This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Dear SaaStr: Which SaaS Products Offer ONLY Annual Pricing? Many of the companies Ive invested in only offer annual pricing. And here, forcing annual pricing just creates gates to getting paid. Smartsheet for example standardized on annual pricing plus a free trial. Freemium doesnt work well here.

Dear SaaStr: Why Do Angels Invest Even if Most Of Them Fail? True angels invest so early, maybe only 2 out of 50 make any real money. If it’s just 1 Big Winner out of 50 angel investments, to even just double your money, that winner has to do 100x. And is a 10x Return Even Enough? You’re right, 10x isn’t enough.

One of the hottest topics in AI for B2B is around outcome-based pricing. Simply that outcome based pricing may be exciting to VCs who think it unlocks more TAM and budget, and it may seem exciting to founders and execs who think it will help them grow deal size. What I do know is a pricing model is not a product. What do I mean?

It’s now falling to 150 because 81% percent of the dollars invested in venture capital at the height of the boom came from non-traditional venture capital firms which are all very likely to leave investing. You get a base number of minutes for a particular price. US venture funding went from 8 to 300 over 15 years.

It will show you how to select the right solution and what investments are required for success. We hope this guide will transform how you build value for your products with embedded analytics.

Most Smaller VC Funds ($100m or smaller fund) would like to own 10% or more after a Seed or Pre-Seed Investment , but typically model around 7% average ownership. If it’s not a core investment, VC funds may be more flexible. But these exceptions to ownership targets make these investments non-core.

Traditional VCs usually reserve another 1x-2x of their first check for later investments. If the synergies are real, they’ll happen irrespective of some token investment. An investment won’t create a partnership. An investment may anoint one vendor in the space as the preferred vendor over competitors. Be realistic.

Several macro factors are converging to create this perfect storm: Enterprise Budget Scrutiny : CFOs are demanding higher ROI thresholds for software investments. The low-hanging fruit of digital transformation has been picked, and companies are being more selective about additional software investments. Slower New Customer Growth.

Financial Services: Mortgage & Loan Processing Help users explore mortgage options by collecting key inputs like purchase price, credit score, down payment, and property location, then presenting tailored loan choices with current rates. Pay only for what you use with transparent pass-through pricing for 3rd party integrations.

Pricing Model Evolution : HubSpot’s multi-tiered pricing approachfrom free tools to enterprise solutionscreates natural upgrade paths as companies grow, maximizing lifetime value while maintaining strong operating margins (14% non-GAAP operating margin in Q1 2025). Their ecosystem extends their reach globally.

So everyone is now paying the price for lowering the bar in the Boom Times of mid ‘20 to early ‘22. And now we’re paying the price. The same things happened in VC and investing. I did some of this myself, both on people and investments. Better to do with fewer people, fewer investments, fewer initiatives.

Dear SaaStr: Should I Buy a Great “ com” At a Crazy Price or Just Stick What the “ ai” We Already Have? One of the top SaaStr Fund investments is Owner, growing incredibly quickly. domain is confusing customers or holding back your brand, it might be worth the investment. But if youre finding that the.ai

But it’s clear that it’s still in the investing phase, and increasing spend in sales & marketing. But SMBs in the middle have become more cost and price-sensitive. #10. Outside of a pre-IPO phase, Klaviyo has been cash-flow positive or close for most of its history. Just not as quickly as overall revenue growth. #4.

When SaaStr Fund made the first investment in RevenueCat back in 2018, nobody could have predicted that this “simple API for managing in-app subscriptions” would become the infrastructure powering 33% of all mobile subscription apps and reach a $500M valuation in 2025. The SaaStr Fund Thesis: Mobile Subscriptions Will Explode.

This isn’t just about productivity — it’s about economic disruption : The Agent Economics: Traditional SaaS: $3,500 per employee annually across organizations AI Agents: Can replace entire job functions for <$100/month The math may be devastating for high priced seat-based pricing models 3. Palantir was ready.

We’re obviously written up a lot about Fundraising and Investing here on SaaStr.com, but time and time again, SaaStr CEO and Founder Jason Lemkin has seen so many Founders sign a bad term sheet based on gut instinct, VC celebrity or vibes, and while that may be fine, it’s not enough.

Having been through 4 acquisitions in different forms (founder, exec, etc), it’s a lot like a venture capital investment. A ton of time is invested negotiating price, and then way, way too much time on inconsequential legal terms, and then … it closes. Not really.

This extreme revenue concentration shows Figma’s ability to create significant value for mid-market and enterprise customers—a small number of deeply engaged accounts drive the majority of revenue, indicating strong product-market fit at scale and pricing power within larger organizations.

