This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Today, we capture on average approximately 1% of our customers’ GTV as revenue from their subscription to and current usage of our products. ”” Benchmark Data The data shown below depicts how the ServiceTitan data compares to the operating metrics of current public SaaS businesses.

Given most software companies are not profitable, or not generating meaningful FCF, it’s the only metric to compare the entire industry against. I created this subset to show companies where FCF is a relevant valuation metric. Companies that do not disclose subscription rev have been left out of the analysis and are listed as NA.

As you all know, one of my favorite metrics to look at is net new ARR added in a quarter. For those who don’t, I will take quarterly subscription revenue x 4 as a proxy for ARR. Given most software companies are not profitable, or not generating meaningful FCF, it’s the only metric to compare the entire industry against.

Given most software companies are not profitable, or not generating meaningful FCF, it’s the only metric to compare the entire industry against. I created this subset to show companies where FCF is a relevant valuation metric. Companies that do not disclose subscription rev have been left out of the analysis and are listed as NA.

In this week’s Workshop Wednesday , Salesforce Ventures Investor, Jessica Bartos, shares the 5 metrics every SaaS company should care about in any market environment, especially the one we’re currently in. Growth Is Still Number One Growth is still the number one metric, but it’s not the only one. You do that by showing momentum.

Given most software companies are not profitable, or not generating meaningful FCF, it’s the only metric to compare the entire industry against. I created this subset to show companies where FCF is a relevant valuation metric. Companies that do not disclose subscription rev have been left out of the analysis and are listed as NA.

Given most software companies are not profitable, or not generating meaningful FCF, it’s the only metric to compare the entire industry against. I created this subset to show companies where FCF is a relevant valuation metric. Companies that do not disclose subscription rev have been left out of the analysis and are listed as NA.

Standout feature for creators: Creators can get access to a wide range of campaigns and sign up to be presented to join the platform’s database. The platform allows creators to connect with brands, access product discounts, and receive payments directly through Shopify, making it easier to monetize their influence.

By Inga Broerman How Industry Consolidation is Reshaping Subscription Billing The subscription economy is on a path of rapid growth and transformation, projected to reach a $3 trillion valuation in 2024. For smaller and mid-sized businesses, this consolidation presents both challenges and opportunities.

Given most software companies are not profitable, or not generating meaningful FCF, it’s the only metric to compare the entire industry against. I created this subset to show companies where FCF is a relevant valuation metric. Companies that do not disclose subscription rev have been left out of the analysis and are listed as NA.

Given most software companies are not profitable, or not generating meaningful FCF, it’s the only metric to compare the entire industry against. I created this subset to show companies where FCF is a relevant valuation metric. Companies that do not disclose subscription rev have been left out of the analysis and are listed as NA.

Upgrade your subscription to get access to the rest of this post and other paid-subscriber only content. Upgrade subscription The post Video of my SaaStr 2023 Presentation: The Strategic Use and Abuse of SaaS Metrics appeared first on Kellblog. You're currently a free subscriber.

Given most software companies are not profitable, or not generating meaningful FCF, it’s the only metric to compare the entire industry against. I created this subset to show companies where FCF is a relevant valuation metric. Companies that do not disclose subscription rev have been left out of the analysis and are listed as NA.

Through these interactions, I’ve built up mental benchmarks for metrics on which I place extra emphasis. My hope is that this analysis can provide startup entrepreneurs with a framework for how to manage their businesses around SaaS metrics (e.g., This metric is more self-explanatory, so I won’t go into detail.

Pendo for Startups” gives companies access to the product usage data that today’s investors consider alongside business metrics as they vet deals, as well as sentiment and guidance tools to improve product usage and adoption. Blissfully unveiled their SaaS Trends 2020 report, hitting on a few highlights in the virtual presentation.

Given most software companies are not profitable, or not generating meaningful FCF, it’s the only metric to compare the entire industry against. I created this subset to show companies where FCF is a relevant valuation metric. Companies that do not disclose subscription rev have been left out of the analysis and are listed as NA.

Given most software companies are not profitable, or not generating meaningful FCF, it’s the only metric to compare the entire industry against. I created this subset to show companies where FCF is a relevant valuation metric. Companies that do not disclose subscription rev have been left out of the analysis and are listed as NA.

And very well may lead to better “other” metrics like retention or churn. Given most software companies are not profitable, or not generating meaningful FCF, it’s the only metric to compare the entire industry against. I created this subset to show companies where FCF is a relevant valuation metric.

Update on Q4 Earnings One metric I love tracking in net new ARR added in a quarter. Given most software companies are not profitable, or not generating meaningful FCF, it’s the only metric to compare the entire industry against. I created this subset to show companies where FCF is a relevant valuation metric.

Chargebee is a robust subscription management platform. However, there are certain aspects of collecting recurringpayments that you would still be responsible for when using Chargebee, such as: Connecting to payment gateways manually. Zoho Subscriptions. Remitting taxes at the end of the year.

Given most software companies are not profitable, or not generating meaningful FCF, it’s the only metric to compare the entire industry against. I created this subset to show companies where FCF is a relevant valuation metric. Companies that do not disclose subscription rev have been left out of the analysis and are listed as NA.

Just a quick post to share my slides from today’s presentation at SaaS Metrics Palooza 2024 , entitled The Impact of AI on SaaS Metrics. In the future, we’re going to read invoices , instead. But for external reporting, the big six SaaS metrics all depend on ARR and going forward that won’t change.

Given most software companies are not profitable, or not generating meaningful FCF, it’s the only metric to compare the entire industry against. I created this subset to show companies where FCF is a relevant valuation metric. Companies that do not disclose subscription rev have been left out of the analysis and are listed as NA.

There’s a trend in pitch decks and startup pitches I’ve been watching - the commingling of metrics definitions, especially ARR. The valuation multiples on annual recurring revenue are the highest across startup categories. Then, consumer subscription businesses began pitching using ARR. Tom-ay-to / tom-ah-to.

One metric I like to examine is how much companies adjust their full-year guidance. Given most software companies are not profitable, or not generating meaningful FCF, it’s the only metric to compare the entire industry against. I created this subset to show companies where FCF is a relevant valuation metric.

Unlike Meritech Public Comps , where you can see metrics for the best [1], public SaaS companies, this private company data is somewhat harder to come by (the only other source that springs to mind is RevOps Squared ) and, for most of us, it provides much more realistic comparables than Meritech [2]. See slide 13 of this presentation. [3]

ChartMogul is an analytics platform to help you run your subscription business. You get a complete overview of your global subscriber base; MRR, ARPU, ASP, churn and LTV are presented in a beautiful and easy to use dashboard. Our clients love to use our solution. Every day, all day.

Provides end-to-end visibility of analytics and key metrics to all stakeholders, including executives, Finance professionals, line-of-business leaders and other business partners. You can some metrics below based on different share prices. Financial and Operational Reporting. This implies roughly a $4.2 - $4.8b market cap, and a ~7.5x

Given most software companies are not profitable, or not generating meaningful FCF, it’s the only metric to compare the entire industry against. I created this subset to show companies where FCF is a relevant valuation metric. Companies that do not disclose subscription rev have been left out of the analysis and are listed as NA.

About Our Presenters. Kurt is the head of product, payments, strategy, and corporate development at FastSpring, as well as the General Manager of Interactive Quotes (IQ). No matter what your business model, we meet you where you are. No matter what your business model, we meet you where you are. About FastSpring.

This might present a chance to complement product-led engagement with enterprise sales. Moving away from a subscription to a consumption-led model can bring several benefits to your business. Moving away from a subscription to a consumption-led model can bring several benefits to your business. Be clear on your new metrics.

Given most software companies are not profitable, or not generating meaningful FCF, it’s the only metric to compare the entire industry against. Most public companies don’t report net new ARR, so I’m taking an implied ARR metric (quarterly subscription revenue x 4).

Given most software companies are not profitable, or not generating meaningful FCF, it’s the only metric to compare the entire industry against. I created this subset to show companies where FCF is a relevant valuation metric. Companies that do not disclose subscription rev have been left out of the analysis and are listed as NA.

Did you know the subscription economy is touted to reach $1.5 As a business that provides software as a service, you will not only need to jump on this bandwagon, but more importantly, you will need the right set of subscription management tools to stay on it to keep reaping the profits of this booming industry. trillion by 2025 ?

Given most software companies are not profitable, or not generating meaningful FCF, it’s the only metric to compare the entire industry against. Most public companies don’t report net new ARR, so I’m taking an implied ARR metric (quarterly subscription revenue x 4).

.” How Klaviyo Makes Money Klaviyo has about 130k customers, with an ACV of ~$5k From the S-1: “We generate revenue through the sale of subscriptions to our customers for the use of our platform. We currently permit our customers to send unlimited push notifications, which are included as part of our email subscription plan.

Given most software companies are not profitable, or not generating meaningful FCF, it’s the only metric to compare the entire industry against. I created this subset to show companies where FCF is a relevant valuation metric. Companies that do not disclose subscription rev have been left out of the analysis and are listed as NA.

Here’s an interesting stat: 70% of businesses consider subscription and membership models indispensable for future commercial growth and expansion. They must engineer a well-rounded solution that makes handling subscriptions a breeze (and yes, it is as hard as it sounds). However, only 10% of them currently employ these models.

Step 2: Card recognition If there is a successful authentication, the checkout system will retrieve the customer’s stored card information and present the customer with a list of available card network options. The customer will then select their preferred means of payment. Your provider should help with this.

For businesses offering subscriptions, memberships, retainers, and other recurring services, recurring billing is a powerful solution to streamline processes and ultimately enhance revenue generation. Consider this: Consumers are already conditioned to the subscription model. Learn More What is Recurring Billing?

Given most software companies are not profitable, or not generating meaningful FCF, it’s the only metric to compare the entire industry against. Most public companies don’t report net new ARR, so I’m taking an implied ARR metric (quarterly subscription revenue x 4).

We expect these dynamics to persist in the near term, which is reflected in our revised FY '25 subscription revenue guidance. Quarterly Reports Summary Guidance for Snowflake and Workday are product rev and subscription rev, respectively. I created this subset to show companies where FCF is a relevant valuation metric.

Given most software companies are not profitable, or not generating meaningful FCF, it’s the only metric to compare the entire industry against. I created this subset to show companies where FCF is a relevant valuation metric. Companies that do not disclose subscription rev have been left out of the analysis and are listed as NA.

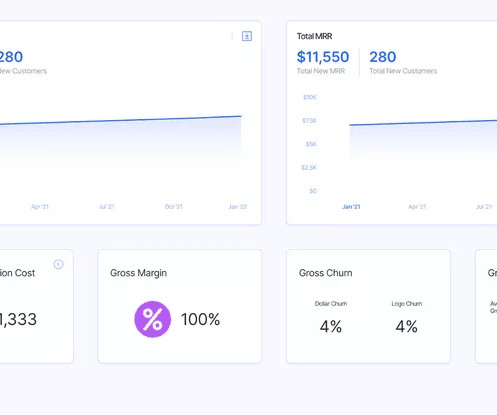

Would you like to learn how to design a SaaS metrics dashboard for your team without any coding? We also explain what metrics you may want to track and how to use the insights they offer. These dashboards are often customizable so they allow businesses to focus on specific metrics relevant to their goals. SaaS Metrics Dashboard.

We organize all of the trending information in your field so you don't have to. Join 80,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content