This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

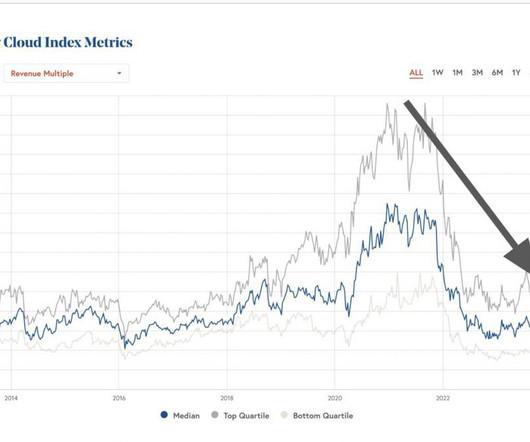

There’s a lot of great data in the report, but one analysis helped answered a question I’ve been wondering the past 12-18 months: Are start-up actually more overvalued today than at the peak of Cloud mania in 2021? Because valuations are as high as ever, and yet … public software multiples are far, far, far lower than 2021.

And what you can see is there is really almost no liquidity for startups and scale-ups in SaaS and Cloud at the moment. And there hasn’t been for a while: It was great times for SaaS liquidity in late 2020 through the end of 2021. And 2021 was a record year for Saas IPOs. Epic times. Liquidity was everywhere.

And for many in SaaS, especially those that sell mainly to startups and tech, it’s often been a rough 2 years. Well, the best in SaaS and venture and Cloud are not just still growing at epic rates, but they’re acquiring so much funding … they can still run the 2021 playbook. So can you pay less these days?

4 Truly Great SaaS IPOs Since 2021! How To Perfectly Pitch Your Seed Stage Startup With Y Combinator’s Michael Seibel #4. We Just Left a Vendor Weve Used for 5+ Years. They Dont Even Know It Yet. #3. How Many Sales Reps You Really Need for Next Year #4. Is SaaS Back? (TL;DR: TL;DR: It Sure Feels Like It) #5.

Let’s all be clear, 2021 was insane: * SPACs worth billions with no revenue * Multiples magically tripled * Fintechs with 10% GMs worth same as 80% GMs * #5 in market got same premium as #1 * Growth stage seen as free money * Seed VCs bought in $3B-10B rounds vs sell. High Burn rate SaaS startups will still exist, but they will be much rarer.

In 2021, they were often worth 40x revenue. And it also makes it harder to meet the “ask” of a startup that might want a much higher revenue multiple. Revenues Multiples Are Down Even the best public SaaS companies are worth ~10x revenue today. When times are really good, more deals get done.

Is your B2B startup now part of the past … because it was founded before 2023? VCs especially are obsessed with AI-native startups. When I talk to founders who launched in 2020 or 2021, I hear the same anxiety: “Are we already legacy?” No one’s coming to save you. It’s not too late. We are early.

Battery Ventures: Startups Are Actually Far More Overvalued Now Than in 2021 #3. Top Posts: #1. 83% of You Haven’t Gotten AI SDRs to Work — Yet #2. The Arguments For Not Raising at a Unicorn Valuation #4. 5 Interesting Learnings from ServiceTitan at $700,000,000 in ARR #5. Carta: 43.6%

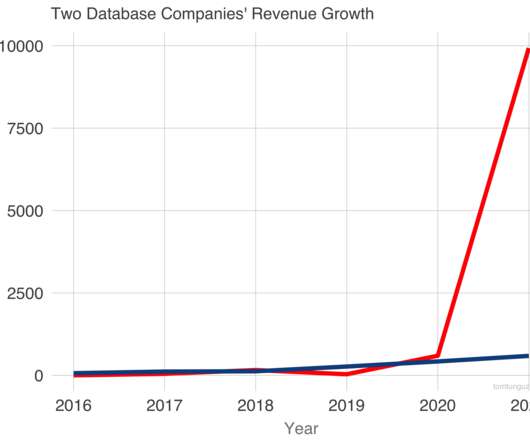

I’m going to tell you a bit about two startups and I’d like you to guess the name of each company. Both startups provide database software to developers to build applications. But here the stories diverge in 2021. Both of these businesses are publicly traded. Both have grown very fast. Red Company. Blue Company.

So that’s a wrap on SaaStr Annual 2021, #007. — Jason BeKind Lemkin (@jasonlk) September 30, 2021. We had as many attendees in 2021 as 2019, and 55% of the SaaStr community couldn’t come (Europe, Australia, NZ, etc) for visa issues alone Get ready for an epic 2022. #2. — D Sharp (@djdsharp) October 1, 2021.

