This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

For software companies, this phenomenon can be a tailwind, as it drives accelerated deal closures and increased sales velocity, sometimes with less price sensitivity from buyers looking to quickly deplete their budgets. As we head into the end of 2024 I wonder if a similar, but even stronger, budget flush will play out.

Great for small to medium teams with a pay-as-you-go pricing model. Quick Comparison Tool Key Features Pricing Ideal For Middleware Real-time alerts, root cause analysis Free tier; $0.30/GB The importance of such rapid alerting was highlighted during the CrowdStrike outage in July 2024, emphasizing the need for swift responses.

Google Cloud , Azure, and GitLab, all tied directly or indirectly to AI, are seeing massive acceleration. But Google Cloud, Azure, and GitLab are all benefiting and on fire. The New Era of Hyperfunctional SaaS: 2024-2029 So what are the pillars to operating as a Hyperfunctional SaaS company? #1: Is there a bubble?

Single Sign-On & Authentication Integrations : SSO integration (Okta, Azure AD, etc.) Continuous News & Improvements: The press page shows multiple press releases about acquisitions and product updates – e.g., ProProfs acquiring WebinarNinja in 2024 and Qualaroo in 2020. connects your knowledge base with your identity system.

Azure 26 33 26.9% Cloud Operating Margin Azure 44% AWS 38% GCP 17% Plus the operating margins of these companies is massive at around 40% for the top two. The second version of Trainium, Trainium2, is starting to ramp up in the next few weeks and will be very compelling for customers on price performance.” GCP 23 35 52.2%

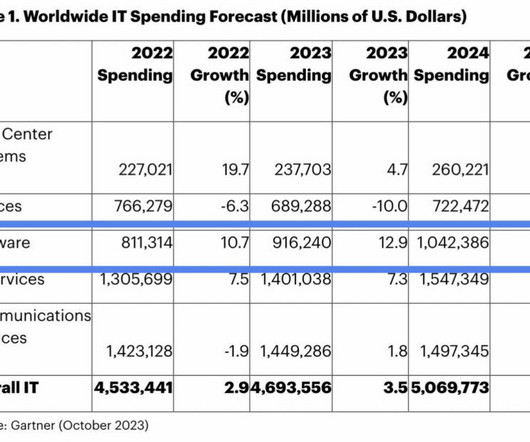

On top of that, inflation and price increases are eating into overall IT budgets. In fact, In fact, Gartner sees overall global software spend growing faster in 2024 than 2023, a very health +13.8% — and crossing $1 Trillion in total spend for the first time! So where does this all net out? With some big caveats.

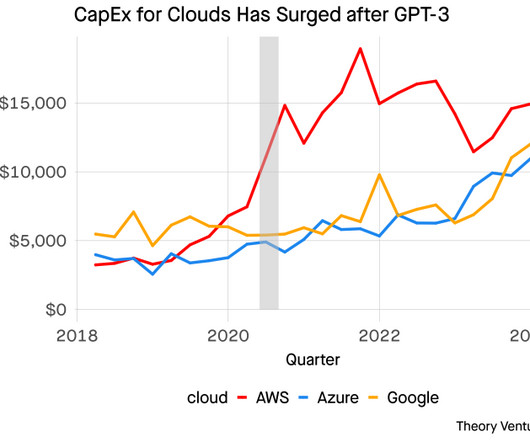

Cloud Capex in Q1 AWS $14 billion Azure $14 billion Google Cloud $12 billion These are not one-time investments, but part of a broader trend that started to occur after the introduction of GPT 3 in mid-2020 Amazon was the first to invest significantly. 8 percentage points increased margins in a quarter is titanic.

It’s worth pointing out that Azure is a bit above the long term trendline, while AWS is still below (but accelerating up). It’s worth pointing out that Azure is a bit above the long term trendline, while AWS is still below (but accelerating up). Let’s get into some high level data.

Subscribe now Cloud Giants Report Q3 ‘23 Not a great signal for software this week from the Cloud Giants (AWS, Azure and Google Cloud)…After Q2 (3 months ago), the tone from the Cloud Giants around optimizations was largely: optimizations have started to ease, and net new workloads have picked up. Staggering scale already.

