So we’ve done a lot with Workday over the years at SaaStr but haven’t done a deep 5 Interesting Learnings dive. But we should have. Workday is one of the iconic enterprise SaaS leaders.

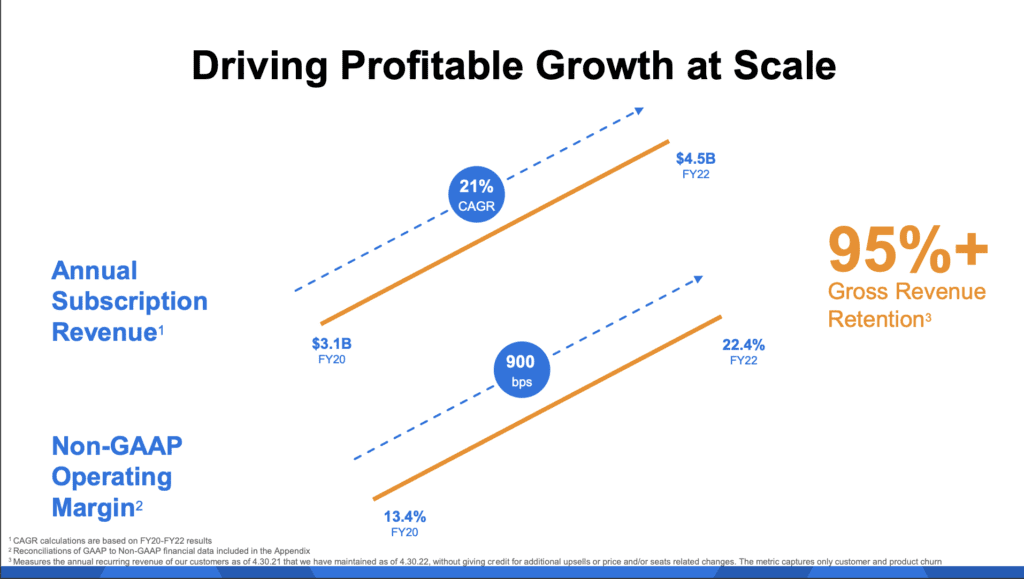

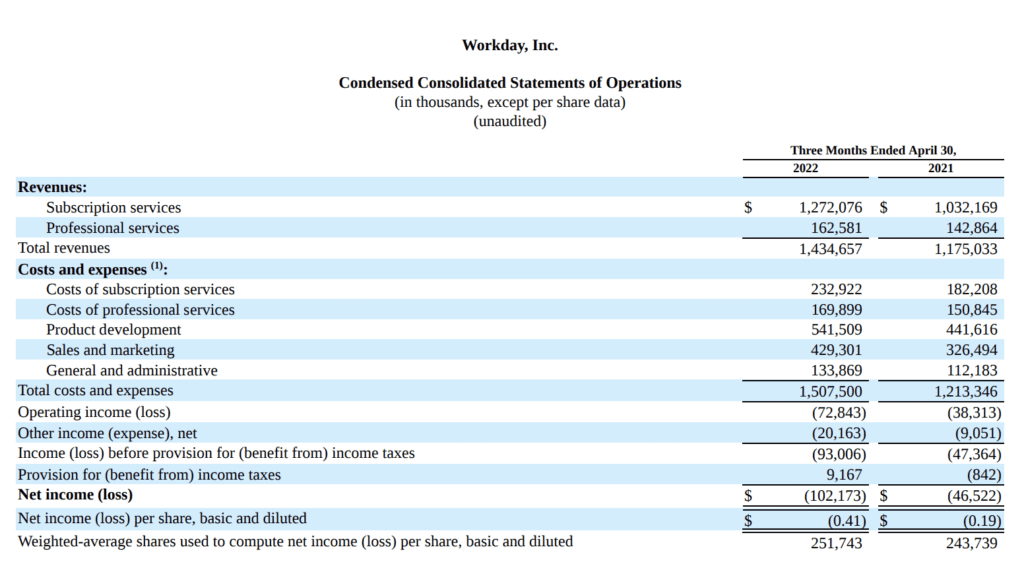

It’s scaling efficiently and impressively. At a $6 Billion revenue run ($4.5B in SaaS revenue), it’s growing an impressive 22% with fairly epic operating cash flows of 30% (more on that below).

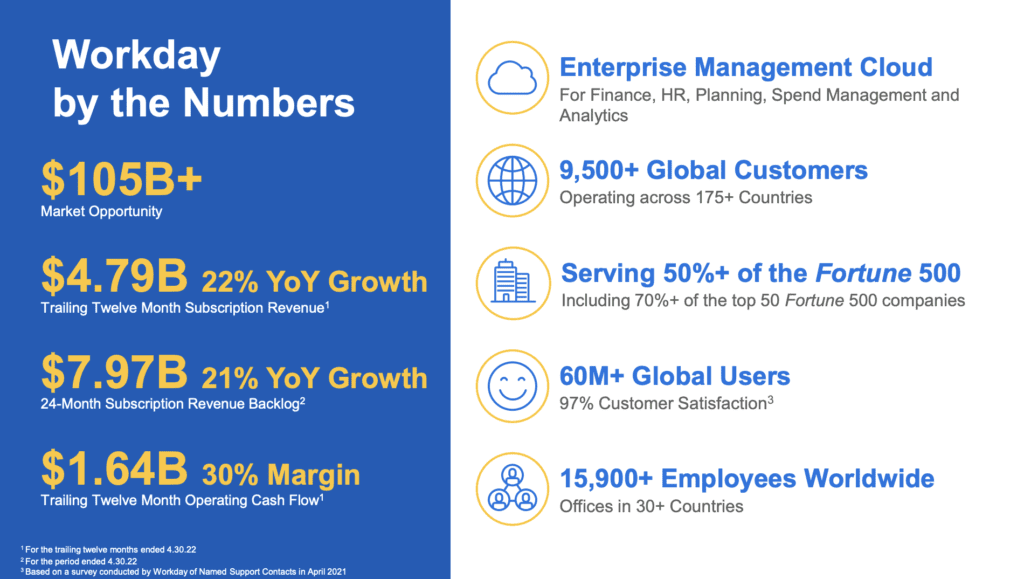

#1. 9,500 customers at $6B in ARR, so about $600,000 ACV per customer. That’s enterprise! And that’s what happens when 50%+ of the Fortune 500 are your customers.

#2. 95% GRR. It’s again nice to see a SaaS leader break out GRR, not just NRR. GRR is revenue retention from existing accounts, including churn but excluding any account expansion. Workday’s NRR is relatively low, which is probably why it highlights GRR over NRR / NDR. But in any event, it shows you should aim for 95%+ GRR in your enterprise accounts as well.

#3. Generating epic free cash flow at 30% of revenues, and $1.6B+ Billion a year in operating cash flow. Workday has become a cash engine at scale, as all top SaaS companies should. Of course, a $6B run-rate is pretty mature. But it’s still good to see confirmation that 30% of revenue should drop to free-cash flow at scale. Workday is another example of hitting that goal at scale. Qualtrics, for example, has 35% margin on its professional services. More on that here.

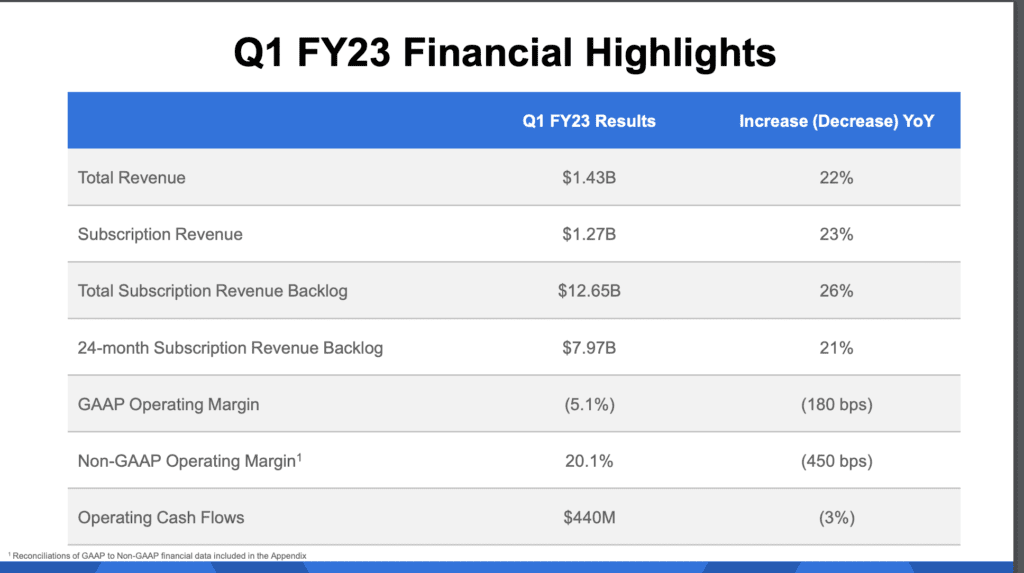

#4. Breaks-even on Professional Services (11% of revenues). Even at its scale, Workday doesn’t make money on services, in fact it loses just a little bit on them. It brought in $163m in pro serve revenue the past quarter — but the costs were $170m. Likely more if you think about the fully-burdened cost of providing them. Different companies have different approaches here. Workday’s goal, like Salesforce’s, is to push as much of this on services partners as possible.

#5. 16,000 employees, so about $375,000 in revenue per employee. That’s pretty efficient, higher than the $250k we often see for scaling SaaS companies, although not the crazy high efficiency we see in some B2C and other companies. A key contribution to profitability.

And a few other interesting learnings:

#6. 24 Month Subscription Backlog of 21%. That’s OK but not higher than their growth rate, showing that Workday isn’t leveraging a big backlog of signed longer term deals to leverage for even higher growth in the coming quarters.

#7. Adding 1,000 European jobs to its Dublin HQ. Another Cloud leader standardizing on Dublin as their EMEA HQ.

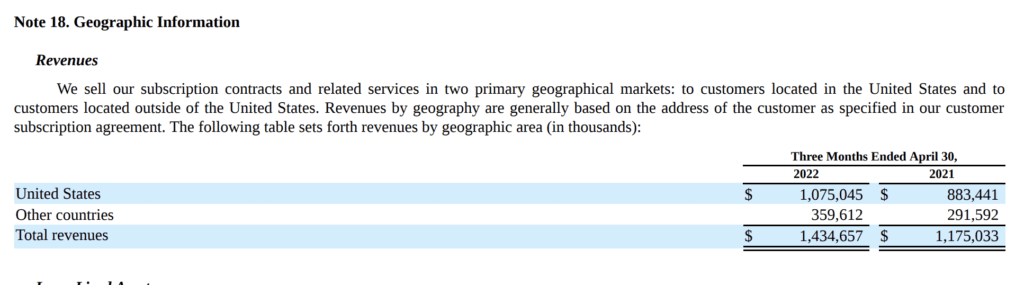

#8. 75% of revenue in the U.S. Perhaps not a surprise given how country-specific HR and especially finance platforms are. But lower than many B2B SaaS companies whose products are less subject to specific financnial and other accounting regulations, rules and processes.

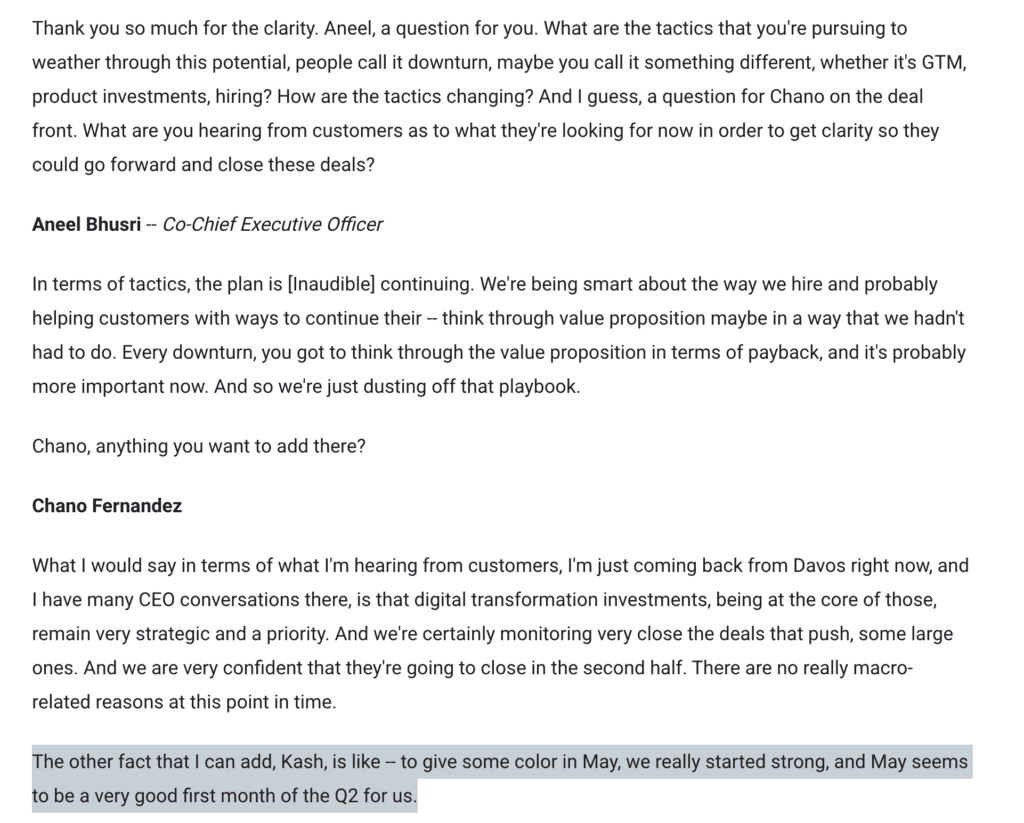

#9. Not seeing any downturn yet. Workday saw a few big deals push a quarter or so, but they aren’t seeing any wholesale decline in digital transformation or pipeline creation. They are holding to 20%+ growth going forward.

Quite a run! Workday will be at a $10 Billion run rate before you know it. 95% GRR combined with 20%+ annual growth gets you there.