This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

When SaaStr Fund made the first investment in RevenueCat back in 2018, nobody could have predicted that this “simple API for managing in-app subscriptions” would become the infrastructure powering 33% of all mobile subscription apps and reach a $500M valuation in 2025. ” required weeks of developer time to answer.

The Numbers Tell the Story: Monday.com Q1 2025 : 30% growth, $282M revenue Asana 2024 : Single-digit growth, struggling with churn Mostly Same Product Category, Mostly Different Customers Both companies build “work management” software. The “productivity software” that seemed essential in 2021 is now getting cut.

revenue multiple proves strong B2B companies with real growth (and it’s strong) can still command premium exits. The deal shows acquirers are hungry for revenue acceleration—Xero expects to more than double group revenue by 2028 with this acquisition. discount from its 2021 peak valuation of $4B. exit represents a 37.5%

For seven years, growth was painfully slow: 2016-2021 : Minimal revenue, limited funding first years 2022 : $1M ARR (after 6 years!) Usage-Based Pricing for AI Subscription models work for traditional software, but AI-powered platforms often create variable value. 2023 : $2.4M ARR Despite raising significant funding ($97.4M

In 2023, companies are looking to improve their revenue and drive sustainable growth by scaling their subscription offerings, to increase the rate of growth and resilience by moving from one-time sales to recurringrevenue. GARTNER is a registered trademark and service mark of Gartner, Inc. All rights reserved.

Every IPO other than Sailpoint is trading up, and we’ve got a jolt of momentum here for the first time since … well … 2021. Navan represents something different: a mainstream B2B software company with enterprise clients and subscriptionrevenue models that institutional investors understand. But we may have our first. .

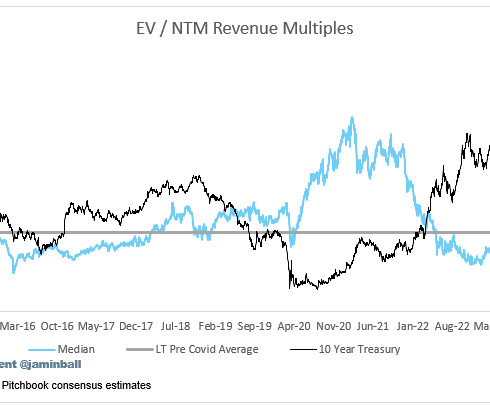

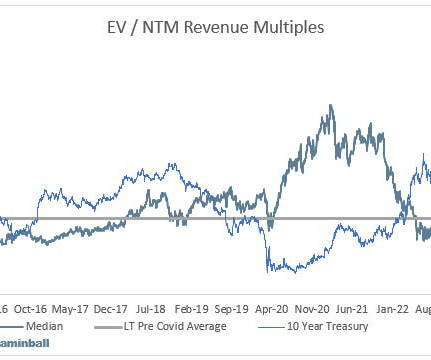

As a result, software vendors often see an uptick in revenue and bookings during these periods. We all know 2020 and 2021 was the year of excessive software buying fueled by ZIRP. Revenue multiples are a shorthand valuation framework. This concept is nothing new and has been going on for a while. Top 5 Median: 17.3x

Instead of prioritizing new business acquisition, CLG turns existing customers into a primary source of revenue. CLG-driven companies achieve exponential revenue growth through retaining existing customers and expanding their accounts—and this is only possible with a stellar customer experience at the core. And it’s not just you.

The State of GTM Jobs: Customer Success At the crossroads of retention and revenue, Customer Success (CS) is a cornerstone for sustainable growth and is growing in both scope and importance. The primary ways to achieve this are by monetizing the post-sales motion or more closely aligning it with revenue. Chasing down invoices?…

Billion in 2015 Second IPO in 2021, $10 Billion market cap Salesforce acquires them in 2025 for $8 Billion Man, it's a journey pic.twitter.com/Lmi9NPQbj6 — Jason SaaStr.Ai Key insight: Even profitable, growing companies with real revenue can see valuations decline in different market cycles. But founded … in 1993!

Subscribe now Shades of 2021 in Venture Markets Private markets are really starting to heat up, and I’m starting to see shades of 2021. ” I heard that a lot in 2021, and unfortunately not many call options hit… It’s hard to invest at 100x ARR and exit at 10x and make a return VCs aim for.

So many startups these days are claiming they have “ARR” from revenue that … doesn’t recur. Doesn’t ARR stand for Annual RecurringRevenue? ARR now really means revenue with 100%+ Net Revenue Retention. 50% revenue from software (recurring), 50% from payments (not-recurring).

Revenue grew nicely at first from $1m to $3.5m — Jon Ma (@jonbma) March 27, 2021. Customer count growing 33%, revenue growing 65% — the “Golden Ratio” for future growth. UiPath grew from 6,009 customers last year to 7,968 at January 2021, or 33% growth. Fast, but revenue grew much faster (65%).