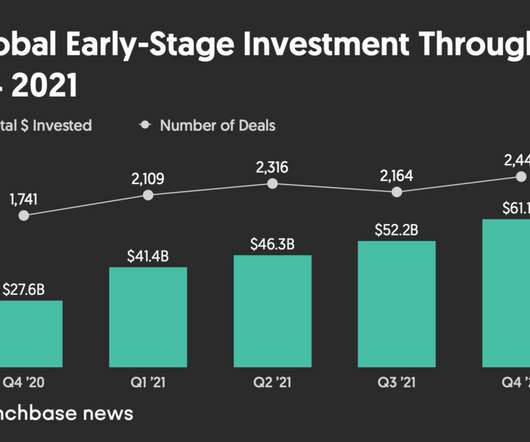

Everyone has slightly different data, but it helps answer a seeming conflict in the VC markets: Massive amounts of funding have flowed into startups … and yet … Why doesn’t it seem easier to raise seed funding for many startups? So net net: Global VC investment doubled in 2021 from 2020, from $335B to $643B; and.

It’s time to Meet Your Mentors for SaaStr Annual 2021! To help facilitate meetings between up-and-coming startups with top VCs, we’re bringing back our super popular Meet a VC program. We have hundreds of investors joining us for SaaStr Annual 2021, not to mention hundreds of post-revenue startups.

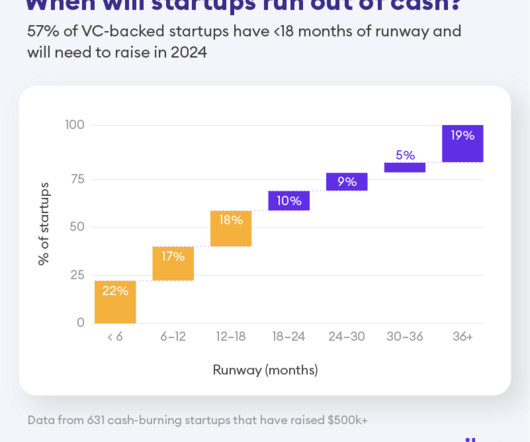

SaaS products and services like Pilot track the finances of 1,000s of SaaS and other startup so they’re an interesting source of hard data. Something that’s both not surprising but also pretty impactful: 57% of venture-backed startups will have to go “back to market” in 2024 to raise more capital. Carpe Diem.

About 20%-25% are growing like it’s 2021. The post Maybe Only 10%-15% of VC Backed Startups Can Raise Another Round Right Now appeared first on SaaStr. And at the growth stage, top decile may not even be enough to raise another round. This is roughly what I see in my own portfolio at SaaStr Fund. Ask your existing investors.

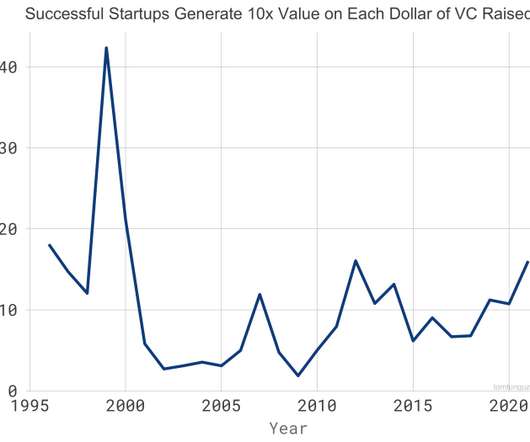

How much value does a successful software startup create per dollar of venture investment? Over the last 30 years, a venture dollar invested in a successful US software startup generated $10 of value. In 2021, the figure topped 15 for the first time in ten years. Startups in the 90s raised less than $10m.

returns from VC + PE in 2021 pic.twitter.com/ZSjfFQMXYh. So 2021 was a crazy year for venture capital, topping 1,000 unicorns and an IPO-a-day. Very well for top Limited Partners (“LPs”), the folks that invest in VC funds, and give them the capital to invest in startups. And they had an incredible year.

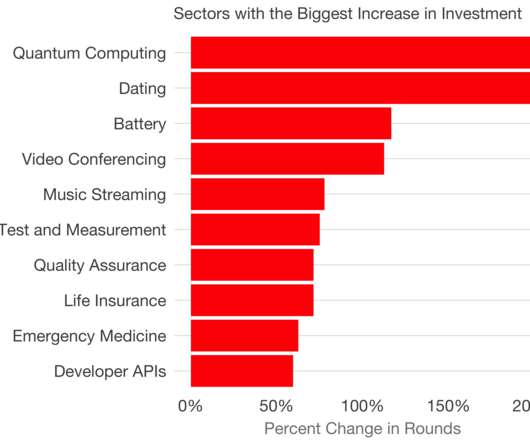

From time to time, I chart the fastest growing categories of startup investment in the US for seed through Series C. I analyzed Crunchbase data and looked for the startup categories that grew fastest in terms of funding rounds year-over-year, provided there were at least 10 rounds in that category.

