This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

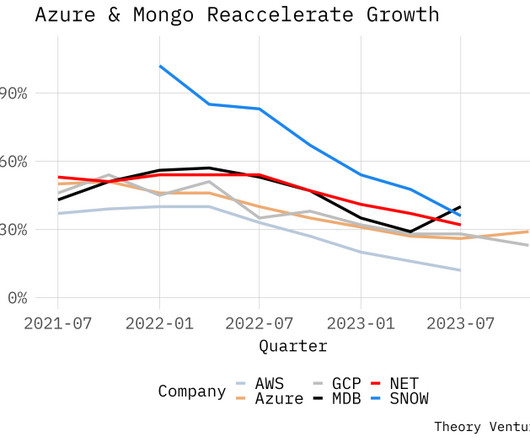

Q1 ‘25 earnings season for cloud businesses is now behind us. And no, this wasn’t all because of leap year last year (that would only account for a ~3% delta at most) The Hyperscalers (AWS, Azure, Google Cloud) also declined net new adds year over year, but not by as much. Net new ARR added was down 28% from Q1 last year.

Down nearly 30% YoY from Q1 last year pic.twitter.com/9MLyLe3XXf — Jamin Ball (@jaminball) June 5, 2025 Bottom Line Up Front : The aggregate cloud software market just delivered its worst quarterly performance in years, with net new ARR additions plummeting nearly 30% year-over-year in Q1 2025. billion in Q1 2025 , down from $2.33

Why 40% Cloud Adoption Marks the End of Easy Growth. The 40% Tipping Point : With 40% of workloads now in the cloud, SaaS has hit market maturity. If you’re not top 2-3 in your category, prepare for acquisition, find a defensible niche, or pivot to less mature markets.

Q: Which merger and acquisition trends, if any, do you expect to unfold in the next 12 months? These are the Best of Time in Cloud and SaaS, as odd as that still seems. If you are worth $20b-$1T+, you often don’t want to wait for a small acquisition or internal initiative to bear fruit. And you pay up to get it.

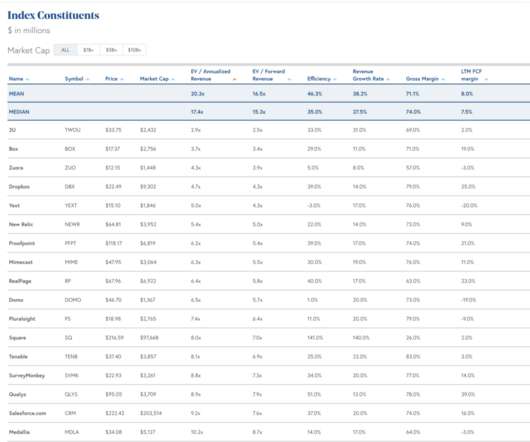

He summarized the M&A (acquisitions) of The Top 10 Software Acquirers. And what you can see is there is really almost no liquidity for startups and scale-ups in SaaS and Cloud at the moment. Public SaaS and Cloud companies, and AI leaders like NVidia, have still generated a lot of cash for shares. years or so.

Every year, Bessemer Venture Partners releases a State of the Cloud report. This year, it’s all about AI, which is why Sameer Dholakia, Partner at Bessemer, calls it the Cloud AI Era. Four portfolio companies join Sameer to talk about three trends of the Cloud AI Era. Like we’re all here at SaaStr in Cloud.