The majority of its revenue is now from Bitcoin transactions, not “traditional” payments and software. Square is still a high-margin software company at its core with a large but low-margin payments business on top. Going global is tougher in payments and fintech. So is Square a SaaS company? It’s core.

Answering the most common and most pressing questions about MRR to guide your 2021 planning. Monthly recurringrevenue is one of the least exciting topics to take on in 2020. MRR stands for Monthly recurringrevenue. It measures the total repeatable revenue your company generates each month. What is MRR?

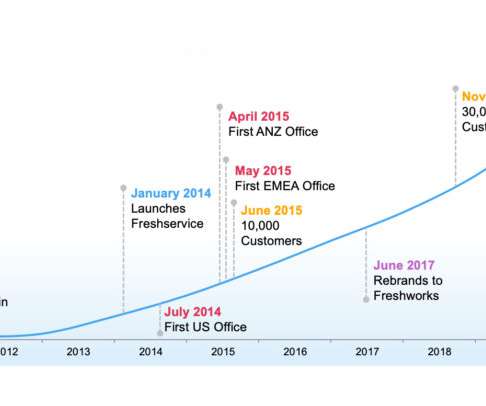

49% revenue growth from 20% customer growth. From 10,000 customers in 2015 to 50,000 in 2021. Freshworks quintupled its customer base from 2015 to 2021. 62% of revenue from annual subscriptions. A reminder that, like Zoom , you don’t have to force annual subscriptions. NRR of 118%.

Was it misunderstanding bookings vs. ARR vs. GAAP revenue, was that the issue? With early revenue, you start thinking about churn and scalability of every aspect of the business, including product, infrastructure, customer support, sales and marketing. Mistake #1: Bookings are not revenue. They didn’t make any sense.

— Jason BeKind Lemkin (@jasonlk) April 16, 2021. Over $500,000 revenue per employee. Monetizing ecommerce via subscriptions, but not payment processing. But in contrast to Wix and Shopify, it doesn’t keep much of the revenue from merchant services itself. 70% annual, 30% monthly subscriptions.

We recently announced a new partnership and integration with Invoiced. The integration was created by the Invoiced team because they wanted to find a way to integrate their billing data with ChartMogul. What is Invoiced? At the same time, the product also allows them to provide a modern payment experience to their customers.

In 2021+, Yes. SaaStr 555: Secrets to Building a High-Performing Revenue Marketing Engine with Demandbase VP of Marketing Tracy Kraft. Unlocking Growth in the Internet Economy: a Perspective from Stripe Head of Invoicing, Suzanne Xie. A 4 Point Test To Know If You Are Ready to Hire BigCo Folks. When to Go Multi-Product in SaaS.

Only 20% of Revenue from “SaaS”, 80% From Transactions and Float (Fintech) Bill started off 100% SaaS, and slowly and deliberately added payments. Fast forward to today, and only 20% of its revenue is from software subscriptions. But a reminder how software + payments can really work well, when it works. #3.

So it’s been a long IPO drought since HashiCorp was the last IPO of the Boom Times in December 2021. But now a second SaaS security leader has filed to IPO, Rubrik. But they are ar $780,000,000+ in ARR, with an 86 NPS and strong revenue growth at 29% overall and 49% in subscriptions (yes, it’s confusing).

Blackline is one of the leaders in accounting software and invoicing-to-cash. Blackline had consistent growth of 20%+ in 2020, 2021, and 2022. 5% Customer Growth + 106% NRR = 11% Revenue Growth Super helpful when the math ties here ? #7. But when they needed that founder DNA, Therese came back last year. As CEO again.

Meanwhile, a 2021 McKinsey study revealed that over two-thirds of B2B buyers prefer remote or digital self-serve channels over a traditional in-person sale. For example: Are you making your quoting and invoicing experience as efficient and flexible as possible? The post SaaS: Is B2B Revenue Better than B2C?

Those of us who’ve been around a while think of New Relic as a freemium and almost SMB tool, but today 77% of their revenue comes from accounts greater than $100k. New Relic’s net negative churn / net dollar retention has dropped to 98% in the last quarter, despite a record 77% of revenue being from the enterprise.

Zoom came out of 2020-2021 with SMBs no longer growing, but a huge boost in the enterprise. Payments still materially accelerating overall growth to 16%, and predicting revenue growth from payments and merchant solutions to more than double that of subscriptions and SaaS. More on that here.

— Ari Levy (@levynews) September 22, 2021. While its software has decent margins of 66%, software is only 10% of Toast’s total GAAP revenue. It loses money on the hardware (gross margin negative) and the payments solutions have barely a 20%+ margin and constitute the vast majority of revenue today.