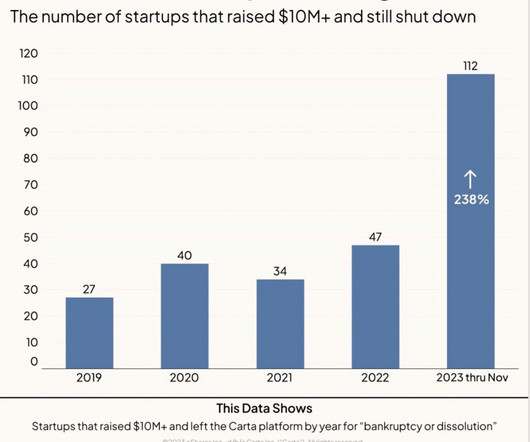

But for many startups, the hangover from the Excesses of 2021 is a real and tough one. Startups shutting down are up 238% this year — already. So, so many SaaS startups got funded in the Boom, and they just can’t all make it. And the latest Carta data here supports that. Now it sort of has to be that way.

A lot of our SaaS older times don’t quite know what to make with a lot of B2B startups these days, let alone some public SaaS companies. So many startups these days are claiming they have “ARR” from revenue that … doesn’t recur. In 2021+, Yes. Doesn’t ARR stand for Annual Recurring Revenue?

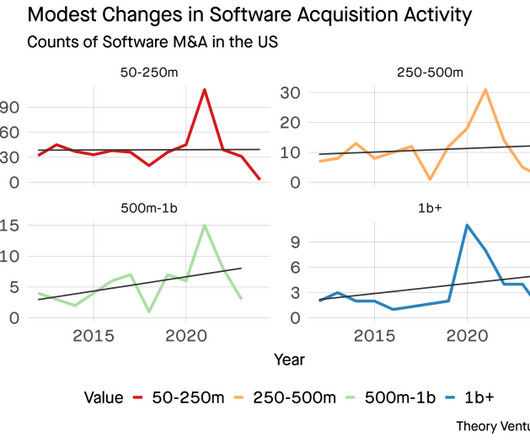

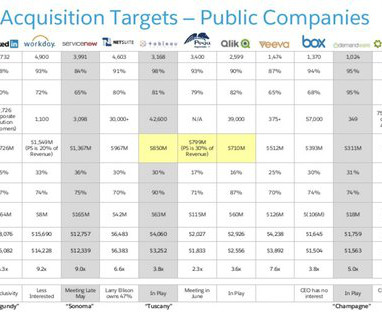

What drives the acquisition market of startups? In 2014, 2016, 2020, 2021, these big mergers drove the figures into the tens of billions. X 2021 43.8% It’s the big deals. In the last decade, the total number of venture backed software M&A by count has remained relatively constant. X 2015 20.1% - 2016 43.0%

Per Pitchbook and IVP, top-tier growth rounds had a 114x ARR ask at the very peak in 2021! Average asks and multiple for the very, very SaaS companies went up 700% in the Boom from late 2020-late 2021. We’re never “going back” to how things were in late 2020 and 2021. It Was 114x in 2021.

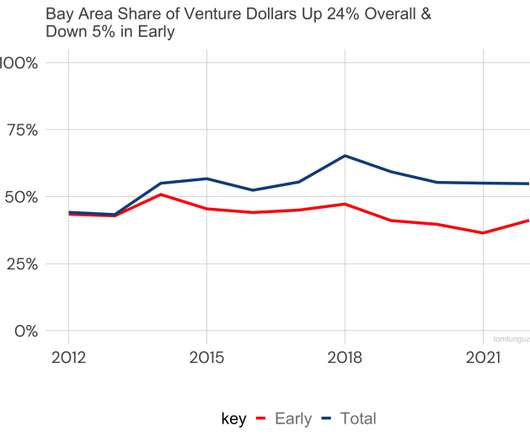

There’s a prevailing narrative that the health of the Bay Area startup ecosystem faces challenges. San Francisco’s share of startup rounds by count has fallen from its perch ten years ago. In 2021, San Francisco Bay Area startups raised $126b. In 2019, US startups raised $126.4b.