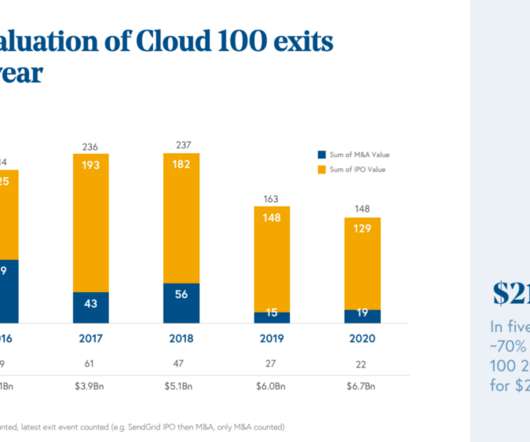

So Bloomberg and CB Insights have the latest data out on start-ups getting acquired, and 2025 is off to a record start : Wiz’s record $32 Billion acquisition by Google pushes the dollar value to a record, but you may have also missed there were 11 VC-backed $1B+ exits already in 2025, worth $54.5 Cloud has just gotten going.”

He had the idea that the Cloud, not called the Cloud back then, would enable two entities to see the same transaction from their perspective. If we go back to 2006, BILL was a cloud-based company. At the time, there were dozens of cloud-based companies. acquisition. The thing with a moat is that it takes time.

Billion PostgreSQL Battle for AI Agent Supremacy Brief Overview : Two data giants are making strategic moves to dominate the AI agent infrastructure market through major PostgreSQL acquisitions. This acquisition builds on previous AI investments, including the 2023 purchase of Neeva, a generative AI search startup. Databricks: The $1.25

So public Cloud and SaaS stocks continue to be under a lot of pressure, with many Cloud leaders trading for half of what they were trading at just a few months ago. Of combining two slower-growing SaaS / Cloud companies into one that is growing at an OK rate. Potential key: – 28% EBITDA. jasonlk) April 11, 2022.

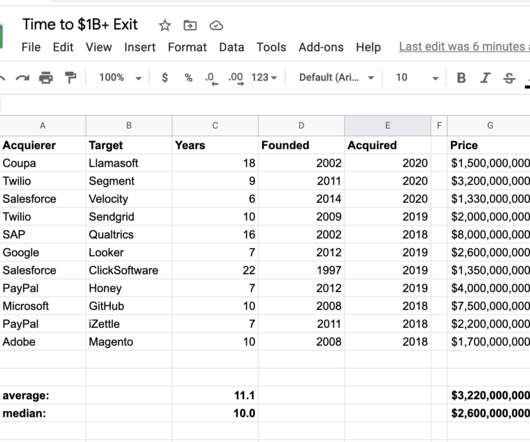

The other day Coupa did its first $1B+ acquisition, of 18+ year old Llamsoft. There should be a lot more billion+ acquisitions in Cloud and SaaS, if only because there are more decacorns to buy them. There are 100s of SaaS and Cloud unicorns today and dozens of IPOs. Adobe and Shopify are now worth $100B+.

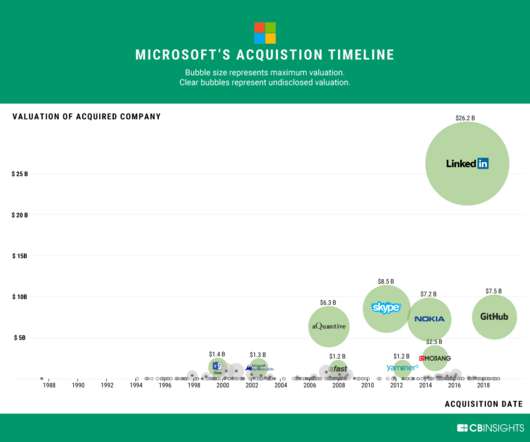

Yesterday, both Google and Microsoft announced their earnings for their cloud businesses. At the time of acquisition, Github had about 25m users & projected to reach 100m in 2025. “All of the number of developers using GitHub has increased 4x since our acquisition 5 years ago.”

Recently Bessemer Venture Partners did another great deep give on Cloud metrics at the Cloud 100. They’ll update their classic “State of the Cloud” on Sep 27-29 at SaaStr Annual 2021 in the SF Bay Area so come join us there for the latest! But only the best SaaS and Cloud get these multiples.

