This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Let’s be honest: payments used to be a pain. If you’re a SaaS founder, product leader, or engineer, you’ve probably stared down the barrel of a tangled payment integration wondering, “Why does something so essential feel so unnecessarily complicated?” The truth is, the world of embeddedpayments has evolved—dramatically.

If you’re building an AI-powered SaaS product, your focus is likely on creating amazing AI features — whether that’s smart automation, AI co-pilots, or data-driven insights. More than that, how you can embed payments seamlessly inside your app to deliver a smooth user experience and open new revenue streams.

You’re here because someone—maybe your CEO, maybe your investor, maybe your gut—told you that owning payments could be a game-changer for your platform. But here’s the part that gets glossed over: how you own payments matters. Should you become a full PaymentFacilitator (PayFac)? They’re right. You control the flow.

The embedded finance market—including Payfac-as-a-Service—is projected to exceed $7 trillion in global transaction volume by 2030. I f you’re running a SaaS platform, marketplace, or digital-first business, you’ve probably already bumped into the complexities of paymentprocessing. What Is Payfac-as-a-Service?

What is a payment processor? A payment processor facilitates the flow of transactions typically made with credit cards, debit cards, and other digital payments. The processor is responsible for processing and settling the transactions initiated by the paymentfacilitators merchants, but they can also offer so much more.

A master merchant, often referred to as a paymentfacilitator or merchant aggregator, is a third-party agent that acts as the link between acquirers and online merchants. The master merchant simplifies the onboarding process for sub-merchants by handling the complexities of payment integration, security requirements, and compliance.

Whether youre a product leader, fintech founder, or payments partner, understanding the language behind embedded finance platforms is mission-critical. This blog post is your jargon-free guide to all the advanced embedded finance terminology you’ll encounterfrom OAuth to multi-rail payment strategies.

Real-time payments: Funds move instantly between financial institutions, even on weekends and holidays. Banks and Credit Unions: Modernize Your Offering Use FedNow to: Offer customers real-time P2P and B2B payments. Reduce reliance on legacy payment rails like wire and ACH. What is FedNow? Improve cash flow visibility.

But launching your eCommerce store is just half the equationaccepting payments efficiently and effectively is a whole different ball game. On the surface, it seems effortless, with customers only taking a few seconds to initiate and complete payments. Its the bridge between an eCommerce website, its customers, and the bank.

If youre a software provider looking to boost revenue, streamline operations, and deliver more value to your users, ISV integrated payments can be a game-changer. Embeddingpayments directly into your platform can unlock tremendous benefits both for you and your users. The best part?

Customers in this age of instant gratification always expect a smooth and seamless online payments experience. As a business owner, you must have a clear understanding of how online paymentsprocessing works to be able to create a hassle-free checkout process that will keep buyers coming back to your eCommerce store.

Over the years, BrainStorm has evolved from a training services company to a world-class SaaS platform. Infinicept is a provider of embeddedpayment solutions. From the beginning, the company’s goal has been to help users achieve more with their software tools. G-P, Global Made Possible.

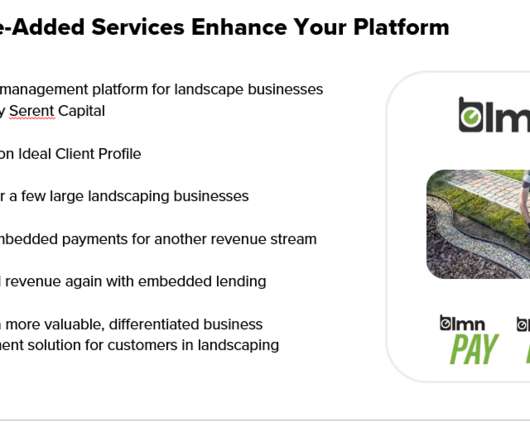

An ICP aligns your product, sales, marketing, service, and executive teams to all focus on your highest-value accounts. Brex then scaled its payments business quickly. Then, it built an entire ecosystem around it, soon launching Shopify payments, an embeddedpayment tool that quickly became the largest piece of the business.

What is a payment processor? A payment processor facilitates the flow of transactions typically made with credit cards, debit cards, and other digital payments. The processor is responsible for processing and settling the transactions initiated by the paymentfacilitators merchants, but they can also offer so much more.

Before we dive into the risks associated with payments, let’s review why embeddingpayments is good for SaaS businesses and the three paymentprocessing solutions available to software companies today. What are the benefits of adding payments to vertical software? What is a PayFac® developer?

As you work to expand your SaaS, software, mobile games, or other digital product business worldwide, having the right payment methods available to global customers is key to ensuring they all feel comfortable purchasing. If you want to offer more payment methods around the world, don’t miss this episode of Growth Stage.

This is especially true now more than ever before as Software-as-a-Service (SaaS) solutions continue to be amongst the fastest-growing segment within the tech world. Consumer adoption of digital solutions is accelerating at a rapid pace, with the SaaS market projected to grow from $315 billion in 2025 to $1,131 billion in 2032.

A master merchant, often referred to as a paymentfacilitator or merchant aggregator, is a third-party agent that acts as the link between acquirers and online merchants. The master merchant simplifies the onboarding process for sub-merchants by handling the complexities of payment integration, security requirements, and compliance.

Did you know embeddedpayments can increase a software provider’s income? They turn payments into a new source of money. B2B payment transactions exceeded 15 billion in 2024 , with digital payments now making up 85% of transactions. Embeddedpayments are a game-changer. billion in 2023 to $291.3

And it’s all thanks to embedded finance and embedded fintech. Embedded finance isn’t entirely a new concept. Airline credit cards, payment plans for costly items, and car rental insurance are forms of embedded finance that have been around for a while. Today, you don’t even have to exit the app.

Embedded Finance is more than just a buzzword; it represents a fundamental shift in how financial services are delivered and consumed today. Ian Hillis, Head of Growth at Worldpay for Platforms discusses this new term and what the opportunity may await software providers on our latest episode of PayFAQ: The EmbeddedPayments podcast.

Imagine cutting years off payment system setup. The number of PaymentFacilitators (PayFacs) has grown 13.8% For businesses, this means they can use payment systems without starting from scratch. PayFac as a Service lets companies add paymentprocessing to their platforms. each year since 2018.

Key takeaways What is embedded finance and how it integrates financial services into non-financial platforms. The benefits and challenges of implementing embedded finance for businesses and consumers. Examples of embedded finance applications across various industries. What is embedded finance?

Stripe Connect is a comprehensive paymentprocessing solution designed to cater to the unique needs of platforms and marketplaces. As a part of the broader Stripe suite, it facilitates digital transactions and enables businesses to accept credit card payments and manage complex money flows. What is Stripe Connect?

Business owners are increasingly showing an overwhelming preference for SaaS platforms with embeddedpayment capabilities as part of their offerings. Manual paymentprocessing and disconnected software and payment solutions are dying out, and research by Sifted shows that the integrated financial services market will grow to $3.6

Unlock Hidden Revenue, Scale Smarter, and Choose the Right Partner Introduction: Payments Are No Longer Just Transactions If you’re building a SaaS or platform business, embeddingpayments isnt just a featureits a business model. But heres the thing: not all embeddedpayment solutions are created equal.

Ever sat through a payments meeting and wondered if you accidentally joined a secret society that only speaks in acronyms? Between PFaaS, NACHA, and VPA, the payments industry has more abbreviations than a teenagers group chat. You’re not alone. Some you’ll recognize. Some you’ll want to forget.

We organize all of the trending information in your field so you don't have to. Join 80,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content