenue doubles in 5 years even with no new customers.

One of the crowd favorites has been Mark Roberge, all the way back to 2017. 2017: How the Best Outbound Sales Teams Are Managed. Mark first joined us in a terrific panel session on how the top outbound teams are managed, 2018: Sales Mistakes that Can Kill Your SaaS Business How to Avoid Them. Ok, now a look back!

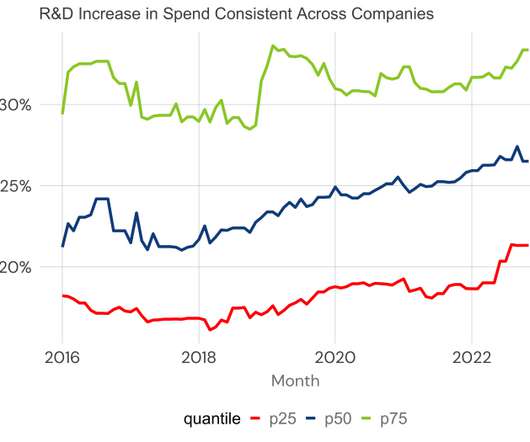

By prioritizing sales & marketing, the company successfully lengthened runway to increase revenue, which eased the subsequent fundraising. Actually, the opposite is true: software companies spend more on R&D (research & development) & less on Sales & Marketing (S&M) as a percent of revenue today than six years ago.

Certainly, public SaaS revenue multiples are way down, and that’s impacted many things, including making VC fundraising substantially harder than in the go-go days of 2021. Salesforce Growth: 2023 $31.8B (guidance) 2022 $26.5B 2021 $21.25B 2020 $17.1B 2014 $4.1B. Thank you Ohana! pic.twitter.com/CMhrBXgHSF.

But over time, it’s added a large enterprise and B2B component for marketers and others to track, manage and market videos that we’ll spend a bunch of time digging in on, as it’s the fastest-growing segment, growing from little-to-none in 2017 to 25% of revenue today. 50% of revenue outside the U.S.

Revenue grew nicely at first from $1m to $3.5m 2017: $30m rev. Customer count growing 33%, revenue growing 65% — the “Golden Ratio” for future growth. Fast, but revenue grew much faster (65%). That means both halves of the revenue engine are humming. ARR uses to mean true recurring revenues.

The second SaaStr post ever, way back in late 2012, was “ Everybody Lies: SaaS Revenues in the Inc. Let’s take a look back at where HubSpot, Upwork, and others were in 2011 GAAP revenue — and where they are today. Learnings for this year, for 2011 GAAP revenue (Inc. in 2011 GAAP revenue. generation.

(Note: I wrote a version of this in 2017 when times were good. Your second-order revenue engine still needs to work. Even if sales cycles have slowed down. Make sure that the $2m or $5m or $20m you ended the year with at least renews as a cohort, even if for not as much revenue as you’d planned. In the media.

Series A dollars provided the business 17 months’ of runway at constant burn assuming no revenue. Today, the public markets value companies like it’s 2017. In 2021, employment costs per capital increased to roughly $200k. At 28 employees, a $16m Series A fueled the company for 35 months. But we’re no longer in 2021.

Only 8% of Slack’s revenue last year was from direct conversion from Free to Paid — and that’s down from 10% the year before. Today, Slack has 575+ customers paying more than $100k a year, which important now accounts for 40%+ of its revenue. That’s way, way up from just 22% of revenue from $100k+ deals in 2017.

Today, just 2 years after that, Hubspot in a very similar space (just more SMB) and with very similar revenue, is worth $18B. First product doesn’t work, no revenue for 3 years. Worth $2B by 2017. And revenue has grown to $1B+ ARR for all the winners. That’s 18x. Shopify: Founded 2006. 2015 IPO at $1.27B.

Shopify’s first quarter revenue: Q1 2021: $989 million Q1 2020: $470 million Q1 2019: $321 million Q1 2018: $214 million Q1 2017: $127 million Q1 2016: $73 million Q1 2015: $37 million Q1 2014: $19 million Q1 2013: $9 million. Shopify doesn’t call its non-software revenue “MRR” A small but interesting note.

CEO Peter Gassner is truly of the most impressive founders I’ve personally met and you can take a look at our deep dive from SaaStr Annual 2017 here not long after they’d IPO’d: One of many remarkable things about Veeva: it burned about $3m on the way to IPO. Revenue has accelerated in 2021 — even at $2B in ARR.

The Rebrand That Changed Everything 2017’s pivot from dapulse to monday.com wasn’t just a name change. Product-Led Growth Before It Was Cool While others were building massive sales teams, Zinman pushed for a product that would sell itself. The result? ARR growth?

Free Cash Flow up from 3% of revenue at $400m in ARR to 10% at $550m in ARR. From $11m in annual revenue in 2017 to $500m+ in 2022. 50k+ customers are 26% of revenue today, and 10+ seat deals are 76%. Still, a quarter of their revenue is still from smaller customers. And a few other interesting learnings: #6.

Different accounting rules govern revenue & cost recognition. In 2017, the industry migrated from ASC 605 to ASC 606, which are financial arcana as esoteric as it reads. If that argument is correct, then the average gross margin of a software company in the public domain would fall from 72% to 47%. Quite a stark difference.

First $100k customer in 2017. GitLab’s SaaS revenues are still just 20% of their revenues, although that’s up from 9% in 2020. GitLab China is a new independent company formed in 2021, both SaaS and self-managed, available only in China, Hong Kong and Macau. We may see this more often. #4. Then 20 by 2018.

Five months into 2017 nine venture-backed technology companies have gone public compared to 14 in 2016. Snap grew revenues by nearly 6x annually. The IPO market in 2017 seems to be very healthy and is on pace to be twice as active as last year. The other seven have demonstrated the broad public investor demand for new offerings.

Bookings, MRR, Revenue. For as long as SaaS companies have existed, we’ve used one way of counting revenue, called GAAP. Starting in 2017, revenue recognition for SaaS companies will change, and SaaS startups will have more flexibility in the way they record revenue than in the past. I am not an accountant.

They had revenue their first month after launch. His learning: follow your customers. The Slack story is incredible, but most of us need to focus on getting to revenue very early. Finally, the session we did with Jeff at the 2017 SaaStr Annual right after Twilio’s IPO was incredible. But the customers started coming.

90% of revenue originates through self serve channels - an astounding figure for company that generated more than $1B in revenue last year. Dropbox’s revenue grew from $604M to $1.1B from 2015 to 2017, a compound annual growth rate of 35%. Revenue Growth. MC/2017 Rev Multiple. Gross Margin. Market Cap.

growth-adjusted revenue multiples. And BVP’s very helpful inclusion of growth adjusted revenue multiples in their deck supports that: At first glance – with a 180% increase in this metric since 2017 – it would be yet another reinforcement of the “investors are nuts” talking point.

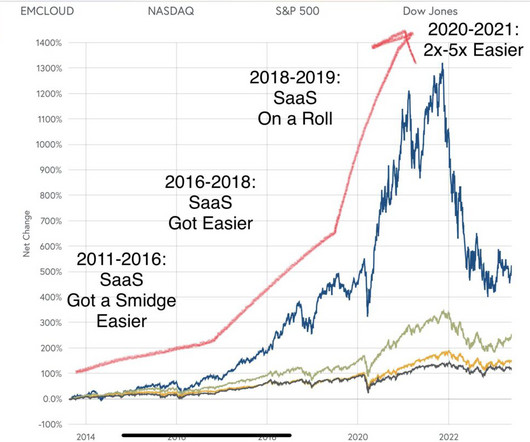

Each year from 2017-2021 was easier than the prior year. Revenue multiples for public SaaS companies in 2023 IMHO are still too low. Now we have a whole generation of SaaS employees and execs who have only seen SaaS. Get Easier Every Year. 2022 was harder, but it took a while to see it wasn’t transitory.

