If I had to summarize venture capital today, it would be like this: There is Very Little Oxygen Today Above $200m Valuations

What do I mean?

It’s still a weird world in venture:

- Firms are both shutting down and raising new funds.

- More entrepreneurs are doing direct investing themselves than ever.

- Unicorns are hurting, but — Nasdaq is at an all-time high.

So net net we still see very high levels of seed investment. Folks are still hoping and dreaming that bet, as improbably as it might be, could still do 100x-1000x and becoming the next Datadog, Snowflake, Klaviyo, Samsara, Uber, etc.

But the problem in SaaS especially is that the average public SaaS company is trading for about $2 Billion, and at about 6x ARR.

So what? Well at least in theory, you can still make 100x or more at a $20m valuation if the company ends up worth $2 Billion. Sort of, if you ignore dilution.

But how do you make 8x-10x at the later stages, Series B and on? It becomes mathematically very hard to make 8x-10x on any valuation in SaaS above $200m post-money.

Yes growth investors don’t expect every deal to do 8x-10x. But they do need some of them to. And if they don’t see at least a clear path to potentially get there, it’s very hard to do the deal.

In 2021, with public SaaS stocks trading at 20x or more, and many worth $10B or even $100B, it was easy to see 8x-10x from even a $1B valuation. Hence, so many unicorns.

Today, it’s just much harder for growth investors to see an 8x-10x outcome past a $200m valuation.

Net net, we are seeing a world where seed remains vibrant, but each stage after that is tougher.

"Very few 'traditional' SaaS rounds are really getting done at north of $200m valuations" pic.twitter.com/TZS8jTcObM

— SaaStr (@saastr) January 21, 2024

And after a $200m valuation? You really have to >prove< you are an outlier today to raise at that valuation. Not just have some good reasons to hope.

If nothing else, even after the Unicorn Bust and 18 months of tough headlines, I find most founders at Series A and later are still too optimistic about how hard it will be to raise the next round. Just trust me. Go find out, ask around, ask your board and existing investors. Your existing cash may need to last even longer than you were planning.

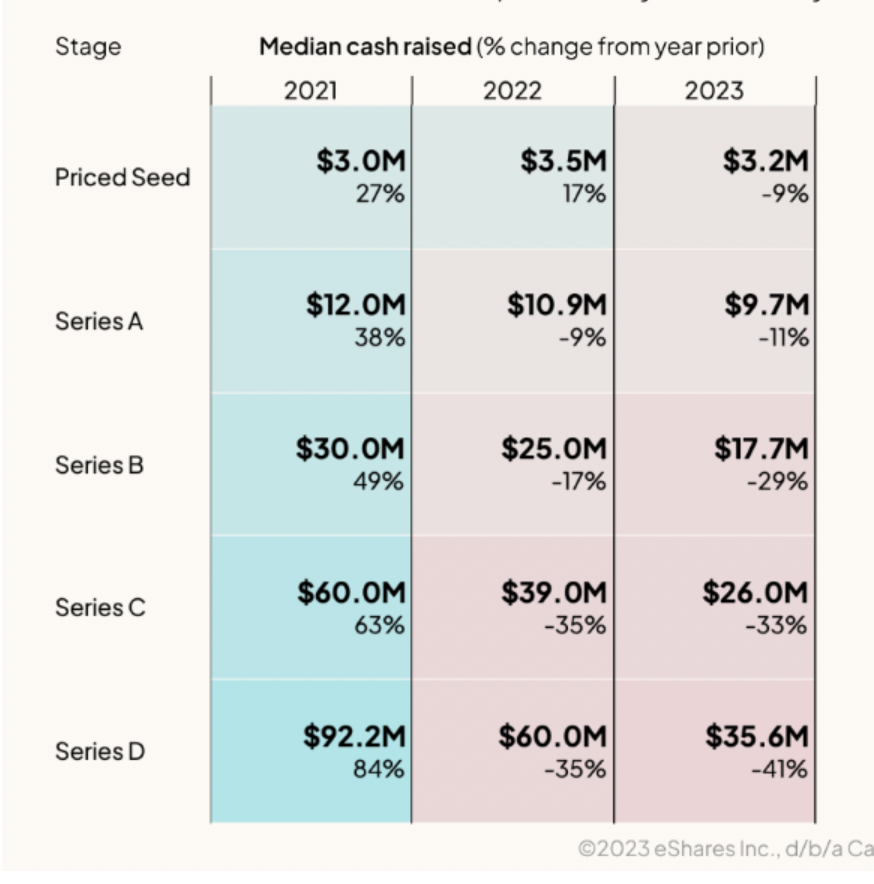

The latest Carta data I think illustrates the point well, although even there it may be too bullish, given how large AI rounds have warped the data. Seed rounds are down -9% this year. But Series D? -41%. I suspect in SaaS, it’s closer to -80% without AI hyped deals.

…

And a great recent deep dive on VC SaaS investing here: