This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Replit’s Dramatic Transformation: From Stagnant to Stratospheric The Dark Years (2016-2023): Building in the Desert Replit’s story begins like many overnight successes—with years of grinding in obscurity.

The Platform Play (2010-2016): Expanding Beyond Core Use Case Market Cap Journey: ~$10B → $50B This is where NVIDIA showed true platform genius. The AI Bet (2016-2020): Riding the Massive Wave Market Cap Journey: $50B → $323B Here’s where timing met preparation. Key Lesson : Don’t just solve the immediate problem.

The top quartile companies are growing at slower rates today than the bottom quartile companies in 2016. There are few, fast growing, younger SaaS companies to sustain the growth rates. The median has never been lower in the last ten years.

In 2016, Mastodon , an open-source and decentralized microblogging platform, was launched. Despite initial excitement and a successful crowdfunding campaign, Diaspora struggled to gain mainstream traction. Their platform still exists and currently has around 850,000 users.

Conquest Numbers Let’s separate the happy convergence talk from the harsh conquest reality: SaaS: The Steady Performer Under Siege $295 billion market in 2025 with 18.4% growth rate vs.

Frank, MZ & Shen, T 2016, ‘Investment and the weighted average cost of capital’, Journal of Financial Economics , vol. Militaru, I 2016, ‘UTILITY OF NET PRESENT VALUE (NPV) FOR FIRMS IN TODAY’S ECONOMY’, Romanian Economic and Business Review, vol. 2471-2511, DOI:10.1111/jofi.12110. 2015.09.001.

By 2016, Procore was a multi-product, multi-stakeholder platform expanding into enterprise and mixed-use construction firms. We lost nearly every customer, Tooey admits. But the companies that survived the recessionmixed-use and commercial buildersbecame Procores new focus. That pivot paid off.

Over the years, BetterCloud has evolved to become multi-SaaS (2016), included no-code automation (2020), acquired best-in-class SaaS Spend Management tool, and constantly evolve BetterCloud to meet the needs of todays IT professionals. Eduardo R.,

Check out the 2023 , 2022 , 2021 , 2020 , 2019 , 2018 , 2017 , and 2016 posts. To everyone in SaaS (and especially our incredible customers): heres to a productive, profitable close to 2024 💪 The future looks brightand I can’t wait to see what we build together.

I’m like, do you really think call recording was sexy in 2016 when I came in? Udi Ledergor: So, you know, I hear that a lot. Uh, people come to me and say, oh, UDI, well it was easy for you. You worked at a company so sexy like gong. You think that was sexy?

Notion has been working on this together since 2016, and has customers like OpenAI, Toyota, Figma, Ramp, and thousands more on this journey with us. Computers may be our most powerful tools, but most of us can’t build or modify the software we use on them every day. At Notion, they want to change this with focus, design, and craft.

When the first oeksound plugin, Soothe, was created in 2016, creator Olli Keskinen and his friend Hannes Andersson were studying music technology to become recording engineers. But yeah, that was all made by one person in November, 2016. Anything is by different, by like start by default, it is global.

At least one domain controller must be running Windows Server 2016 for advanced features like Windows Hello for Business. All user domains must be trusted by the domain where the ADFS servers reside. The ADFS service account needs read access to user attributes across all trusted domains and forests.

Uh, from segment because I don’t know if you remember, but in 2016, you probably signed up for the, the segment startup program and that credit is about to expire based on your traffic and our analysis of [00:10:00] segments, current pricing, you’re going to have to pay about 62, 000.

Before that, he was the CEO and Co-Founder of DataHug, which was acquired by Calidus Cloud in 2016. More for your eardrums Ray Smith is the VP of AI Agents at Microsoft. Previously, he was the Global VP of Product for SAP, CRM and Sales Cloud.

Before that, he was the CEO and Co-Founder of DataHug, which was acquired by Calidus Cloud in 2016. And before that he was the CEO and co-founder of DataHug, which was acquired by Calidus cloud in 2016. Previously, he was the Global VP of Product for SAP, CRM and Sales Cloud. I mean, moonshot projects sound pretty fun.