Q: When should a CEO walk away from an acquisition? I’ve walked from acquisitions where I, to be honest, did want the money but still walked. You have (at least) 4 constituencies in an acquisition: You and your co-founders. We all get too emotional and clouded. I’ve thought about this a lot. Your employees.

have done $1B+ acquisitions before their IPO. Get bought for stock early by Coinbase or Snowflake, sometimes the value can grow dramatically after the acquisition. Not just with the big public Cloud companies. And start-ups have gotten bigger. So they can pay more. Stripe, Databricks, etc.

Discover Bessemer Venture Partners’s annual State of the Cloud report, going through trends, benchmarks, and metrics that underpin the Cloud economy. The past twelve months have been relatively turbulent for Cloud founders. What does this mean for Cloud companies? What does this mean for Cloud companies?

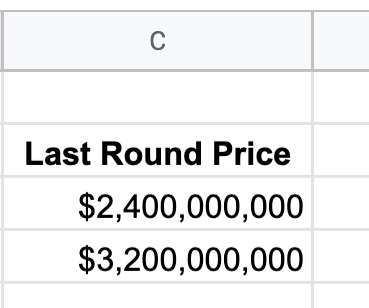

First IPO in 1999 First acquisition for $5.3 private equity buyout (Permira + CPPIB) Company needed to transform for the cloud era Classic “take private to modernize” playbook 2021: Second IPO on NYSE at $27.55/share IPO private IPO acquisition is becoming a common path. Informatica acquired for $8 Billion!

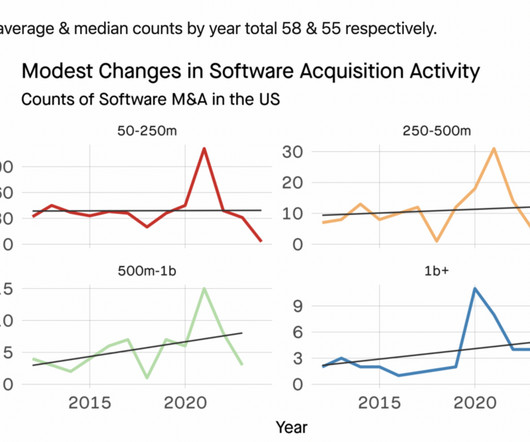

This time, on Mergers & Acquisitions. My biggest take-away: there are barely more than 50 acquisitions of $50,000,000 or more, at least disclosed one, in software of U.S.-based After all, there are so many more SaaS and Cloud leaders worth $1B+ that there wer a decade ago. based startups each year. By dollars, yes.

Q: What was the biggest acquisition failure or missed opportunity by a company? Still, my partial list in Cloud/SaaS: Google letting Microsoft buy / outbid for Github for $7.5b. Still, Service Cloud is huge so in the end, Salesforce built an epic business here in the enterprise segment. Priorities change when CEOs change.

It’s a massive acquisition at a massive price relative to other software acquisitions. The Skype acquisition was also about identity, consumer identity. This acquisition capstones the commitment. Box-out Amazon and Google in the Cloud Wars. “Every” business is moving to the cloud.

Similar questions have surrounded Microsoft’s acquisition of Blizzard; The US Department of Justice seeks to unwind the Google/DoubleClick merger ; British regulatory bodies forced Facebook to reverse its Giphy acquisition. Tricky questions also cloud recruitment conversations : who is hiring the new employee?

Nvidia, Google Cloud, Azure, etc. The Big Acquisitions Are Doing Well. 1% Dilution Many faster growing public SaaS and Cloud companies aim for 2% a year dilution or less from employee grants, down from the 10%+ common at start-ups. But how about 2026+? We’ll see. Salesforce Growth: FY26 $40.9B (guidance) FY25 $37.9B

An acquisition can make or break your startup. Take IBM’s recent purchase of RedHat to accelerate hybrid cloud adoption, or Salesforce’s acquisition of Mulesoft to coordinate, unlock, and integrate customer data better than any competitor. Good acquisitions aren’t easy to pull off. I could go on.

