This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

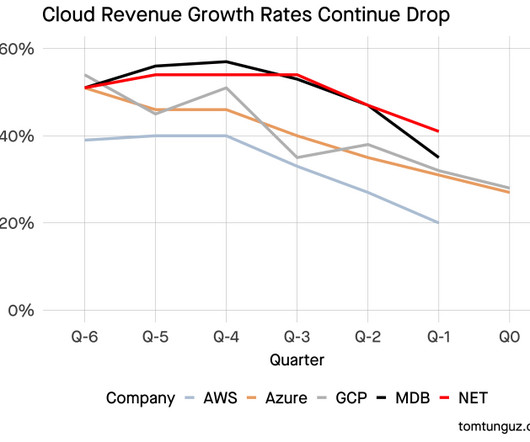

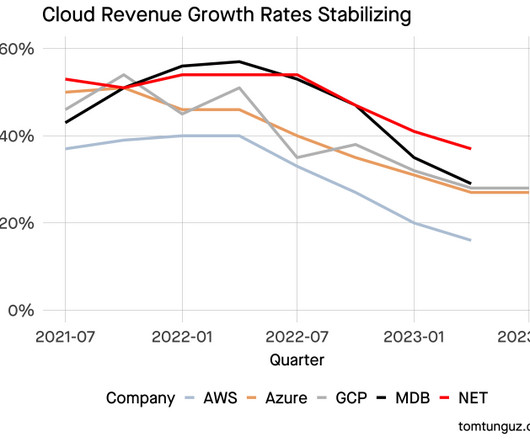

Subscribe now Azure Report - Cloud Infra Looks Good! For software, all eyes were on Azure - which grew 31% YoY (ahead of expectations closer to 29%). Azure doesn’t disclose exact Azure quarterly revenue (they disclose growth rate in absolute terms and in constant currency), but there are good estimations.

I’m watching public company earnings to identify early trends in the software market to inform startups’ plans for 2023. Google Cloud Platform (GCP) & Microsoft Azure had strong quarters with about 28% annual revenue growth each. The total customer count for Azure’s OpenAI has grown dramatically.

It’s worth pointing out that Azure is a bit above the long term trendline, while AWS is still below (but accelerating up). It’s worth pointing out that Azure is a bit above the long term trendline, while AWS is still below (but accelerating up). After earnings, that perception either changed positively or negatively.

We saw moderated consumption growth in Azure and lower-than-expected growth [elsewhere]. Segment Expected Growth Productivity 12% Office Commercial 6% Office On-Premise -25% LinkedIn 5% Dynamics 13% Intelligent Cloud 18% Azure 26% Server -3% Services -3% 2. At some point, the optimizations will end.

They each have some of the largest cloud businesses in the world in AWS, Azure and Google Cloud respectively. The information provided is believed to be from reliable sources but no liability is accepted for any inaccuracies. This is for information purposes and should not be construed as an investment recommendation.

The hyperscalers (AWS, Azure, GCP) are always some of the first companies to report earnings during earnings season (coming up in 2 weeks), and there’s always a read through for consumption names (meaning people believe there’s a correlation). This post and the information presented are intended for informational purposes only.

I’m watching public company earnings to identify early trends in the software market to inform startups’ plans for 2023. Both Google & Microsoft announced growth rates in GCP & Azure that held steady from one quarter to the next. Yesterday, Microsoft & Google announced earnings. The desire for AI is broad.

Some well-known providers of SSO include Google Cloud Identity for companies using GSuite, Azure Active Directory for companies using Office 365, and Okta if you’re a larger company with more complex needs. . For password management, 1Password and LastPass are popular options. 3 – Get a Mobile Device Management (MDM) Solution.

With a PLG-heavy background, first working at Microsoft Azure and again with Atlassian, the PLG pioneers, he gives insights into leveraging PLG for the growth of your organization. Atlassian, Microsoft Azure, and Zoom are good examples of that. How PLG Evolved First, let’s start with PLG and its evolution. It’s not fully self-serve.

Subscribe now Cloud Giants Report Q3 ‘23 Not a great signal for software this week from the Cloud Giants (AWS, Azure and Google Cloud)…After Q2 (3 months ago), the tone from the Cloud Giants around optimizations was largely: optimizations have started to ease, and net new workloads have picked up. Staggering scale already.

