This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Subscribe now Azure Report - Cloud Infra Looks Good! For software, all eyes were on Azure - which grew 31% YoY (ahead of expectations closer to 29%). Azure doesn’t disclose exact Azure quarterly revenue (they disclose growth rate in absolute terms and in constant currency), but there are good estimations.

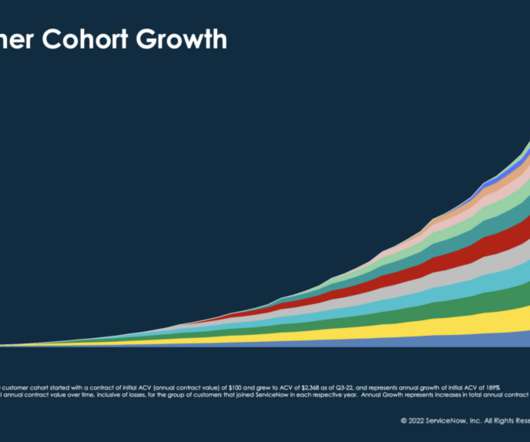

Ok, this chart is a bit confusing, but if you look at ServiceNow’s currency-adjusted revenue, you can see super-consistent 29%-30% growth in subscription revenue each of the past 5 quarters. #2. Enterprises run on ServiceNow. #3. What a visceral comparison to Salesforce, which has seen a dramatic slowdown in enterprise growth.

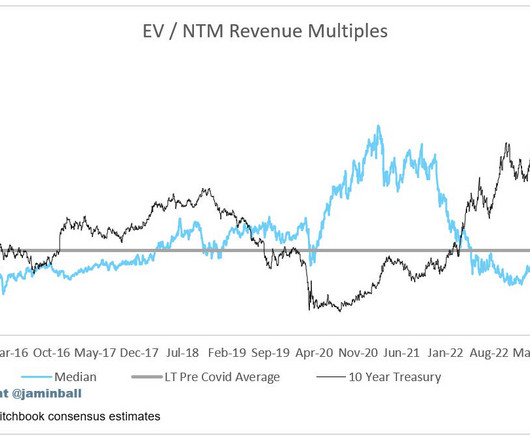

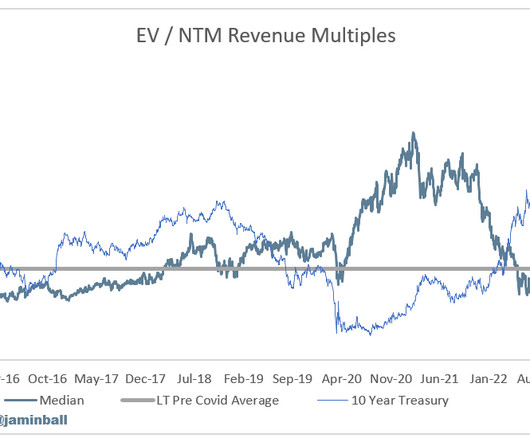

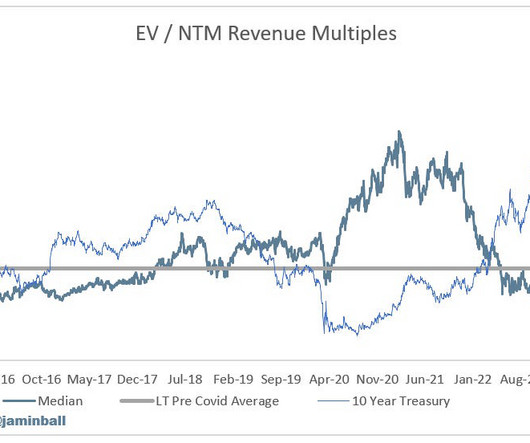

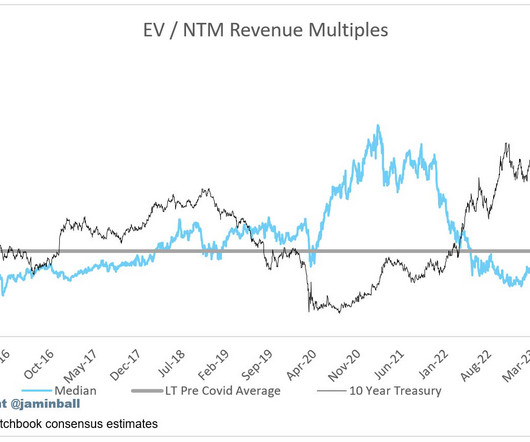

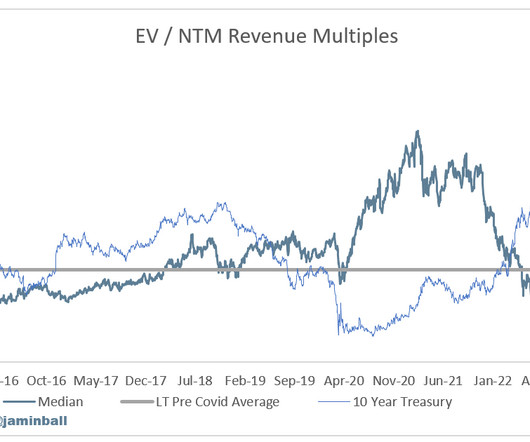

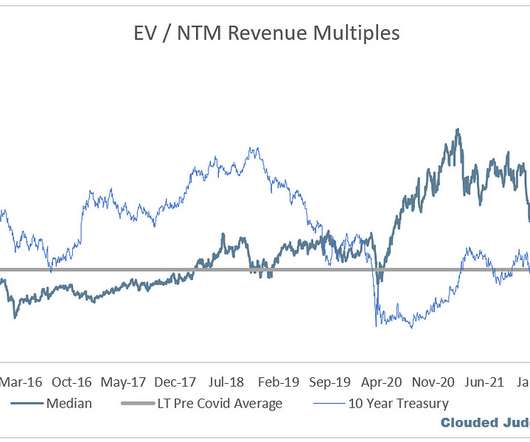

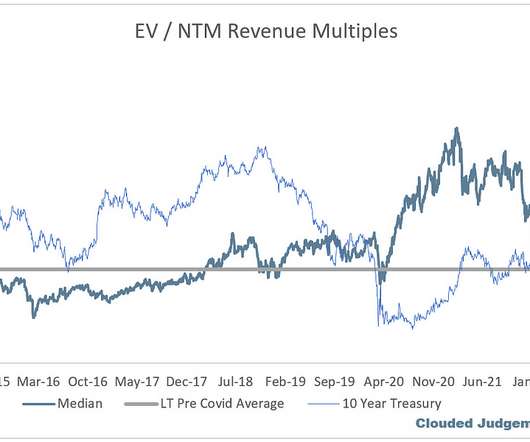

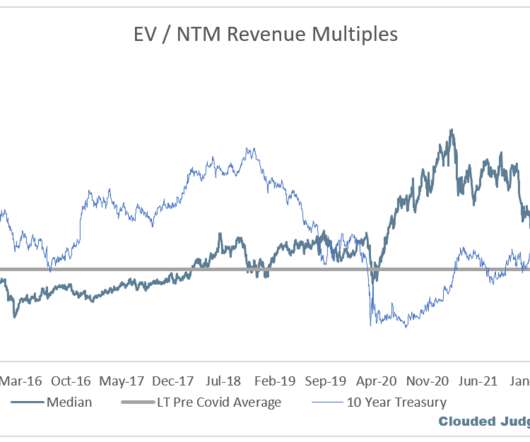

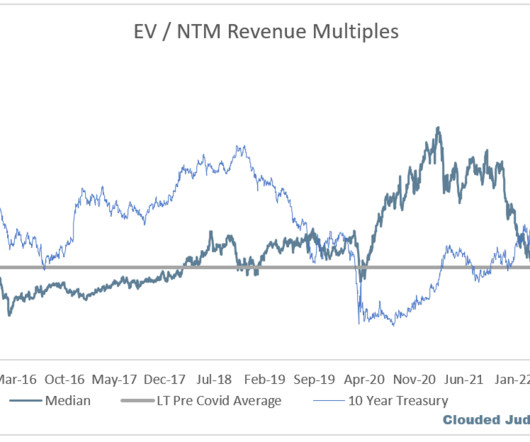

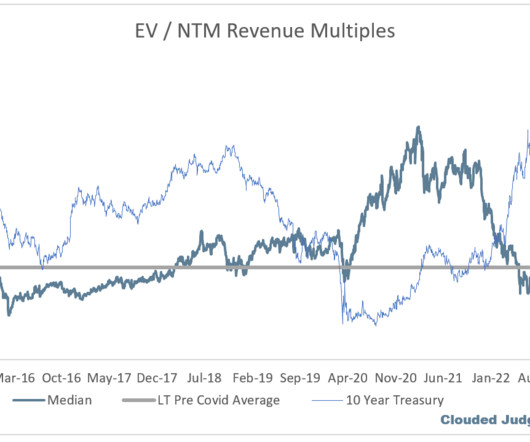

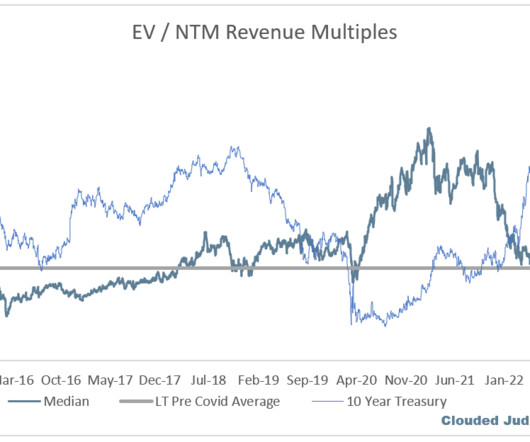

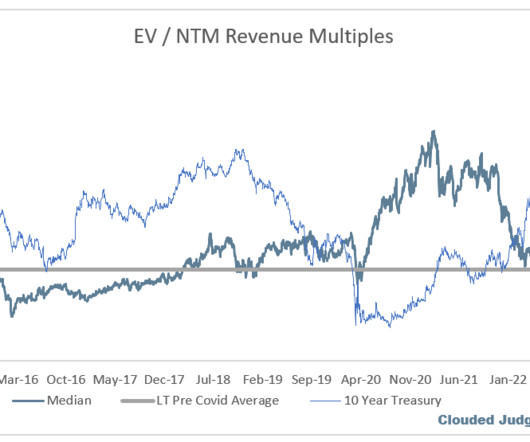