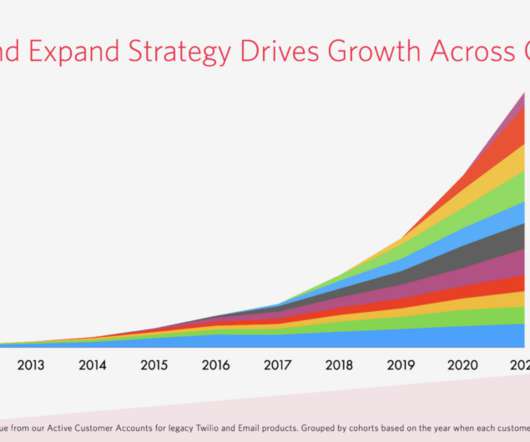

International Revenue up to 34%, from 29% in 2019. A third of their revenue in now outside the U.S. #4. Messaging now just half their revenue. We talked with CEO Jeff Lawson below way back in 2017 about how to go multi-product. We talked with CEO Jeff Lawson below way back in 2017 about how to go multi-product.

$5k+ customers are now 73% of revenue — up from 62% in 2021. Still, it’s impressive that even at $600m+ ARR, 27% of their revenue still comes from customers that pay less than $5k … That’s a long tail that truly has gone the distance. #4. 39% of Revenue Outside U.S., 39% of Revenue Outside U.S.,

And another great deep dive with Eric on the First $100,000,000 in revenues here: And the latest on Zoom at $4.3 Billion in revenue here: 5 Interesting Learnings from Zoom at $4.7 This dedication to user experience helped shape Zoom into a more user-friendly platform than its competitors.

Last week we had a great one with Robby Allen, Chief Revenue Officer at AgentSync, check it out here. In 2017, he was named by LinkedIn as one of the top 5 CMOs in the world to follow for thought-leadership in the digital marketing domain. I always learn a lot from these — they are in essence a best practices list from each leader.

One of the clearest examples of how lopsided the services-to-software dynamic can be is from Mulesoft’s S1 filing in 2017. The incremental market cap created by this shift could be enormous, as more revenue is reclassified into higher-multiple software categories rather than lower-multiple services categories. Bucketed by Growth.

This led to our first meet-ups in 2013 and 2014, the first SaaStr Annual in 2015 , the industry’s leading podcast in 2016, the first SaaS founder coworking space in 2017, and SaaStr Pro , the first learning management system for SaaS founders in 2018. Revenue leaders were able to network once again. Now a staple!)

You have to be scrappy at this stage, and Braze was trying to find product market fit with no product, no revenue, and no customers. This was around 2017, and CS became simpler and focused on post-sales, retention, and reduced churn. This revenue chart is 2017-2021 before Braze IPO’d.

Up until say 2017–2018 or so, in SaaS, there was a rough rule: a relatively small amount of secondary liquidity ($1m-$2m) would be offered by growth investors in top VC rounds once a startup crossed $10m ARR or so. They bootstrapped themselves to tens of millions in profitable revenue, and then sold a big chunk of founder secondary.

Revenue growth accelerated from 32% to 41% * And new customer growth accelerated to a crazy 45% YoY * All while keeping ACVs constant at ~10k. Hubspot didn't just grow an incredible 41% in Q1'21 to $1.1B It accelerated. They did it the hard way, with SMBs. — Jason BeKind Lemkin (@jasonlk) May 6, 2021. Seize the day. 2014 $4.1B.

GAAP revenue in Q1 ’19) because it’s in a space filled with strong competitors. It’s an almost 100% enterprise play — they have 227 customers spending over $100k a year, comprising 84% of their revenues. Revenue doesn’t all have to be recurring, folks. 130%+ revenue retention. The lesson?

We organize all of the trending information in your field so you don't have to. Join 80,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content