Before that, he was the CEO and Co-Founder of DataHug, which was acquired by Calidus Cloud in 2016. More for your eardrums Ray Smith is the VP of AI Agents at Microsoft. Previously, he was the Global VP of Product for SAP, CRM and Sales Cloud.

And then the “Flash Crash” of 2016 came, our first big hit. I did a deeper dive on SaaS multiples, and what that means for founders and SaaS execs, below at SaaStr APAC: The post The Three Valuation Lows in SaaS: 2013, 2016, and 2022 appeared first on SaaStr. It was just too hard to make money at 4x ARR.

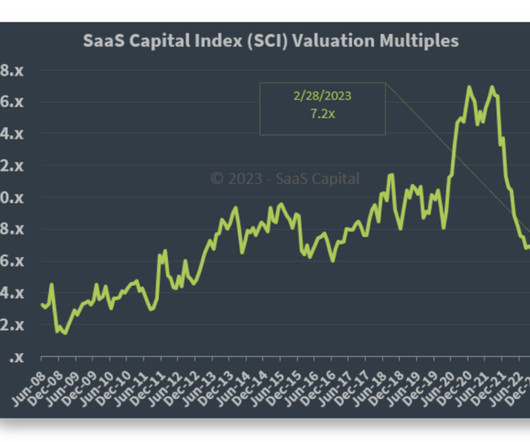

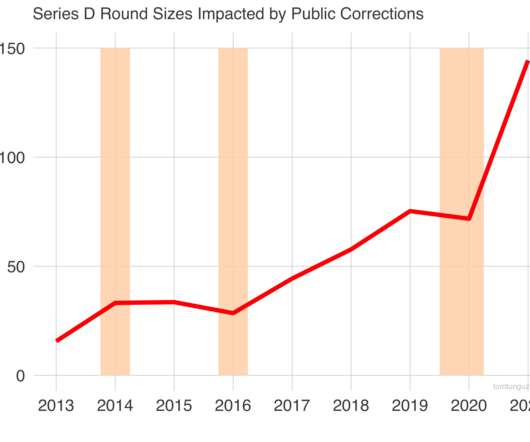

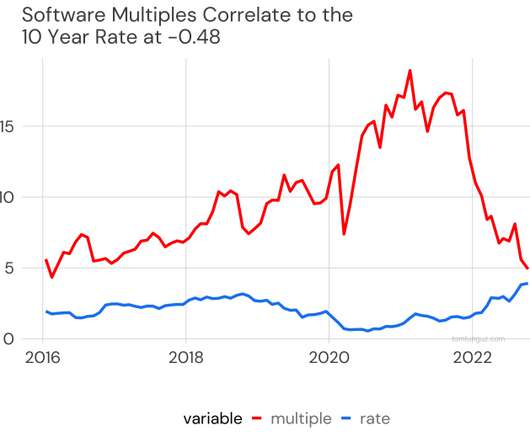

Since 2016, public software has witnessed four corrections. Also, 2014 to 2016 saw a 57% reduction in multiples and of course after 2008. In fact, the 75th percentile multiple has appreciated 25% annually since 2016 and the median has increased by approximately 20%. Today, we’re in the midst of the fifth. Correction Year.

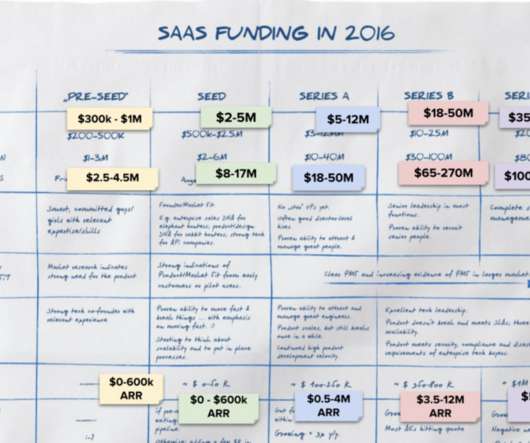

What began as a blog post in 2016 has evolved into a yearly exploration and survey to founders and investors to discover what it really takes to raise capital for SaaS companies. The Evolution of SaaS Funding From 2016 to 2021. Originally, in 2016, Point 9 measured MRR, but they have since changed their focus to ARR).