Q1 earnings season for cloud businesses is now behind us. These charts clearly show the ZIRP pull forward, the ensuing cloud cost optimizations, and then the recovery. GCP data is a bit more noisy as they don’t disclose GCP itself, but rather Google Cloud which includes GSuite.

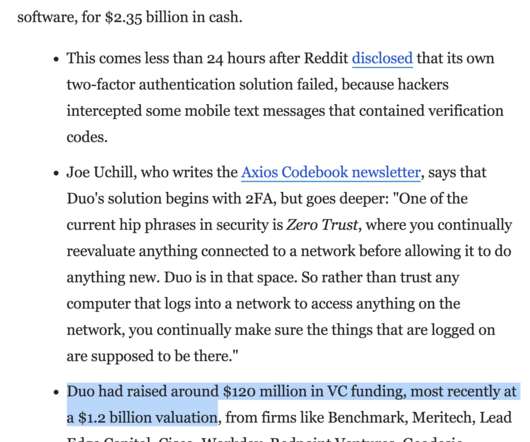

Billion acquisition of HashiCorp. About Dave McJannet: Dave McJannet is the CEO of HashiCorp, and led the company from early-stage to its successful IPO and $6B+ acquisition yb IBM. The last IPO of the 2020-2021 era was HashiCorp in December 2021. And it’s one of the first to be acquired! IBM just closed on its $6.4

Post-acquisition life is a whole new world for a founder. For me, seeing the EchoSign brand retired in favor of Adobe Document Cloud was painful. Post-acquisition, your financial upside is usually capped, although sometimes the post-acquisition financial incentives can still be substantial. Its different.

Data Cloud has been Salesforce’s fastest-growing product ever and will be their “fastest multi-billion dollar product ever,” indicating the market understands this data-first approach to AI implementation. This suggests a mistake in not integrating acquisitions more aggressively from the beginning.

The Week in Cloud: A look at the stories in Cloud, SaaS, and business software that we found particularly useful and interesting. Number 2 is still awfully big in the largest market in all of Cloud: [link]. A huge donation, driven by the Cloud: [link]. A huge donation, driven by the Cloud: [link].

They’re at almost $500m in ARR, with 1,850 customers, now growing a modest but steady 19% and they have gotten pretty efficient, like most other public SaaS and Cloud leaders. But new products from acquisition have fueled the overall customer count growth to 1,858. #2. But if you’re in the space, it’s a big player.

A strategic acquisition like Llamasoft is worth 15x. And as we’ll see below, those prices might actually be pretty high, because acquisitions often come at a premium. If you can grow faster, it’s more worth it than ever in SaaS and Cloud. The “growth premium” in SaaS has never been higher. And the weak?

Unparalleled Networking Opportunities SaaStr Annual brings together thousands of SaaS, Cloud and AI executives, founders, VCs, and industry leaders under one roof across our 40+ acre campus, May 13-15 in SF Bay! VIP Networking app for B2B founders and execs attending (no service providers, sorry!) And the VCs that want to fund them!

Every week I’ll provide updates on the latest trends in cloud software companies. Acquisitions don’t happen over night. If you need a champion to close a customer / sale, you need a SUPER champion to get an acquisition done. Subscribe now Share Clouded Judgement Leave a comment Follow along to stay up to date!

jasonlk joins @Jason to talk: 2020's cloud software boom How @zoom_us & @ericsyuan conquered competitors The public CEO acquisition mindset. : [link] : [link] pic.twitter.com/JT7MPreIpT. The Godfather of SaaS is BACK on today's Rising Stars of SaaS! — This Week in Startups (@TWiStartups) December 2, 2020.

Let’s take a look at 3 B2B acquisitions from a few years back as an example. Let’s first start with the $35m acquisition of TokBox after 11 years and the $220m acquisition of SpringCM after 13 years. talking about “tuck-in” acquisitions that can attach to existing revenue streams.

.” Cross-selling generates $5M+ in new monthly revenue – Rippling’s cross-sell motion alone drives over $5 million in net new ARR each month before counting any new customer acquisitions. The company now has three distinct “clouds”: HR Cloud : Traditional HR and payroll functions.

Salesforce grew Mulesoft, ExactTarget, and so far, Slack and all grew well after their acquisitions. In fact, Salesfeorce’s mutiple Clouds today are really built on top of its biggest acqusitions. ZoomInfo , one of SaaS’s great recent IPOs, is really an acquisition story. The “ZoomInfo” product was an acquisition.

So as you’ve seen, acquisitions have picked up in SaaS. So many acquisitions, so many IPOs, so many public and private valuations of great SaaS companies are actually at / worth less than 10x ARR. Yes, if the acquisition is strategic, multiples are at all-time highs. Yes, these are the Best of Times in Cloud.

Every week I’ll provide updates on the latest trends in cloud software companies. To fund significant customer acquisition costs to capture market share. The first assumption is that at the end of the rapid customer acquisition spend you will end up as the monopoly or duopoly leader (with, importantly, pricing power).

We’re approaching the age of 1,000+ Unicorns and despite a global pandemic, this remains The Best of TImes in Cloud and startups in general. The two latest $1b+ acquisitions weren’t quite as glamorous as they seem: Uber acquires Postmates for $2.6b. Or almost a billion+ acquisition. Amazon acquires Zoox for $1b.

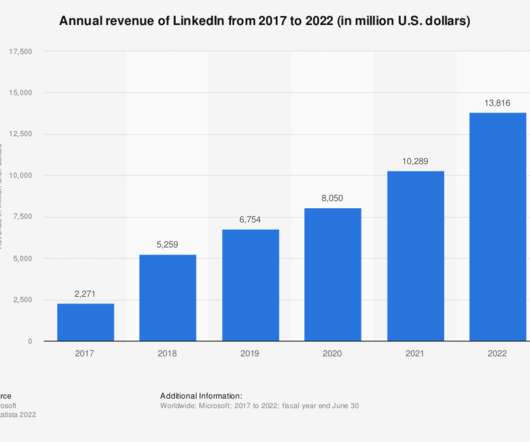

Because SaaS and Cloud are. Revenue tripled since Microsoft acquisition in 2016. After a slow patch after the acquisition, LinkedIn hit its new stride and tripled from $3B to $10B ARR from ’16 to ’21. #3. Cloud is an awesome force. #4. B2B market is on fire. Growth is accelerating — dramatically.

For a Really Big Tech Company, any acquisition of less than about $1b is somewhere between an experiment and a bet. In 2015, Microsoft wanted to help accelerate its SaaS / Cloud strategy and made a bunch of bets. took off, and Microsoft’s Cloud strategy became clear … a new task manager wasn’t important enough.

Perhaps the #1 reason though is that acquisitions are … weird and unpredictable. It’s just, once you see how it really gets done, you see a few non-obvious things: For every acquisition, there are 10 others just as good they could have done. There are 500+ Cloud and SaaS unicorns today. What do I mean?

And as much, it’s really a bellwether of SaaS and Cloud. Things are on fire in SaaS and Cloud. The Sales Cloud remains highly mature, only growing 11%. Service Cloud has passed Sales Cloud in revenue, and Platform is the biggest percent of revenue. SaaS and Cloud have flattened. Not anymore.

For most software companies, COGs encompasses cloud hosting costs and some fraction of customer success and professional services salaries. For startups, there tend to be two significant drivers of gross margin: cloud computing costs and professional services. Assume the company grows 5% per month. The company burns $1.9M

We organize all of the trending information in your field so you don't have to. Join 80,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content