3 Came from the Investment Bank They Hired. In my experience, hiring an investment bank to help you in any acquisition > $100m or so is critical. But Andy got 3 other firm offers through the bank he hired — along with a price more than $10m higher. They Ran a Crisp, Tight Process And Got 4 Offers to Buy Them.

SaaS pricing isn’t static – it’s a living strategy that grows with your company. In this article we dive into a playbook for pricing across different stages of company growth, inspired by Geoffrey Moore’s Crossing the Chasm. Tiered pricing models emerge to address these differences.

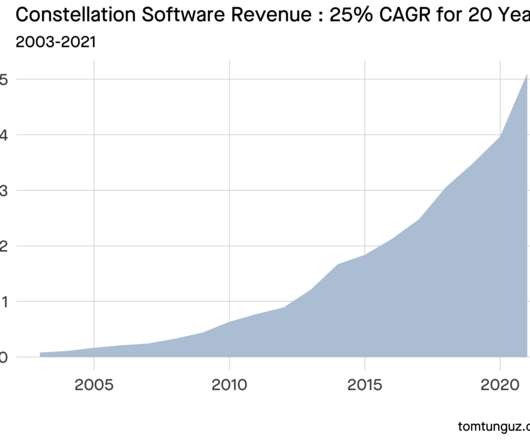

A former venture capitalist, Mark Leonard started Constellation in 1995 with $15m of outside investment & a goal of buying vertical software companies with a moat & good unit economics. Price Increases. New bookings added 10% ; price increases 5%. Growth Source. Acquisition. New Bookings. Contraction. -3%. Net Growth.

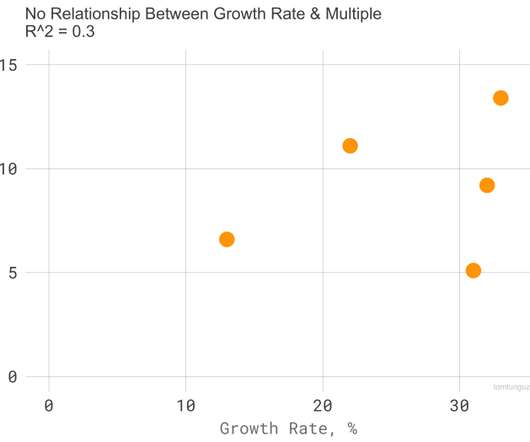

But no relationship exists between the Nasdaq’s price level & multiples. The data suggests the market has attained a pricing floor. I can’t ascertain how record fundraising inflows into private equity funds might bolster these prices, but the billions burning holes in PE wallets must impel some activity.

I get to set the price of the apples because they’re my apples. Price Determines Product Quality (Self-Fulfilling Prophecy) “When you’re making a product, the price you set will determine how good your product is. net income, 111.5% revenue growth year-over-year 2013 IPO : $129.5M net income, 111.5%

This matters a lot more when stock prices are going down, and management teams often grant additional shares to make employees whole (thus increasing dilution even more) Net Revenue Retention High net revenue retention is the fourth aspect of a successful quarter, and one of my favorite metrics to evaluate in private SaaS companies.

And as stock prices rip higher, growth VC floods back in. But overall, the growth investments weren’t big wins. 2021 prices were certainly inflated in many cases from valuations today. So SaaS is back. Top SaaS stocks are on fire the past few months, and the SaaS downturn in B2B2B appears to be behind us. At least at IPO.

The B2B / SaaS Parallel : Many SaaS companies build their entire business on one pricing model, one customer segment, or one distribution channel. This early investment in regulatory compliance has become their key differentiator against Tether and newer entrants. Circle trading at $85 up from $31 IPO price.

I try to look at two things in Vertical SaaS startups, at least when investing : Will everyone in the vertical / industry use it? The good news is, you can support these price points effectively with a very efficient inbound sales team, and/or a mix of self-serve and sales-led. At two different price points. That’s the question.

GTMfund’s 3 Areas of Focus for Investing Thanksgiving weekend is always a period of reflection and gratitude. Reflection across go-to-market trends, but also on the investment front (not to mention community !). A common misconception is that the name is representative of the type of software we invest in.

I havent done that, but Ive done handshake deals in one day in maybe 50% of my investments (i.e, Not literally months to do the homework that doesnt take long but sometimes months to see enough progress for the investment to make sense to me, to connect enough dots. Yes, term sheets get done in one day.

Dear SaaStr: How Can I Convince My Investor We’ll Double Their Investment By The Next Round? If you are a VC / private investor, there’s a key meta question: why invest now ? Because, at the same price … later is always better. This is really the reason most very early-stage investments get done.