Still growing, but 30%+ more slowly that before : “Workday has lowered its subscriptionrevenue estimates by up to $85m for fiscal 2021 in response to the COVID-19 crisis.” “ Sales in fiscal 2021 will be about $20 billion , down from an earlier projection of as much as $21.1

Only annual contracts, and plenty of professional services (25% of revenue). 99% of its customers are on annual contracts, and 25% of its revenue is from professional services. 25% of revenue from services may sound high, but it’s a fairly standard ratio in true enterprise software. About $250,000 revenue per employee.

Reason 1: To Introduce You to Digital Invoicing and Interactive Quotes, Our Latest Products. Earlier this year, we released Digital Invoicing , a new, easy way to create and send invoices directly from FastSpring — no PDFs or back and forth emails required. Reason 3: To Highlight Our SaaS and Subscription Business.

The business exploded during lockdown when in-person tours were more difficult, growing 100% YoY from 2020 to 2021, and the business continues to grow today. Its market cap is $945m, but that’s including $450m in cash, so the net enterprise value is closer to $500m, or a bit less than 4x revenues.

But we went on to host 5 incredible digital events that reached 100,000+ … and we’ll be back IRL in 2021. What’s a typical price increase I can expect when renewing my SaaS subscriptions? Even If It Isn’t Revenue.” More on that soon! Additional Health & Safety Rules for 2020 SaaStr Annual.

From just 8% growth in ’18 to ’19 — hyper-mature — to a stunning 59% growth rate after Covid and to almost 100% year-over-year growth at the end of 2021. Its Top 10 Customers have historically paid about 20% of its total revenue, so its whales matter, paying ~$2m a year on average each.

They’re only growing revenue 7-8%, but they are relatively efficient, with 13% adjusted EBIDTA margins. Growth Slowed from 22% in 2021 to 8% Today. Transaction Revenue Has Slowed, But Subscriptions Are Up. Today, the self-service legal services giant is worth an impressive $3.4 5 Interesting Learnings: #1.

. “The Things Nobody Tells You About An $8B Acquisition with Ryan Smith from Qualtrics” #8. “The Current State of SaaS Companies, Subscriptions, and Retention in 2021 with ProfitWell” #9. “A Step by Step Guide to Revenue Growth with Mark Roberge, Harvard Business School” #10.

If you’re looking to grow your small business in 2021 and beyond, you need to organize every aspect of your company. Here’s how to stay organized in 2021 and beyond. Keep Track of Your Small Business’s Invoices and Payments. Every small business needs to manage payments, invoicing, and billing.

This reached a fever pitch in 2021 when every incrementally better company was funded with large rounds of capital. Revenue multiples are a shorthand valuation framework. Multiples shown below are calculated by taking the Enterprise Value (market cap + debt - cash) / NTM revenue. Overall Stats: Overall Median: 5.3x

But with so many payment processing tools on the market, which one should you choose? Here's a list of six payment processing platforms for 2021. Baremetrics provides you with valuable insights that power your business, such as retention rate , recurringrevenue , churn rate, and other metrics. Table of Contents.

ProfitWell is a cloud-based app that generates real-time financial and subscription metrics for data-driven SaaS enterprises. The recurringrevenue growth platform provides users with valuable insights into subscription funnels and one-click analytics for Stripe. But ProfitWell does not benefit all SaaS companies.

When FastSpring’s Chief Product Officer Kurt Smith worked with growth-stage to Fortune 100 companies at Accel-KKR, he consistently saw pricing as one of the most essential growth levers they employed to meet their next revenue goal. And Kurt believes that iterative pricing can be a highly effective strategy during volatile markets.

Revenue forecasting software is used to create predictions of sales. 1 Why Use Revenue Forecasting Software? Why Use Revenue Forecasting Software? Revenue forecasting software allows companies to forecast revenue and efficiently allocate resources in a way that optimizes growth and cash flow. Table of Contents.

They offer some of the best-known subscription boxes around, reflecting an increasingly popular (and potentially lucrative) business model. Why Should You Launch a Subscription Box? According to MarketsandMarkets , the subscription and recurring billing market will grow to around $7.8 Recurring Business Revenue.

If we rewind the clock back a few years and look at the year end top 10 for 2020, 2021, 2022 and now 2023, there are 4 companies that find themselves on every year end list: Snowflake, Cloudflare, Datadog, and Zscaler. and 99.2%, respectively) And below you can see who ended up in the top 10 at the end of 2022 and 2021.

These are tougher times for almost everyone than the Go Go Days of 2021. Billion, Growing 17% Overall with SubscriptionRevenue Growing 22%. So we wanted to do a little weekly look at who in SaaS and Cloud is doing well. Budgets are being scrutinized, and even the best are growing more slowly in many cases. Workday at $6.8

We organize all of the trending information in your field so you don't have to. Join 80,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content