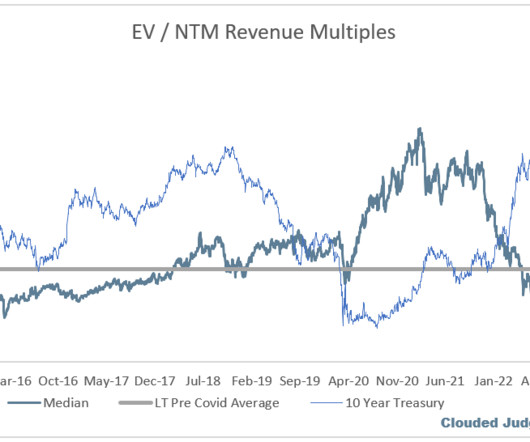

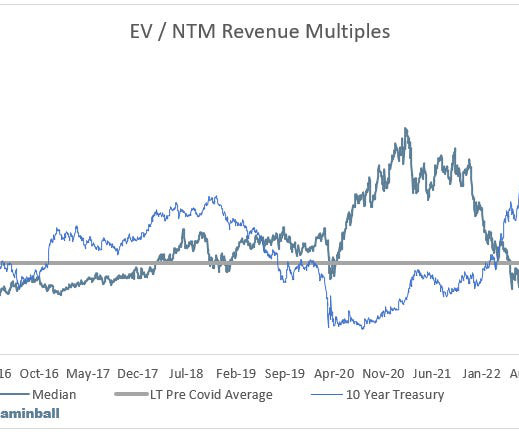

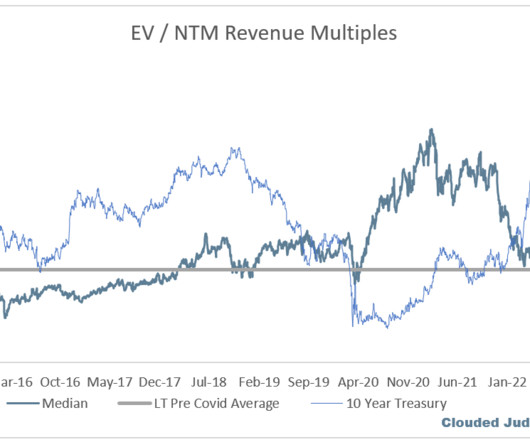

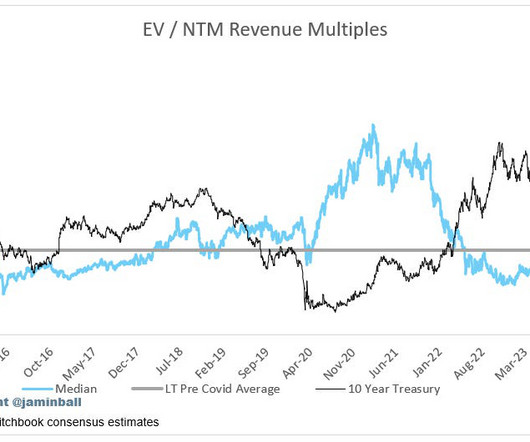

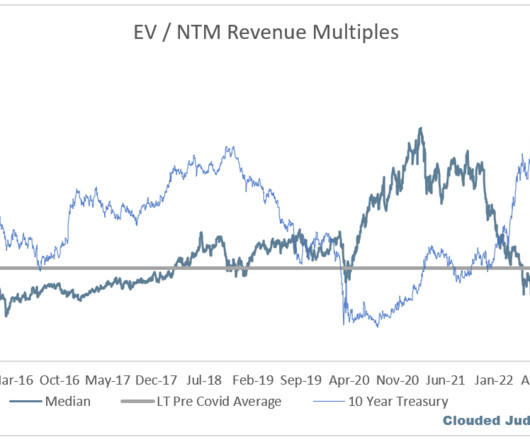

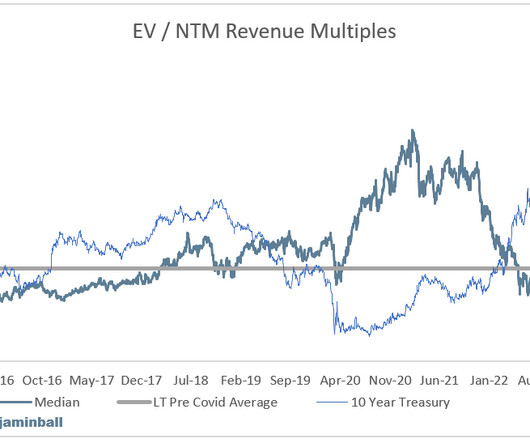

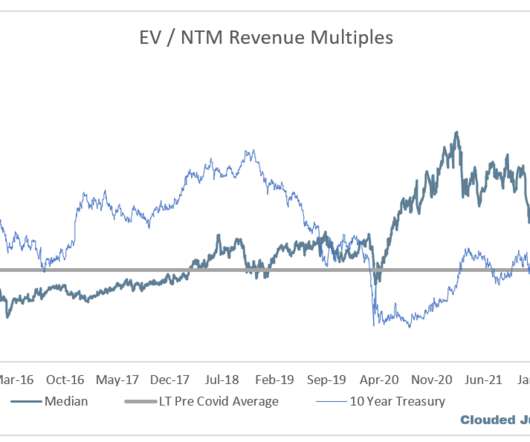

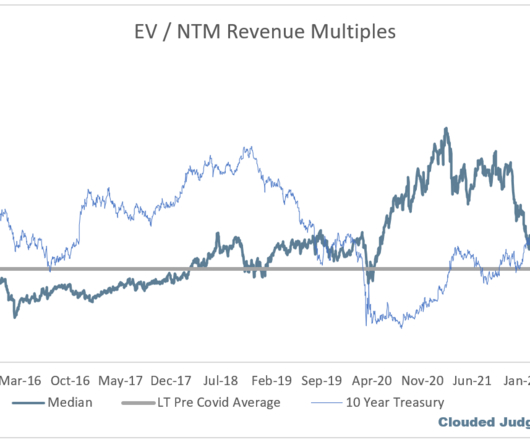

Coming out of that, every company from the largest enterprise to the smallest startup started thinking very critically about cost optimizations. Multiples shown below are calculated by taking the Enterprise Value (market cap + debt - cash) / NTM revenue. So why was it stronger than normal last year? Where was wasted spend with low ROI.

They each have some of the largest cloud businesses in the world in AWS, Azure and Google Cloud respectively. Multiples shown below are calculated by taking the Enterprise Value (market cap + debt - cash) / NTM revenue. Companies that do not disclose subscription rev have been left out of the analysis and are listed as NA.

ChartMogul is an analytics platform to help you run your subscription business. Our mission is to build powerful and secure cloud software for subscription businesses of all sizes, with a strong emphasis on good design and ease of use.

ChartMogul is an analytics platform to help you run your subscription business. Our mission is to build powerful and secure cloud software for subscription businesses of all sizes, with a strong emphasis on good design and ease of use. ChurnZero is the Customer Success platform and partner for growing SaaS and subscription businesses.

Azure’s marketplace has over 4 million monthly visitors. million subscriptions transacted and Google’s marketplace has seen 3X growth in SaaS sales. Rico Mallozzi: So marketplaces are fundamentally changing, go to market motions for a lot of enterprise technology companies. AWS’s marketplace has seen 1.5

Subscribe now Cloud Giants Report Q3 ‘23 Not a great signal for software this week from the Cloud Giants (AWS, Azure and Google Cloud)…After Q2 (3 months ago), the tone from the Cloud Giants around optimizations was largely: optimizations have started to ease, and net new workloads have picked up. Staggering scale already.

” Microsoft on Azure : “And I think last quarter, we said one, we are going to continue to have these cycles where people will build new workloads. Azure (excluding Azure AI) continued to decelerate, and while AWS did come in ahead of expectations, it wasn’t a blow out. Overall Stats: Overall Median: 6.0x

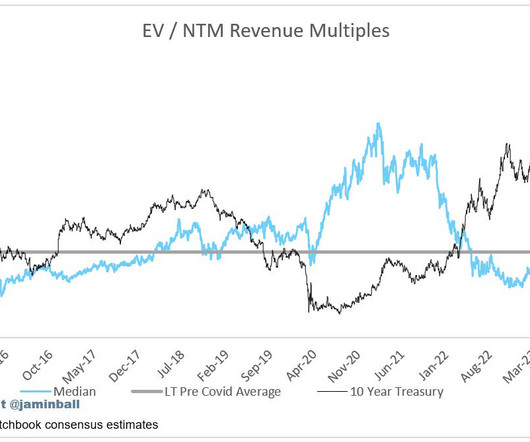

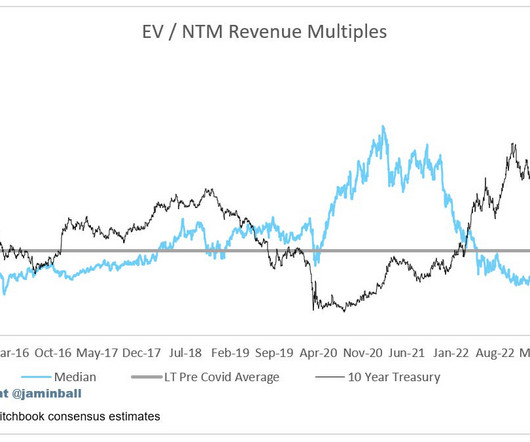

We now have results from the three hypersclaers (AWS / Azure / GCP). Multiples shown below are calculated by taking the Enterprise Value (market cap + debt - cash) / NTM revenue. Most public companies don’t report net new ARR, so I’m taking an implied ARR metric (quarterly subscription revenue x 4).

Hyperscaler Preview Next week Amazon, Microsoft and Google report earnings and we’ll see Q3 data for AWS, Azure and Google Cloud. However, it’s important to keep in mind that while hype and expectations are quite high around AI, true enterprise buying cycles typically lag. Even a DCF is riddled with long term assumptions.

Cloud Downgrades This week UBS came out with a couple research reports citing concerns in AWS / Azure growth. This brings me back to AWS / Azure downgrades. This was the worst tone that we’ve heard in years from large AWS/Azure partners, a group that usually expresses different shades of optimism about AWS/Azure growth.”

SaaS operates on a subscription model, making it easier to manage cash flow and reduce upfront expenses. This democratizes access to powerful tools, whether you’re a startup or an enterprise. Lower upfront costs Say goodbye to expensive licenses and infrastructure costs.

Hyperscalers Report Quarterly Earnings This week we saw AWS (Amazon), GCP (Google) and Azure (Microsoft) report earnings. At the same time, Azure came in below expectations. Azure called out an incremental $800m of costs expected throughout the year (they just finished their Fiscal Q1). Overall Stats: Overall Median: 5.2x

Cloud Giants Report Q2 We also got the Q2 quarters from AWS / Azure / GCP this week! Multiples shown below are calculated by taking the Enterprise Value (market cap + debt - cash) / NTM revenue. Most public companies don’t report net new ARR, so I’m taking an implied ARR metric (quarterly subscription revenue x 4).

Azure (Microsoft) Quarter The week the first of the cloud giants reported - Azure. Early Look at 2023 Guides Given the Azure weakness reported on Tuesday, all software tumbled Wednesday morning with most names down 5-10%. Companies that do not disclose subscription rev have been left out of the analysis and are listed as NA.

AWS (Amazon), Azure (Microsoft), and Google Cloud (Google) all reported this week. Azure reported on Tuesday and gave us that glimmer of hope. Azure : Coming into the quarter, a growth rate that would have satisfied the market would have been ~29%. Azure came in at 31% (constant currency). Follow along to stay up to date!

Microsoft launched Azure in 2010, and Google launched GCP to the public in 2011 (they launched a preview of Google App Engine in 2008, but made it publicly available in 2011). Multiples shown below are calculated by taking the Enterprise Value (market cap + debt - cash) / NTM revenue. Even a DCF is riddled with long term assumptions.

You can see more detail about their net new ARR added each quarter below Azure Growth came in at 27%, and guided to 25-26% growth for Q3. Multiples shown below are calculated by taking the Enterprise Value (market cap + debt - cash) / NTM revenue. Then Q2 came in at 12% (must have seen improvements throughout the quarter).

Usage on Snowflake is driven by queries run on Snowflake Azure: Neutral Tone With Strength in AI Overall I’d characterize Azure’s quarter as a net positive. They guided to 26-27% growth in Azure in Q2 (with 1% coming from AI). Their consumption is driven by usage of applications built on top of Mongo.

All 3 (AWS, Azure, GCP) saw positive reacceleration Quarterly Reports Summary Top 10 EV / NTM Revenue Multiples Top 10 Weekly Share Price Movement Update on Multiples SaaS businesses are generally valued on a multiple of their revenue - in most cases the projected revenue for the next 12 months. Overall Stats: Overall Median: 5.7x

Enterprise software businesses strive for 90-95% gross retention (generally the percent of revenue that sticks with you vs churns altogether), with net expansion in the 120%+ range (the aggregate change in expansion - contraction - churned revenue). .” It’s probably better described as re-occurring vs recurring.

Next week we get all 3 hyperscalers reporting (AWS from Amazon, Azure from Microsoft, and GCP from Google). Let’s double click on Azure. Multiples shown below are calculated by taking the Enterprise Value (market cap + debt - cash) / NTM revenue. Q1 Earnings Season We’re on the eve of Q1 earning season.

AI = Data + Compute I’ll continue beating this drum, but we got two great quotes from Azure and AWS this week. This week we had two of the hypserscalers report (Microsoft / Azure and Google / GCP), and everyone was eager to see their results. Lots to unpack, I’ll hit on a couple of my favorite topics from this week below.

Hyperscalers (AWS, Azure, GCP as companies look for cloud GPUs who aren’t building out their own data centers) Infra (Data layer, orchestration, monitoring, ops, etc) Durable Applications We’ve clearly well underway of the first 3 layers monetizing. Model providers (OpenAI, Anthropic, etc as companies start building out AI).

Zoho Analytics offers four online service plans: Basic : $22 per month Standard : $45 per month Premium : $112 per month Enterprise : $445 per month. Power BI can integrate with Azure Machine Learning—plus, its ML and AI features are driven by Azure functions built into the Azure Cloud. Apache Spark is completely free.

Azure / Confluent / Datadog reported a few weeks back (they all had March quarter ends), and their commentary suggested the worst was behind us. Multiples shown below are calculated by taking the Enterprise Value (market cap + debt - cash) / NTM revenue. This means we got commentary for the first time on May trends. Bucketed by Growth.

This can lead to an airpocket of valuation as companies transition to a different primary valuation metric Outside of the hypserscalers (Azure, AWS, GCP) who have uniquely benefited from AI revenue (mainly selling compute), everyone else has largely struggled. Coming in to Q1 there was broader optimism. Q4’s were generally good!