Only the 2016 reduction of 57% surpasses it. 2014’s correction stalled and then reversed Series D round sizes for 2 years through the second correction in 2016. The public software sector is weathering the second deepest multiple contraction in the last decade. These are marked in peachpuff orange rectangles above.

So Microsoft announced that LinkedIn, which it bought in 2016, has now crossed a stunning $10 Billion in ARR — and growing 27% year-over-year. Revenue tripled since Microsoft acquisition in 2016. Members “only” up 70%, while revenue up 300% since 2016. LinkedIn sold to Microsoft in 2016 for $26B.

from 2015 to 2016 … and then exploded: UIPath History. 2016: $3.5m Top 50 customers grew bookings 81x since 2016, and all 2016 customers together grew 57x. These 2016 customers really leaned in on UiPath. And then after a decade … it started to come together. 2014: $500k rev. seed round. 2015: $1m rev.

Enterprise-value-to-forward-revenue multiples are now below 2016 levels for the first time in 6 in years. It happened in Feburary 2016. The public software market continues to compress. The 25th percentile of companies trade at 3.3x today compared to 4.0x The median or 50th percentile trade at 4.9x Would it be crazy to see 3.3x

100k+ customers have gone from 50% of revenue in 2016 to almost 80% today: #2. From 2 $1m ARR customers in 2016 to 145 today. $100k+ customers are key to ARR growth. Datadog isn’t leaving the smaller customers behind, but they are increasingly a smaller percentage of revenue. More product, more products, more products.

Let’s go back in time … to early 2016. At SaaStr Annual 2016, in February, all the VCs were discouraged. “Unicorns are over,” they said. Just like Marketo was in the 2016 downturn. A sign many of those with the biggest checkbooks in SaaS think things will get substantially better. No way, you say?

In 2014, 2016, 2020, 2021, these big mergers drove the figures into the tens of billions. X 2015 20.1% - 2016 43.0% Multi-billion dollar acquisitions, the blue bars, are the largest contributors to this swing. It’s no surprise that in those years, the biggest acquisitions accounted for more than 53% of dollars on average.

January 2016, SaaS stocks were riding high. It was called 2016: * Everyone panicked * Seemed like multiples would never recover * LinkedIn sold to Microsoft for 7x ARR. That revenue multiples should rise from where they were in 2019. But I’m hardly sure this will happen in practice. And remember, we’ve seen this all before.

2016 was tough, too. But the markets also dropped 50% at the start of 2016, and VCs panicked. It was called 2016: * Everyone panicked * Seemed like multiples would never recover * LinkedIn sold to Microsoft for 7x ARR. There are enough good investors out there. — Jyoti Bansal (@jyotibansalsf) May 6, 2022. #6. And then ….

Since 2016, the average public software witnessed its sales efficiency winnowed from 52% to 47%, a decline of about 10%. Third, those lows touch the highs of the next rung down; i.e., the current levels of the 75th percentile companies’ sales efficiency is equal to the 50th percentile companies in 2016. What happened?

In other words, if machine learning startups raised the same amount of money in 2016 is 2010, the chart would show a value of 1. Advertising technology has seen a resurgence in 2016, reversing a three year trend of declines. There are fewer software startups raising capital in 2016 than 2015.

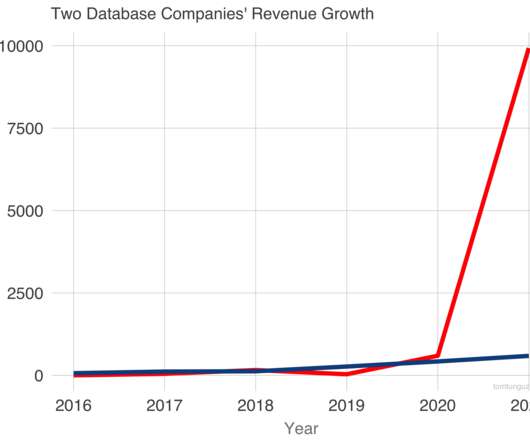

In 2016, each company recorded less than $50m in revenue. Both have grown very fast. In fact, their revenue trajectories through 2020 are nearly identical. Both companies employ a usage-based pricing model: pay for what you use. In two years, both would near $200m in revenue. They would both exceed $400m in 2020.

2016: IPO at $1.15B market cap. And yes, no one could have predicted the run we’ve seen in Cloud in the past few years. But take a look at these examples: Marketo (and Hubspot): Founded 2006. Marketo IPO’s in 2013 at $700m market cap. Vista buys Marketo for $1.8B A little more than 2 years later, it was resold for $4.75B to Adobe.

Cloud has been on an incredible tear since 2012 or so, and then even more since about 2016, and then as you can see above, went into hyperdive in about 2018 … and then into true warp speed after Covid. Yes, the markets have retreated a bit from their all-time highs. But does it even matter? SaaS and Cloud are up +1000% since 2013.

The chart above shows the median enterprise value to forward ARR value since 2016. To estimate ARR for a public company, we annualize the analyst consensus estimates for the revenue 4 quarters from today. It hovers around 5x until 2018, then spikes to 8x, and despite some volatility, reaches its current zenith at a bit more than 10x.

In less earth shattering news, the fact that it's 2017 also means that my "SaaS Funding in 2016" napkin needs an update. As a reminder, in the original post I tried to give a "back of a napkin" answer to this question: What does it take to raise capital, in SaaS, in 2016?

Well, if it were 2016, we’d say no. Bill.com is one of my favorite sleeper SaaS companies. Half of its revenues comes from its software. And half from fees on transactions it processes: Is this all really ARR? But it isn’t. With an incredible 121% NRR from SMBs, it all essentially recurs. Only half does.

It’s not slowing down Salesforce, Snowflake, or almost any other SaaS or Cloud leader. Salesforce Growth: 2023 $31.8B (guidance) 2022 $26.5B 2021 $21.25B 2020 $17.1B 2014 $4.1B. Thank you Ohana! pic.twitter.com/CMhrBXgHSF. — Marc Benioff (@Benioff) May 31, 2022. We may be headed for a big downturn, we’ll see.

2016: Dharmesh joined us for the first time, with one of the most engaging and highly-rated SaaStr Annual session on ever: their journey to IP O. In the run-up to SaaStr Annual 2022 on September 13-15 , we wanted to look back at some of the highest-rated SaaStr sessions of all time, since the first SaaStr Annual in 2015.

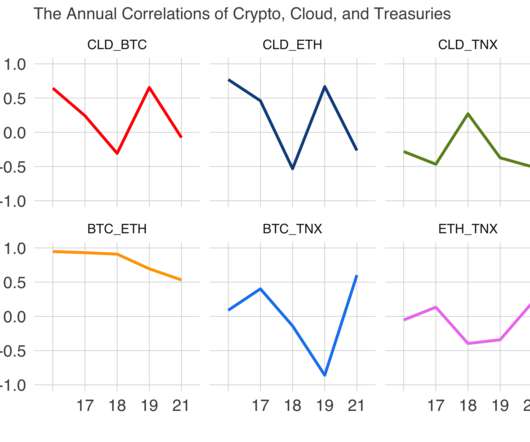

BTC and ETC moved more or less in synchrony from 2016 to 2018. Economics students would argue the discounted cash flow model predicts this behavior. Companies with profits in future years should be less valuable during times of higher interest rates. Three years ago, they went their separate ways.

Automattic was started in 2005 to democratize publishing, and WooCommerce was purchased in 2016 to democratize e-commerce. When WordPress purchased WooCommerce in 2016, they believed it would become their biggest business. Now, Woo is an open-source style Shopify and their largest business. Then, in 2023, they moved into messaging.

We organize all of the trending information in your field so you don't have to. Join 80,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content