And make sure you have your team’s tickets to SaaStr Annual 2021 — you can’t meet the VCs if tickets sell out before you’ve purchased them! Here’s your early peek at the list of SaaS venture capitalists and investment firms already signed up for 2021… (and we all know VCs rarely plan this far out!).

But what about startups? Most VC funds “carry” startup investments at their last round price, unless their value has been materially impaired. So that 100x unicorn round that closed in 2021? Even if the startup isn’t quite a rocketship anymore, most smaller VC funds will stay hold it at the same value. Well, sort of.

The overwhelming participation by both Founders and Investors at the upcoming SaaStr Annual 2021 exemplifies this. After “Founder Confidential” ends, emerging SaaS startups network in person with leading VCs in our CoWorking area as part of our “ Meet A VC ” program. . Startup Advice”. No VCs are invited. We raised our $2.8m

Dear SaaStr: When Should a CEO Tell Startup Employees That The Company Is Going Under? It’s more common these days than in the past, given all the explosion of capital in 2020-2021 … into startups that aren’t going to make it. Everyone knows in a startup, even a big one. I almost did. But I never did.

Hang around startups & venture capital long enough, & you’ll hear this aphorism. In any given year, there’s an 82% chance the value of startup liquidity will change by more than 77% - both up & down. In 2021, the sun shone brilliantly. Companies aren’t bought. They’re sold.

billion Valuation in May 2021 and But Is Now Being Acquired by Atlassian for $975 Million? Great outcomes, but at lower than the peak 2021 prices. Valuations were much, much higher in 2021 than they are today. So high, in fact, that many acquirers will basically ignore those 2021 valuations, more or less.

That’s a wrap on SaaStr Money 2021 ! Fundraising for a Startup vs Fundraising for Banks with Treasury Prime’s CEO and Piermont Bank. Next up — SaaStr Annual 2021 in SF Bay Area, Sep 27-29! The post Catch Up on the Top Sessions from SaaStr Money 2021!! Quite a day! appeared first on SaaStr.

You need startup folks to succeed at a startup. Many startup folks have no idea how to work at scale. — Jason BeKind Lemkin (@jasonlk) August 25, 2021. It’s a reminder the same is true of SaaS startups. Folks that know startups, and what it takes to put those initial points on the board.

The US startup M&A market in Q4 2022 was one of the quietest in the last 20 years. in Q4 2021 to a paltry $2.1b During a down-market, young startups who face a radically more challenging fundraising market than six months ago more often choose a quick sale. US venture-backed M&A fell from $34.6b in Q4 2022.

The last IPO of the 2020-2021 era was HashiCorp in December 2021. The best leaders have experience with both startups and scale to navigate the in-between. The ideal leadership hire is someone who has seen both startups and scale. And it’s one of the first to be acquired! IBM just closed on its $6.4

Q: What are the top startup lessons we learned during Covid? A few lessons that maybe weren’t new, but they we relearned in 2020-2021: Things always bounce back. Shopify and upstarts like Gorgias used this to power ahead in tough times: Anytime is a great time to start a startup. It’s just never clear how long it takes.

If as a VC you invested at $10m pre initially, and say it’s 2021 and that same startup is doing a 100x round at a $300m valuation, this early VC fund can pick and choose whether to invest more or not. The post Every Venture Backed Startup is Now Competing for Reserves appeared first on SaaStr. Just ask. No one asks.

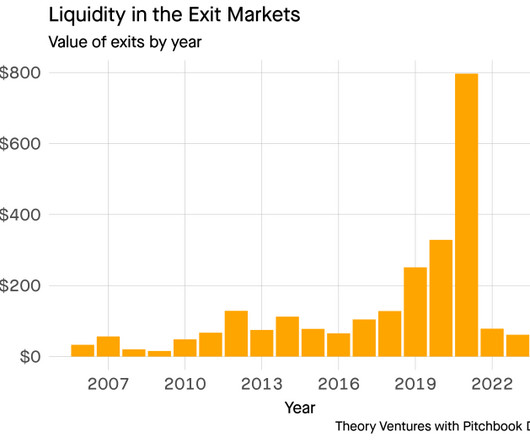

As you can see below, liquidity last year was down 50% from the historical average of the past 10 years, and way, way down from the crazy 2021 peak: Now to some extent, this is to be expects. Private Equity overall and Venture Capital in particular had an insane amount of “exits” for high dollar amounts in 2021. It will bounce back.

From startup to $500M CARR, Spencer Burke, SVP of Growth at Braze, shares how Braze scaled a growth and customer success team. As an early startup team, you’re doing every job under the sun. We get lazy writing job descriptions, and taking shortcuts is a luxury most startups don’t have. Braze went public in November 2021.

So my LinkedIn feed is full of sales execs complaining how unfair startups are: VPs get fired seemingly without cause (it’s never that simple, though. Startups not even hitting 40% quota attainmen t (more common these days, and brutal indeed). VC-backed startups can be an incredible journey. Is this fair? Perhaps not.

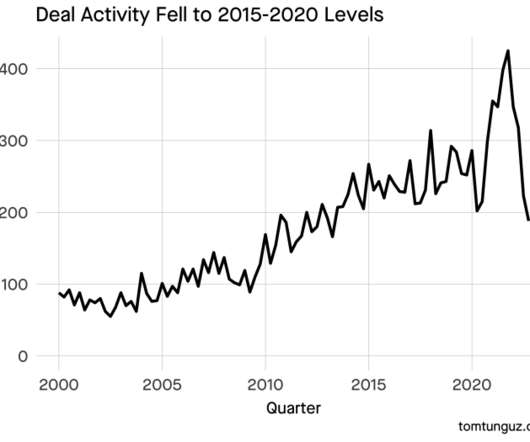

Current State of Early-Stage Venture Market The early-stage venture landscape has experienced significant shifts since the peaks of 2021. We’re seeing: Deal activity decline : From the highs of 2021 (around 3.5B raised in Q4 2021), we’re seeing a return to baseline levels but still below pre-zero interest rate era volumes.

Dear SaaStr: Dear SaaStr: What Were Aspects of Your Startup That Were Easier Than Anticipated? — Jason Be Kind Lemkin (@jasonlk) April 20, 2021. — Jason Be Kind Lemkin (@jasonlk) April 20, 2021. More here : The post Dear SaaStr: What Were Aspects of Your Startup That Were Easier Than Anticipated?

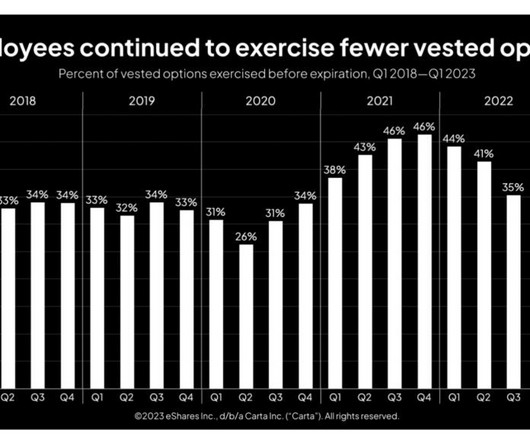

So Carta recently put together some dat a on a topic I’ve wondered about: just how many startups allow option exercises beyond the traditional 90 day window? The answer: the general trend is just over 10% of startups have extended windows beyond the traditional 90 days for departing employees to exercise stock options.

Back in 2021 though, Ramp was just 2 years in — but already experiencing hypergrowth. In 2014, Atiyah co-founded Parabus, a consumer-focused startup that automatically secured refunds when prices dropped on online purchases. Ramp just closed a stunning round at a $15 Billion valuation!

. “You grow into the big, bloated company once you stop being a startup” This talk I gave at Web Summit 2021 is about pushing back against that. Here, I dive into how to remain a startup, what to look out for as you scale, and how to grow up without growing old. The key takeaway?

Dear SaaStr: Do Late Stage Startups Prefer to Get Acquired or Go Public? When it was literally an IPO a Day in 2021, it seemed almost easy. It Was an IPO-a-Day in 2021. It really varies. Especially these days, when the IPO markets are closed. And today — it seems so far from easy. appeared first on SaaStr.

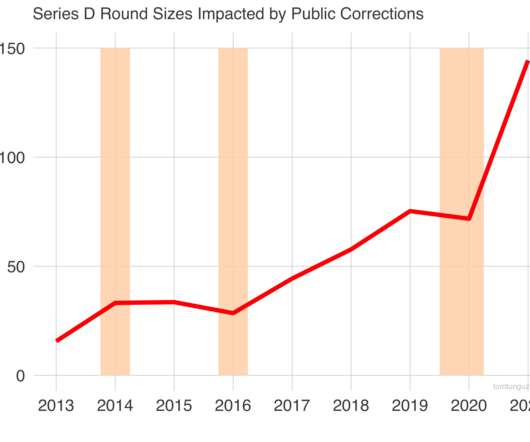

Ds doubled in 18 months starting in 2016, and again doubled from $75m to $150m in 2020-2021 - so the growth has been steeper on the way up and that may suggest a more sudden correction on the other side of the peak. Corrections may subdue the growth rates, but haven’t reversed them in the past.

We organize all of the trending information in your field so you don't have to. Join 80,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content