This has all resulted in the median stock price declining 5% YTD. It looks at the YoY dollar change in quarterly revenue from the hyperscalers (just looking at Azure / AWS because the data goes back further) going back a few years. Heading into Q4 earnings, analysts had expectations for how each business would perform in 2024.

AWS (Amazon), Azure (Microsoft), and Google Cloud (Google) all reported this week. Azure reported on Tuesday and gave us that glimmer of hope. Azure : Coming into the quarter, a growth rate that would have satisfied the market would have been ~29%. Azure came in at 31% (constant currency). Follow along to stay up to date!

In 2024, we believe the revenue opportunity will be multiples larger in the enterprise. Moreover, nearly every single enterprise we spoke with saw promising early results of genAI experiments and planned to increase their spend anywhere from 2x to 5x in 2024 to support deploying more workloads to production.

Said another way, I believe that software valuations were holding up so well in the face of a ~5% 10Y because the market expected acceleration and 2024 numbers to come up. Maybe with the exception of hyperscalers (particularly Azure). And now, it’s unclear when that re-acceleration will happen. And the median guide is 0.4%

Azure / Confluent / Datadog reported a few weeks back (they all had March quarter ends), and their commentary suggested the worst was behind us. An element of re-acceleration is definitely priced in to current 2024 estimates, so we may see 2024 estimates fall. This means we got commentary for the first time on May trends.

Next week we get all 3 hyperscalers reporting (AWS from Amazon, Azure from Microsoft, and GCP from Google). Let’s double click on Azure. ” They anticipate Q1 will be the peak pressure on cloud spend, and we may see a re-acceleration heading into 2024. Q1 Earnings Season We’re on the eve of Q1 earning season.

A 2023 recession feels less likely, with 2024 being the more realistic timing if we do in fact get to a deeper recession. There’s a real chance the fed funds rate isn’t going >5%, and a soft landing or delayed recession is certainly possible (maybe even being priced in). But what’s happened since?

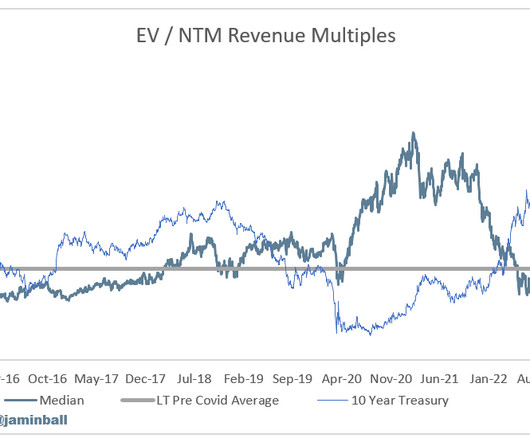

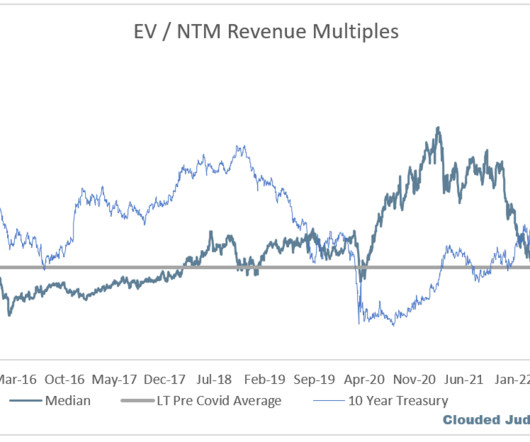

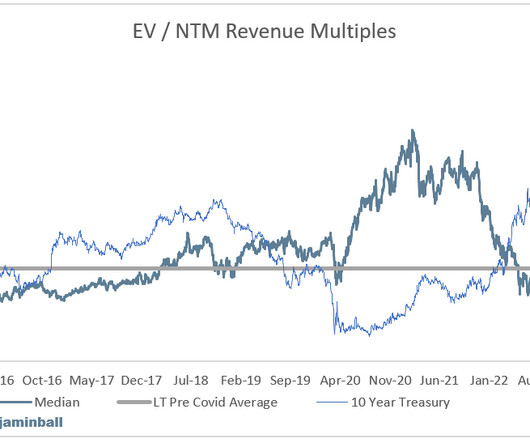

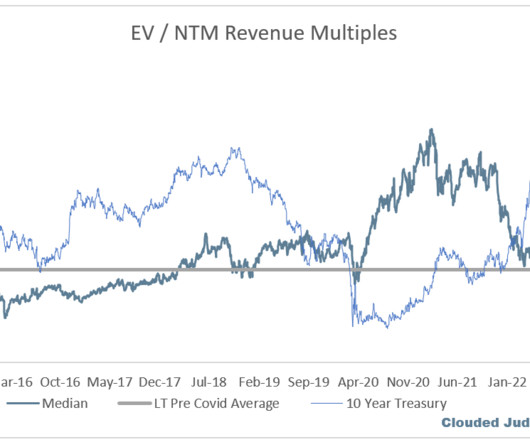

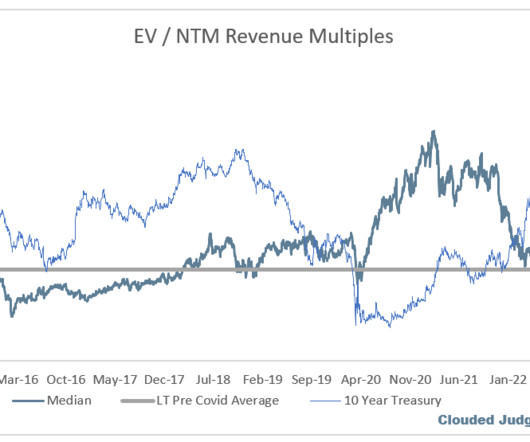

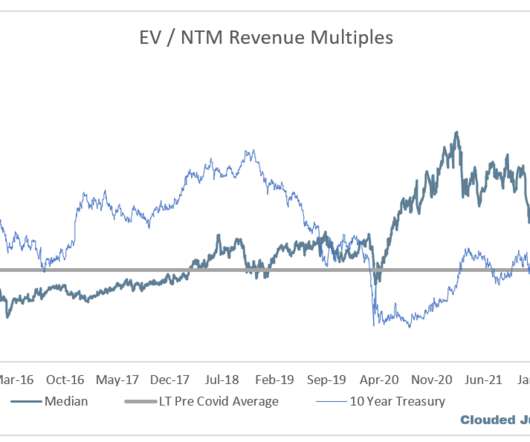

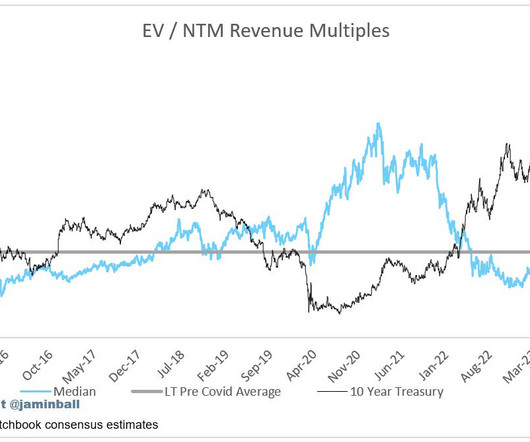

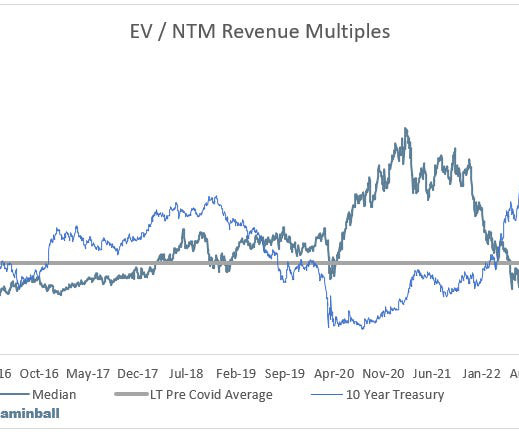

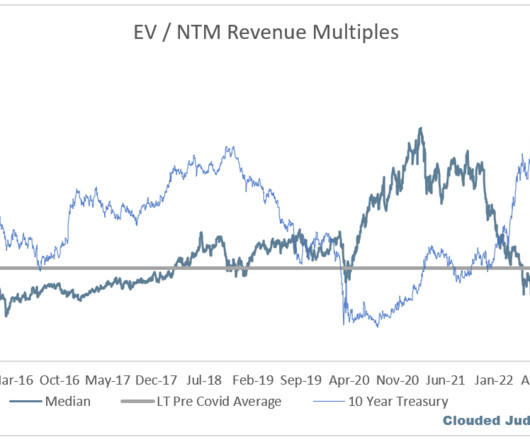

All 3 (AWS, Azure, GCP) saw positive reacceleration Quarterly Reports Summary Top 10 EV / NTM Revenue Multiples Top 10 Weekly Share Price Movement Update on Multiples SaaS businesses are generally valued on a multiple of their revenue - in most cases the projected revenue for the next 12 months.

Hyperscalers (AWS, Azure, GCP as companies look for cloud GPUs who aren’t building out their own data centers) Infra (Data layer, orchestration, monitoring, ops, etc) Durable Applications We’ve clearly well underway of the first 3 layers monetizing. 2024 will be the year of AI applications!

If next quarter we get similar commentary that Azure gave us this quarter (“still a couple quarters away” without any specific guidance), then we may see market loose a little patience. The hyperscalers (AWS, Azure, GCP) are seeing some uptick, but this is largely from selling compute (ie cloud GPUs).

SaaStr founder and CEO Jason Lemkin shares his take on the current SaaS landscape midway through 2024 and what might be coming next in 2025 at the opener to this year’s SaaStr Europa. Maybe endless price increases,” Jason says. You can see the growth on the platform side with Azure, Google, and AWS and how much it’s accelerating in AI.

Offer customized pricing models or add-on services that align with the specific needs and budgets of different customer segments. Microsoft Azure: Microsoft Azure offers a wide range of cloud services, including computing, analytics, storage, and networking. Scientific Research Publishing, [link] Accessed 11 September 2024.