If next quarter we get similar commentary that Azure gave us this quarter (“still a couple quarters away” without any specific guidance), then we may see market loose a little patience. The hyperscalers (AWS, Azure, GCP) are seeing some uptick, but this is largely from selling compute (ie cloud GPUs). Top 5 Median: 14.4x

Maybe with the exception of hyperscalers (particularly Azure). Multiples shown below are calculated by taking the Enterprise Value (market cap + debt - cash) / NTM revenue. Most public companies don’t report net new ARR, so I’m taking an implied ARR metric (quarterly subscription revenue x 4). Top 5 Median: 13.1x

In the short term, enjoy the ride as the chase continues 😊 Kind of related to all of this - we now have seen the Q4’s from AWS, Azure and Google Cloud. Multiples shown below are calculated by taking the Enterprise Value (market cap + debt - cash) / NTM revenue. Lots of deceleration in growth. Top 5 Median: 14.5x

The pricing model, which leads to increases or decreases in revenue based on how much customers engage with a service, has been gaining on the more traditional subscription model as the main way SaaS companies make money. It has tended to be used most in infrastructure platforms, like AWS, Google Cloud, and Azure. Enterprise companies.

As you can tell, there’s a BIG drop-off projected in 2023 Like Azure, they called for a big slowdown of consumption trends in the month of December. Multiples shown below are calculated by taking the Enterprise Value (market cap + debt - cash) / NTM revenue. However, they guided for 2023 and called for 23-24% growth.

Whether youre a startup , an SMB , or a global enterprise , the right ATS can streamline your recruitment process, save time, and help attract top talent in a competitive market. Lever Best ATS + CRM for Scaling Enterprises Pricing: Key Features: 10. JazzHR Best ATS for Small Business Hiring Pricing Key Features: Ideal Use Case 9.

SaaS companies deliver software applications over the internet on a subscription basis, simplifying access and management for users. SaaS, or Software as a Service, companies host and deliver software applications over the internet on a subscription basis. Primarily through direct-to-user subscriptions and third-party distributors.

As enterprises increasingly become more open to introducing cloud software to their environments, you as a cloud provider must proactively anticipate their concerns and address them. Why are enterprise buyers' concerned about cloud software security? What security questions stop enterprise buyers from buying your cloud software?

Microsoft offers enterprise solutions, productivity suites, and cloud services for both B2B and B2C sectors, emphasizing innovation and efficiency. Oracle ERP provides advanced financial and supply chain optimization, and human resources management for large enterprises in both B2B and B2C sectors. Microsoft Dynamics 365.

As enterprises increasingly become more open to introducing cloud software to their environments, you as a cloud provider must proactively anticipate their concerns and address them. Why are enterprise buyers' concerned about cloud software security? What security questions stop enterprise buyers from buying your cloud software?

Traditional pricing models, such as fixed subscriptions and one-time purchases, no longer align with the dynamic and ever-evolving nature of this sector. Take your business further with BluIQ’s flexible, scalable, enterprise-grade intelligent billing solutions.

Margaret Rouse of TechTarget defines role-based access control as a method of restricting network access based on the roles of individual users within an enterprise. For example, with Azure RBAC you can: Allow one user to manage virtual machines in a subscription and another user to manage virtual networks.

Qualys may be a decent choice for enterprise software teams looking for a robust and reliable WAF solution. It helps some large enterprises maintain a strong cloud security status by identifying and remediating misconfigurations, monitoring user activity, and detecting threats in real-time.

While they often went head-to-head in competitive situations, Apttus targeted the enterprise whereas Steelbrick targeted the mid-market. Apttus built their applications on the Microsoft Azure platform with the goal of opening new markets, specifically with Microsoft Dynamics CRM. In early 2016, Salesforce acquired Steelbrick.

Self-hosted SaaS environments that don’t leverage third-party vendors must also proportionally split their self-hosting expenses between company use for business operation and customer subscription platform usage. . Professional services are billable implementation and customization services sold to customers.

Cloud computing services provide on-demand solutions and IT resources to companies via the Internet with pay-as-you-go or subscription-based pricing models. Enterprises can buy or lease only the services they need, thus reducing maintenance and upfront charges. SaaS Characteristics Subscription-based pricing model.

We organize all of the trending information in your field so you don't have to. Join 80,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content