” Microsoft on Azure : “And I think last quarter, we said one, we are going to continue to have these cycles where people will build new workloads. Azure (excluding Azure AI) continued to decelerate, and while AWS did come in ahead of expectations, it wasn’t a blow out.

I’m watching public company earnings to identify early trends in the software market to inform startups’ plans for 2023. Yesterday, Cloudflare announced earnings. I’m adding Cloudflare to the list of tracked companies for this series.

We now have results from the three hypersclaers (AWS / Azure / GCP). The information provided is believed to be from reliable sources but no liability is accepted for any inaccuracies. This is for information purposes and should not be construed as an investment recommendation.

Growth + Margin = Above 40%) versus Non-Qualifiers (Below 40%): Given the wealth of information presented by KBCM, we examined the material differences. You can’t pay your Azure bill or office lease in “Rule of 40” points. KBCM helpfully presents a very detailed comparison of “Rule of 40” Qualifiers (i.e.

Hyperscaler Preview Next week Amazon, Microsoft and Google report earnings and we’ll see Q3 data for AWS, Azure and Google Cloud. The information provided is believed to be from reliable sources but no liability is accepted for any inaccuracies. This post and the information presented are intended for informational purposes only.

It looks at the YoY dollar change in quarterly revenue from the hyperscalers (just looking at Azure / AWS because the data goes back further) going back a few years. If we break this down and look at Azure and AWS independently (graphs below), you’ll see how the AWS “swings” were a lot more volatile.

Azure’s marketplace has over 4 million monthly visitors. And a lot of this depends on your go to market, but we are selling jointly with the AWS and the Azure, et cetera sellers too. Announcer: Visit Dell.com/SaaStr for exclusive savings on Dell products and more information about the Dell for entrepreneurs program.

AWS (Amazon), Azure (Microsoft), and Google Cloud (Google) all reported this week. Azure reported on Tuesday and gave us that glimmer of hope. Azure : Coming into the quarter, a growth rate that would have satisfied the market would have been ~29%. Azure came in at 31% (constant currency). Follow along to stay up to date!

Cloud Giants Report Q2 We also got the Q2 quarters from AWS / Azure / GCP this week! The information provided is believed to be from reliable sources but no liability is accepted for any inaccuracies. This is for information purposes and should not be construed as an investment recommendation.

Cloud Downgrades This week UBS came out with a couple research reports citing concerns in AWS / Azure growth. This brings me back to AWS / Azure downgrades. This was the worst tone that we’ve heard in years from large AWS/Azure partners, a group that usually expresses different shades of optimism about AWS/Azure growth.”

You give the model information and what you’re trying to predict. Then, it takes that information and makes a prediction. So, if you have bad or dirty examples where a negative case isn’t as informative as an almost positive one, you’ll struggle. When you train a model, it’s trial and error.

Only 1 in 3 buyers consider vendor websites the information source they trust most.”. The role of AWS, Azure, and Google Cloud Marketplace is becoming increasingly important. “45% Today, the focus is less on companies advocating for themselves but rather on building people advocates.

Hyperscalers Report Quarterly Earnings This week we saw AWS (Amazon), GCP (Google) and Azure (Microsoft) report earnings. At the same time, Azure came in below expectations. Azure called out an incremental $800m of costs expected throughout the year (they just finished their Fiscal Q1).

Azure (Microsoft) Quarter The week the first of the cloud giants reported - Azure. Early Look at 2023 Guides Given the Azure weakness reported on Tuesday, all software tumbled Wednesday morning with most names down 5-10%. This post and the information presented are intended for informational purposes only.

In comparing the two most recent Microsoft earnings calls, Claude highlighted: faster than expected Azure growth (29% vs 27%) AI contributing 8% of Azure revenue up from 7% higher CapEx spending & greater capacity constraints for data centers much better commercial bookings growth : 17% vs 13% Excellent analysis.

Microsoft launched Azure in 2010, and Google launched GCP to the public in 2011 (they launched a preview of Google App Engine in 2008, but made it publicly available in 2011). The information provided is believed to be from reliable sources but no liability is accepted for any inaccuracies.

You can see more detail about their net new ARR added each quarter below Azure Growth came in at 27%, and guided to 25-26% growth for Q3. This post and the information presented are intended for informational purposes only. Then Q2 came in at 12% (must have seen improvements throughout the quarter).

Usage on Snowflake is driven by queries run on Snowflake Azure: Neutral Tone With Strength in AI Overall I’d characterize Azure’s quarter as a net positive. They guided to 26-27% growth in Azure in Q2 (with 1% coming from AI). This post and the information presented are intended for informational purposes only.

From data encryption to access controls, your information stays protected and compliant, giving you peace of mind. Building integrations with popular tools like Google Workspace, Slack, Microsoft Azure, or project management software enables your SaaS product to fit seamlessly into existing workflows.

AI = Data + Compute I’ll continue beating this drum, but we got two great quotes from Azure and AWS this week. This week we had two of the hypserscalers report (Microsoft / Azure and Google / GCP), and everyone was eager to see their results. This post and the information presented are intended for informational purposes only.

Retrieval-Augmented Generation (RAG) is a cutting-edge approach in AI that combines large language models (LLMs) with real-time information retrieval to produce more accurate and context-aware outputs. Think of a standard LLM as a very smart student who has learned a lot of general information. This is known as AI hallucination.

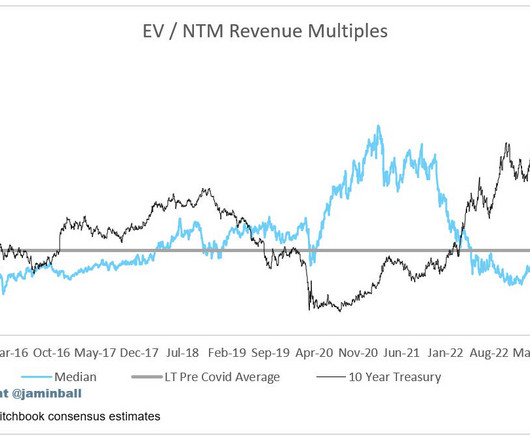

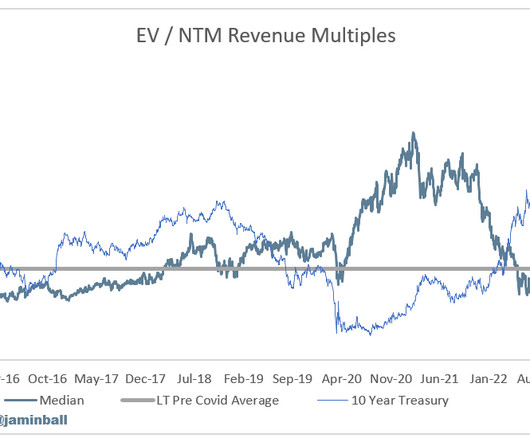

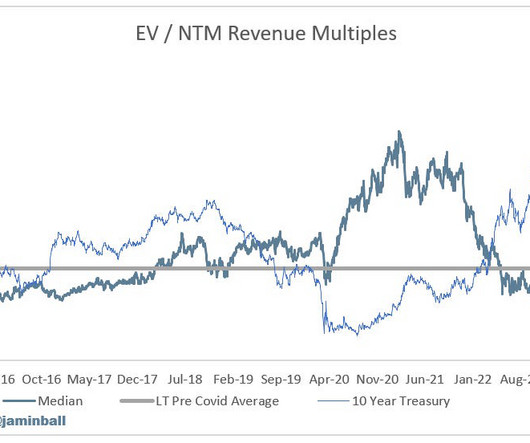

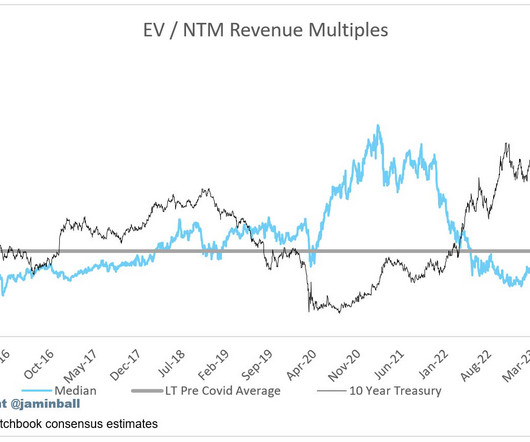

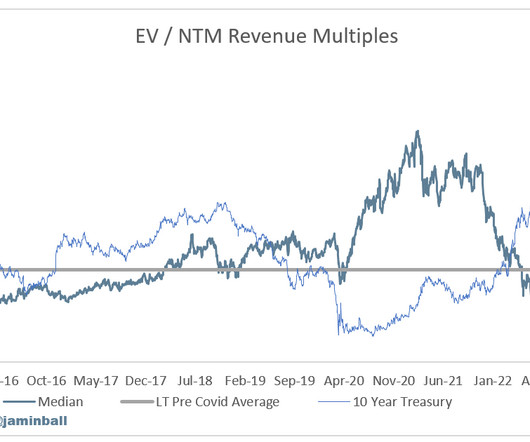

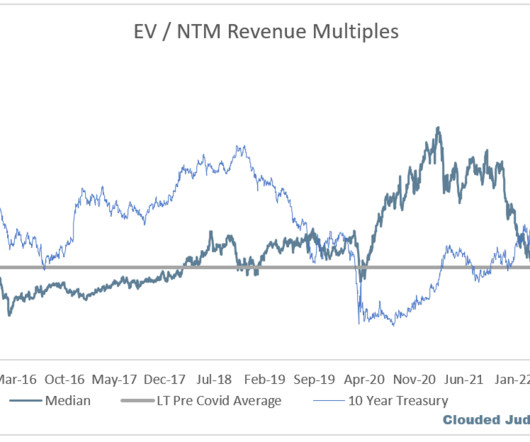

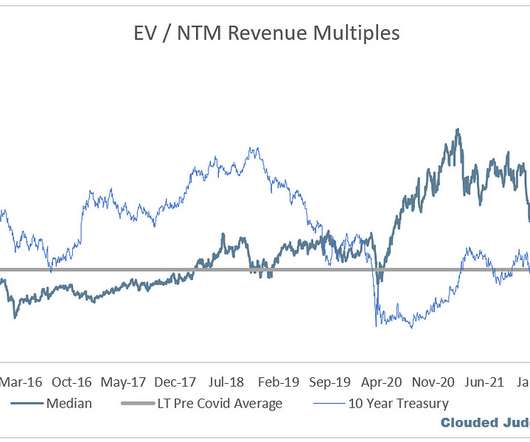

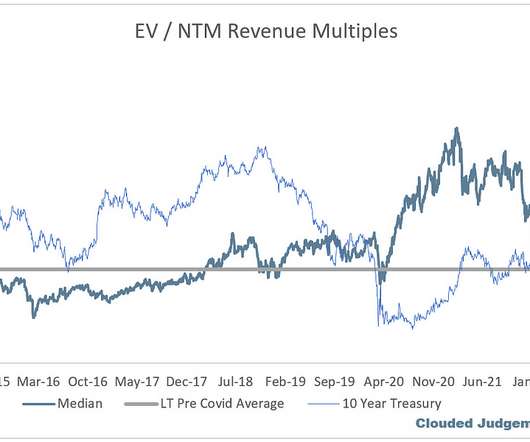

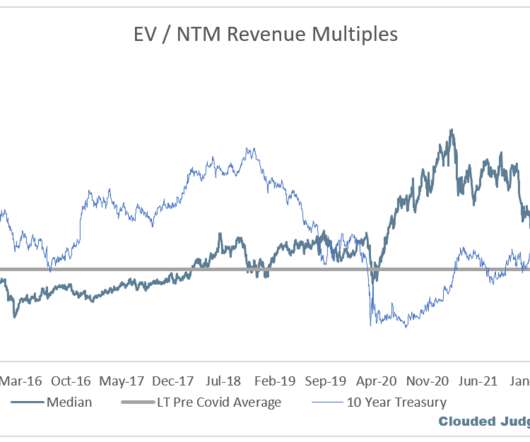

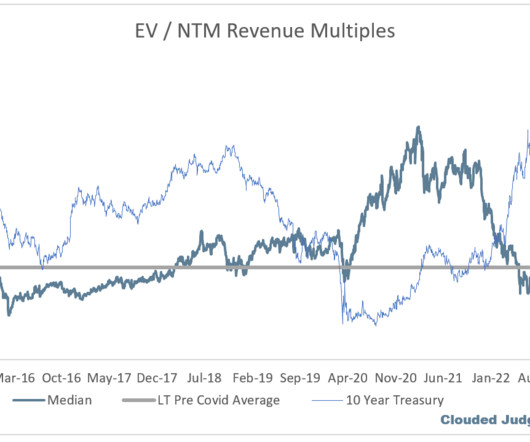

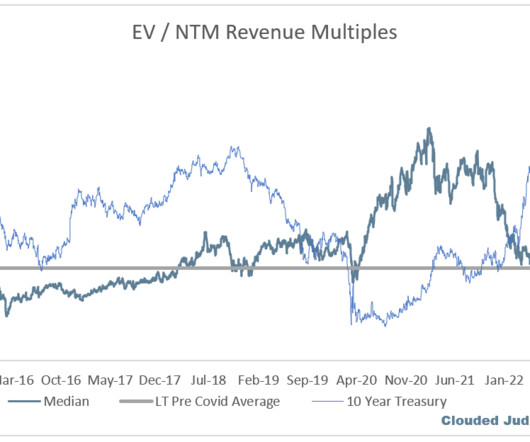

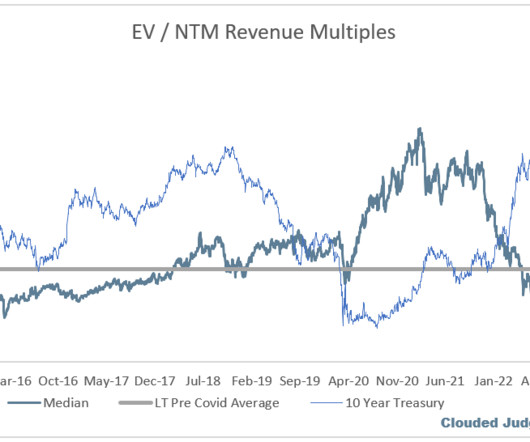

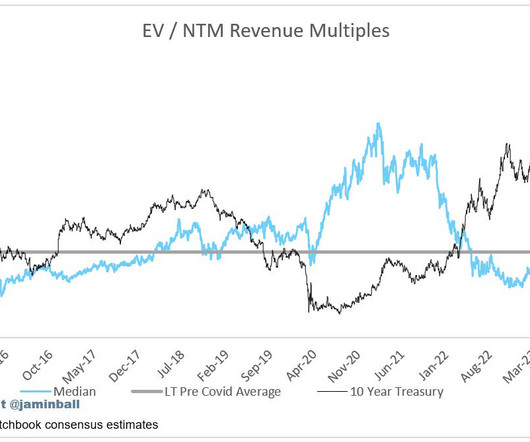

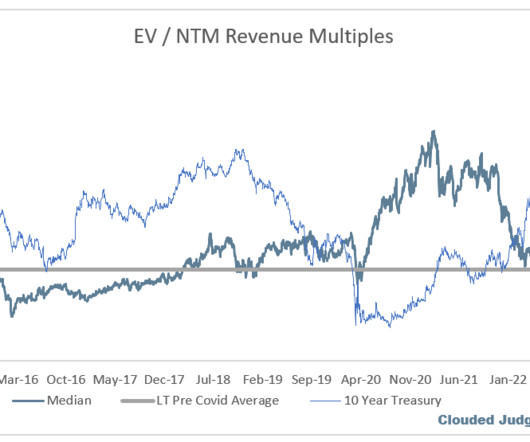

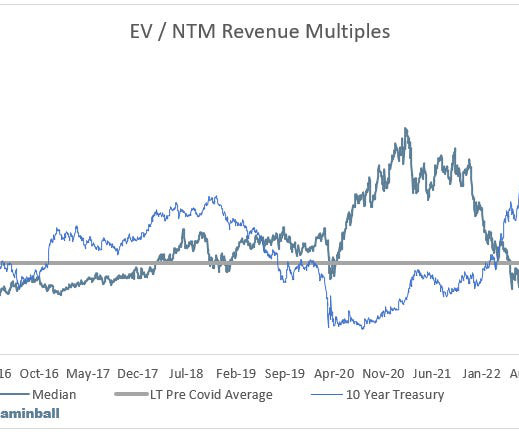

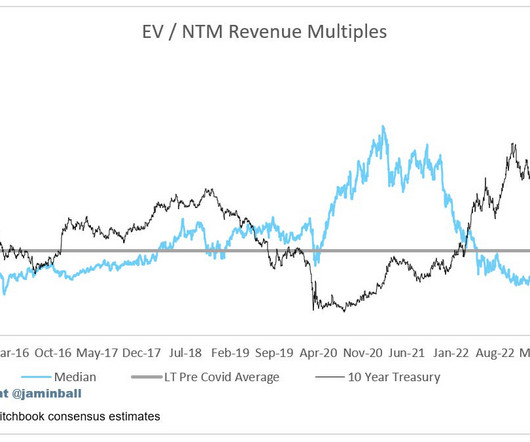

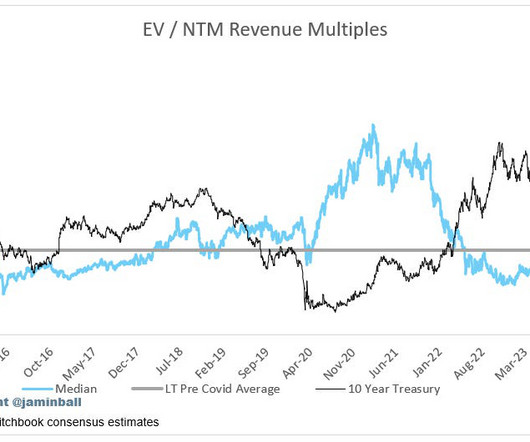

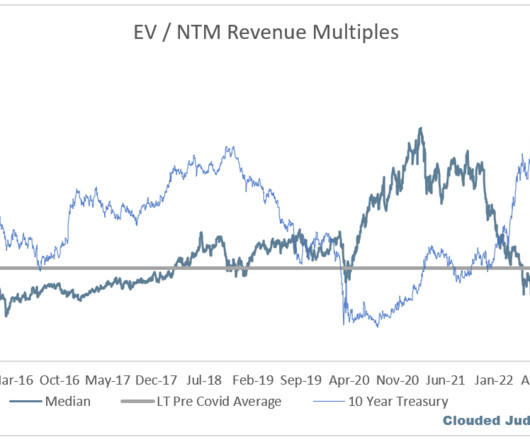

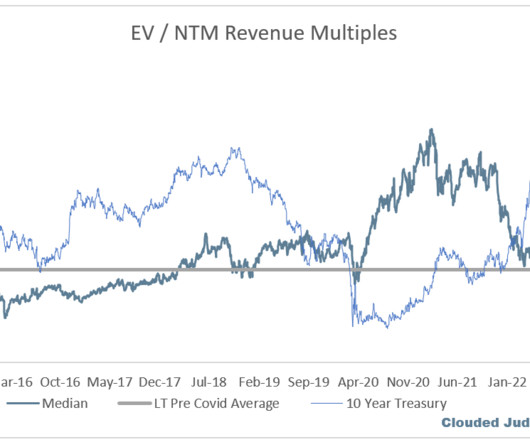

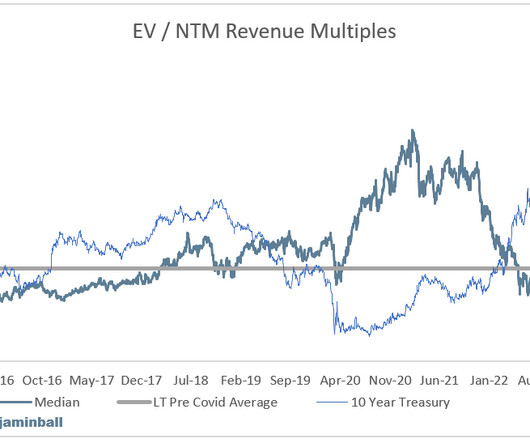

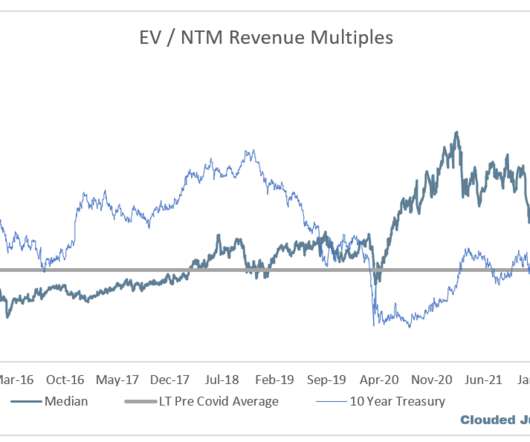

All 3 (AWS, Azure, GCP) saw positive reacceleration Quarterly Reports Summary Top 10 EV / NTM Revenue Multiples Top 10 Weekly Share Price Movement Update on Multiples SaaS businesses are generally valued on a multiple of their revenue - in most cases the projected revenue for the next 12 months.