Key examples are Amazon Web Services (AWS), Microsoft Azure, and Google Cloud Platform, which provide scalable resources like virtual servers and storage. Most SaaS companies offer a scalable pricing model that adjusts based on usage – ideal for managing budgets effectively. What are the benefits of the SaaS model?

Offer customized pricing models or add-on services that align with the specific needs and budgets of different customer segments. Microsoft Azure: Microsoft Azure offers a wide range of cloud services, including computing, analytics, storage, and networking. Scientific Research Publishing, [link] Accessed 11 September 2024.

Platforms like Microsoft Azure or Amazon Web Services are good examples in this regard. Plus, check out how similar services are priced. It may be a good idea to plan out different pricing levels if that makes sense. It ensures a steady revenue stream and the ability to update features without user intervention.

Pro (Feb 2024) matched Gemini 1.0 In 2024 Anthropic released Claude 3 (family: Opus, Sonnet, Haiku) , and in 2025 Claude 4 (Opus 4 & Sonnet 4). In April 2024 Meta released Llama 3 with 8B and 70B parameter versions, trained on ~15 trillion tokens. In late 2024 they launched Mistral Large 24.11 (123B parameters).

” “Azure OpenAI usage more than doubled over the past 6 months” “GitHub Copilot enterprise customers increased 55% quarter-over-quarter” Google on AI “Gemini API calls have grown nearly 14x in a 6-month period.” This will be the fastest business in our history to reach this milestone.”

Access and integration : Some LLMs offer public APIs or cloud deployment (ChatGPT, Claude, Mistral on Azure), while open models can be self-hosted. LLM Performance Benchmark Comparison (2025) Model MMLU HumanEval GSM8K / AIME Context Window Token Speed Pricing (per 1M tokens) DeepSeek R1-0528 84.9% Pricing per token is tiered (e.g.

We organize all of the trending information in your field so you don't have to. Join 80,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content