The shift from “innovation budget” to “operational budget” means AI tools must compete directly with established software investments—and many aren’t winning those comparisons yet. The Hidden Enterprise Pipeline Card spend data, while valuable, captures only a portion of enterprise AI investment.

It’s the emergence of a new category that’s attracting billions in investment and fundamentally disrupting the $500B+ software development market. If model providers change pricing or restrict access, margins could compress quickly. Usage-based pricing aligns costs with value creation and enables explosive growth.

And while the Wiz deal hasn’t closed yet, seeing a record M&A deal price fuels more VC investment. I asked founder Ryan Smith at SaaStr Annual what he thought of that record price? In part, because they see the absolute potential exit sizes just going up and up. “The next one will be even higher.

👑 Larry’s Long-Term Vision : CEO Larry Ellison’s early AI investments and partnerships (particularly around autonomous database technology) positioned Oracle perfectly for the AI infrastructure boom. 💾 Data as the Moat : While others chased AI features, Oracle doubled down on what it does best—managing enterprise data at scale.

It’s about fundamental organizational redesign —from pricing models (hybrid consumption/subscription) to team structures (forward-deployed engineers vs traditional CSMs) to investment priorities (94% AI spend increases among high-growth companies). This isn’t about sprinkling ChatGPT into your sales process.

Models built by OpenAI, Google, and Anthropic have billions of dollars to invest in training these models, so you have more powerful engines under the hood at no cost to you. The price for inference has massively plummeted this year, so you have more powerful models to build into your application, and they cost less every time you use them.

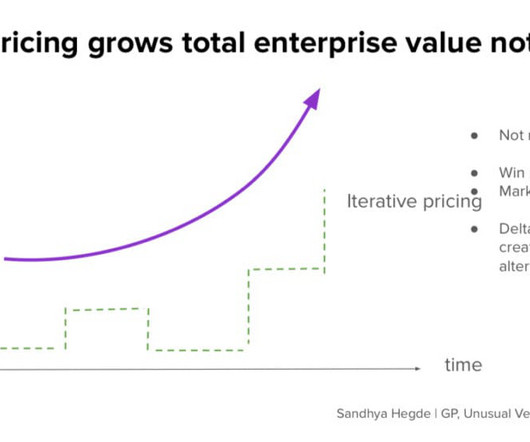

With everything in AI moving so rapidly, what’s the best way to price Artificial Intelligence products or SaaS tools with custom AI features and integrations? So we asked the expert, Sandhya Hegde, General Partner at Unusual Ventures to share her best practices and trends for pricing and packaging AI products. Why is pricing so tricky?

G2 had us back for another great deep dive on just where SaaS investing is there days, and it was a great panel: Accel Partner Arun Mathew Inspired Capital Founder & Managing Partner Alexa von Tobel Salesforce Ventures Managing Partner Paul Drews and Jason Lemkin! Low investment multiples pose a key challenge.

The purpose of the detailed information is to help investors (both institutional and retail) make informed investment decisions. As far as an expected timeline - typically companies launch their roadshow ~2-3 weeks after filing their initial S-1 (the roadshow launches with an updated S-1 that contains a price range).

Founded 2008 * Raises ~$53m in VC * Sells 17 years later for $53m * Only $20m of that cash * 2x ARR price * 1x What Raised Just plain tough. Thats just how investing work. I used to sort of think that way. But the reality is, VCs only make real money if founders make a ton of money. The stakes go way up. So who makes what here?

Competition and Differentiation: Founders worry about competitors copying their product or undercutting them on price. Investing in customer success early can make a huge difference here. But not most of us. It’s often the only way to scale meaningfully in SaaS. And you should. The pace here has accelerated even more with AI.

Engineering resources: With thousands of engineers, companies like HubSpot can make substantial AI investments when they choose to 3. The Future of AI in Customer Support While many vendors are achieving similar baseline results with AI customer support, Brian believes we’re still early in unlocking its full potential.

The key is concentrated investment in differentiation, not diversification. Adobe deal (2022): $20B fixed price IPO potential (2025): $18-27B range + $1B breakup fee received Net outcome: +$4-8B value creation vs. ” Companies achieving 60%+ Rule of 40 scores trade at 2-3x premium multiples.

Walker Research found in 2024 that the customer experience is now equal to price and product regarding key brand differentiators. Organizations that invest heavily in customer success earlier see much higher customer retention and loyalty than the competition. For example, say your company is going upmarket to Enterprise.

We organize all of the trending information in your field so you don't have to. Join 80,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content