Next week we get all 3 hyperscalers reporting (AWS from Amazon, Azure from Microsoft, and GCP from Google). Let’s double click on Azure. This post and the information presented are intended for informational purposes only. Q1 Earnings Season We’re on the eve of Q1 earning season.

Hyperscalers (AWS, Azure, GCP as companies look for cloud GPUs who aren’t building out their own data centers) Infra (Data layer, orchestration, monitoring, ops, etc) Durable Applications We’ve clearly well underway of the first 3 layers monetizing. Model providers (OpenAI, Anthropic, etc as companies start building out AI).

Pepper Money’s chief information officer, Jeremy Francis told CIO Australia that the organisation had several vendors providing different services. He said some services were not being used, and a more simplified and resilient IT environment that supported staff, third party brokers and external customers was needed.

This is why the consumption players (Snowflake, Mongo, Confluent, Azure, AWS, etc) so more variability in the macro slowdown. The information provided is believed to be from reliable sources but no liability is accepted for any inaccuracies. This is for information purposes and should not be construed as an investment recommendation.

This can lead to an airpocket of valuation as companies transition to a different primary valuation metric Outside of the hypserscalers (Azure, AWS, GCP) who have uniquely benefited from AI revenue (mainly selling compute), everyone else has largely struggled. Coming in to Q1 there was broader optimism. Q4’s were generally good!

On the other hand, inferential analysis software takes in your sample information for making useful and reliable generalizations. The software then uses all this information to create powerful drop-and drag reports. As pricing information is unavailable on its website, you’ll have to contact the sales professional to request a quote.

SEO schema : If you have schema in place, the product information will get you in the SERPs, allowing you to rank among your competitors. Ratings, reviews, and FAQs : Since 77% of customers regularly read reviews , help your customer make a sound decision by having additional information to increase their chances of converting.

If next quarter we get similar commentary that Azure gave us this quarter (“still a couple quarters away” without any specific guidance), then we may see market loose a little patience. The hyperscalers (AWS, Azure, GCP) are seeing some uptick, but this is largely from selling compute (ie cloud GPUs).

GASB standards require that interdepartmental or interagency transactions be supported by: Accurate cost allocation Documented pricing logic Audit trails Ledger-ready entries Informal internal billing processesespecially those reliant on manual reporting or static spreadsheetsoften fall short of these standards.

Azure / Confluent / Datadog reported a few weeks back (they all had March quarter ends), and their commentary suggested the worst was behind us. This post and the information presented are intended for informational purposes only. This means we got commentary for the first time on May trends.

Maybe with the exception of hyperscalers (particularly Azure). Sources used in this post include Bloomberg, Pitchbook and company filings The information presented in this newsletter is the opinion of the author and does not necessarily reflect the view of any other person or entity, including Altimeter Capital Management, LP ("Altimeter").

In the short term, enjoy the ride as the chase continues 😊 Kind of related to all of this - we now have seen the Q4’s from AWS, Azure and Google Cloud. This post and the information presented are intended for informational purposes only. Lots of deceleration in growth.

We organize all of the trending information in your field so you don't have to. Join 80,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content